FuelCell Energy's Strategic Restructuring and Market Position in the Distributed Power Generation Sector

FuelCell Energy (FCEL) is navigating a pivotal phase in its corporate evolution, marked by aggressive cost-cutting measures and a strategic pivot toward distributed power generation. As the global energy landscape shifts toward decarbonization and AI-driven data center demand surges, the company's restructuring efforts and market positioning warrant close scrutiny for long-term investors.

Strategic Restructuring: Cost Discipline and Technology Focus

FuelCell Energy has announced a restructuring plan targeting a 30% reduction in annual operating expenses compared to fiscal 2024, achieved through a 22% workforce reduction and operational streamlining. This move aligns with the company's refocusing on carbonate-based distributed generation, a technology it positions as critical for high-efficiency, low-emission power solutions. By pausing R&D on solid oxide technology, FuelCell EnergyFCEL-- aims to consolidate resources into its core carbonate platform, which has already demonstrated efficiency rates exceeding 50%.

The appointment of Mike Hill as Chief Commercial Officer underscores the company's intent to capitalize on the data center market, where AI's exponential growth is driving demand for reliable, clean energy. Hill's expertise in commercial strategy could prove vital as FuelCell Energy targets partnerships like its 100MW Memorandum of Understanding (MOU) with Inuverse for South Korea's AI Daegu Data Center, set to begin implementation in 2027.

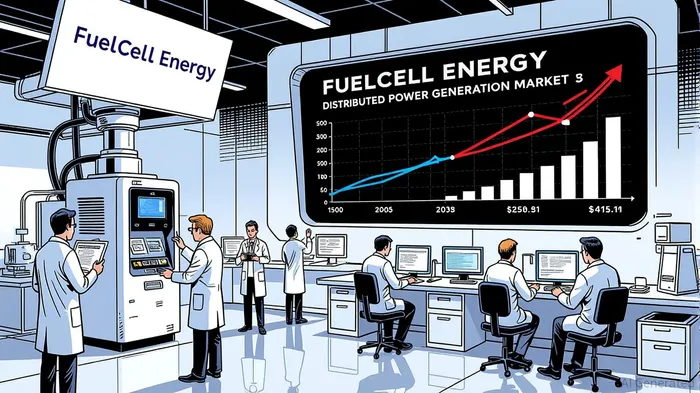

Market Position and Growth Drivers

The distributed power generation market is forecasted to expand from $150.7 billion in 2022 to $415.1 billion by 2030, driven by decarbonization mandates and rising energy demands. Within this, the fuel cell segment is projected to grow at a 17.7% CAGR, reaching $15.2 billion by 2030. FuelCell Energy's partnerships, such as the Tri-gen system with ToyotaTM-- and the 360MW data center power alliance with Diversified EnergyDEC-- and TESIAC, position it to capture a share of this growth.

However, the company faces stiff competition from established players like Ballard Power SystemsBLDP-- and Capstone Turbine Corp., as well as emerging technologies like proton exchange membrane (PEMFC) fuel cells, which dominated 60% of global shipments in 2022. FuelCell Energy's focus on carbonate technology, while niche, could differentiate it in stationary power applications, particularly in data centers where thermal efficiency and reliability are paramount.

Financial Performance and Risks

Despite a 97% year-over-year revenue increase in Q3 2025 to $46.7 million, driven by product shipments to Gyeonggi Green Energy in South Korea, the company reported a net loss of $92.5 million, largely due to restructuring and impairment charges. This follows a Q3 2024 net loss of $35.1 million. While the backlog has grown to $1.24 billion, reflecting new service agreements and project commitments, the company's negative free cash flow of -$35.17 million in Q1 2025 highlights liquidity risks.

FuelCell Energy's debt-to-equity ratio remains relatively low compared to peers, but its ability to convert backlog into sustainable cash flows will be critical. The company's $326 million in cash and short-term investments as of Q3 2024 provides some flexibility, though ongoing restructuring costs and capital expenditures for data center projects could strain resources.

Long-Term Investment Potential

FuelCell Energy's strategic alignment with the distributed power generation sector and data center demand is compelling. The global shift toward AI infrastructure and ESG compliance creates a tailwind for its carbonate-based solutions, particularly as absorption chilling and rack cooling technologies gain traction. However, the company's financial performance—marked by significant net losses and negative cash flows—raises questions about its path to profitability.

For long-term investors, the key variables will be:

1. Execution of Restructuring: Sustained cost discipline and operational efficiency gains are essential to offset R&D and restructuring expenses.

2. Data Center Contract Conversion: The 100MW Inuverse MOU and 360MW ADC partnership must translate into revenue to validate the company's market positioning.

3. Technology Differentiation: Maintaining a leadership position in carbonate fuel cells amid competition from PEMFC and other emerging technologies.

Conclusion

FuelCell Energy's strategic restructuring and focus on distributed power generation position it to benefit from the AI-driven data center boom and decarbonization trends. However, the company's financial challenges—particularly its reliance on non-cash revenue and high restructuring costs—demand cautious optimism. Investors should monitor its ability to convert partnerships into revenue, sustain cost discipline, and demonstrate technological leadership in a competitive market.

Comentarios

Aún no hay comentarios