FSK's $400M 6.125% Unsecured Notes Offering Due 2031: Capital Structure Optimization and Yield Attractiveness in a High-Rate Environment

In a landscape defined by persistently elevated interest rates, FS KKR Capital Corp.FSK-- (FSK) has announced a $400 million offering of 6.125% unsecured notes maturing in January 2031. This move, part of FSK's broader capital structure optimization strategy, raises critical questions about risk-adjusted returns and the alignment of its financing decisions with market conditions. By analyzing FSK's leverage profile, credit metrics, and yield competitiveness, this article evaluates whether the offering represents a compelling opportunity for investors.

Capital Structure Optimization: Balancing Leverage and Liquidity

FSK's debt-to-equity ratio has risen to 1.38 as of June 30, 2025, up from 1.28 in March and 1.15 in December 2024[2]. This increase reflects a deliberate shift toward unsecured debt, which now accounts for 54% of total debt[3]. The company's access to $2.4 billion in available bank lines and $312 million in cash and equivalents[2] underscores its liquidity flexibility, a critical factor in maintaining its Fitch Ratings' affirmed 'BBB-' long-term IDR with a stable outlook[1].

The new notes, priced at a spread of SOFR +274.75 bps[3], are part of a diversified funding strategy that includes secured bank facilities and collateralized loan obligations (CLOs). This approach mitigates refinancing risk while leveraging FSK's affiliation with KKR's $648 billion AUM platform, which provides access to underwriting expertise and SEC exemptive relief[3]. The proceeds, earmarked for general corporate purposes, could further strengthen FSK's net leverage ratio of 1.26x[3], aligning with its target of maintaining a balanced capital structure.

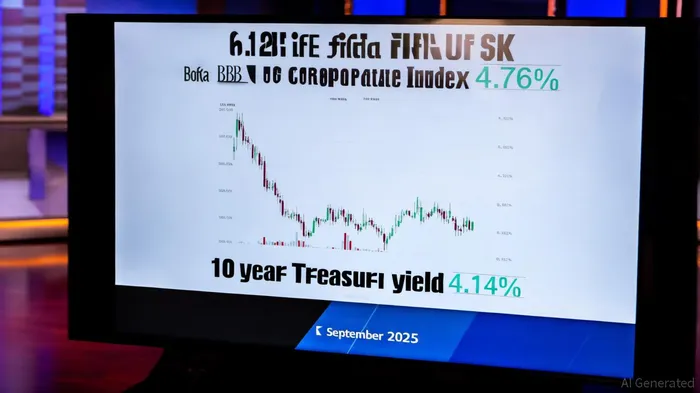

Yield Attractiveness: A Premium in a High-Rate Environment

The 6.125% coupon on FSK's notes stands out against current benchmark rates. As of September 2025, the 10-year U.S. Treasury yield is 4.14%[4], while the ICE BofA BBB US Corporate Index effective yield hovers at 4.76%[2]. This positions FSK's offering with a yield spread of approximately 200 bps over the BBB index and 200 bps over the risk-free rate. For investors seeking income in a high-rate environment, this premium appears attractive, particularly given FSK's 'BBB' rating from KBRA[3], which signals moderate credit risk but not extreme volatility.

However, the yield's appeal hinges on FSK's ability to manage interest rate exposure. With a 2031 maturity, the notes are sensitive to long-term rate fluctuations. Yet, FSK's stable outlook from Fitch[1] and its diversified $13.6 billion investment portfolio across 218 companies[3] suggest resilience against sector-specific shocks. The recent upsizing of its senior secured revolver to $4.7 billion[3] further bolsters liquidity, reducing the likelihood of near-term distress.

Risks and Strategic Considerations

While the offering's yield is compelling, investors must weigh several risks. First, the long maturity exposes FSKFSK-- to potential refinancing challenges if rates rise further. Second, the company's reliance on unsecured debt—now 54% of its total—could amplify vulnerability during liquidity crunches. Third, macroeconomic headwinds, such as a recession or inflationary spikes, may pressure FSK's investment portfolio, which is concentrated in private credit.

That said, FSK's strategic alignment with KKR's credit platform[3] and its proactive liquidity management (e.g., the upsized revolver[3]) provide a buffer against these risks. The stable outlook from Fitch[1] also implies confidence in FSK's ability to navigate the current environment without downgrades.

Conclusion

FSK's $400 million notes offering represents a calculated step toward optimizing its capital structure while delivering competitive yields in a high-rate environment. The 6.125% coupon, coupled with a 'BBB-' credit profile and robust liquidity, offers a risk-return profile that may appeal to income-focused investors. However, the long maturity and macroeconomic uncertainties necessitate careful due diligence. For those aligned with FSK's strategic vision and risk tolerance, the offering could serve as a valuable addition to a diversified fixed-income portfolio.

Comentarios

Aún no hay comentarios