French Fiscal Resilience Amid Global Volatility: A Comparative Analysis of Policy Credibility and Market Confidence

In an era of geopolitical tensions, trade wars, and persistent inflation, fiscal credibility has become the linchpin of market confidence. Nowhere is this more evident than in France, where 2025 fiscal consolidation efforts aim to balance deficit reduction with economic resilience. This article examines France's fiscal strategy through the lens of comparative policy credibility and market confidence, benchmarking it against Germany, Italy, and the U.S.

France's 2025 Fiscal Consolidation: Ambitions and Constraints

France's 2025 Finance Law targets a public deficit reduction from 6.1% of GDP in 2024 to 5.4% in 2025, achieved through €50 billion in spending cuts and temporary tax increases on large corporations and high-income earners, according to a Funds Protector analysis. These measures include an 8% tax on share buybacks for firms with €1 billion+ revenues and an exceptional contribution on corporate profits, as noted by INSEE. While the government emphasizes protecting essential sectors like healthcare and education, critics argue the reliance on tax hikes risks stifling growth, particularly in a fragmented political landscape, as highlighted in the Banque de France report.

The OECD has cautiously endorsed the plan, while the IMF Fiscal Monitor warned of "policy uncertainty" and the need for structural reforms to ensure long-term sustainability. Meanwhile, the Banque de France notes that household savings rates and the temporary nature of some measures may cushion near-term impacts on consumption; industry comparators reported by TheBanks data provide additional context. However, forecasts suggest the deficit may only reach 5.2% of GDP, underscoring risks of fiscal slippage, according to a Goldman Sachs report.

Comparative Fiscal Credibility: France vs. Germany, Italy, and the U.S.

France's fiscal trajectory contrasts sharply with its peers. Germany, despite slower growth, has maintained fiscal discipline through its constitutional Debt Brake, which limits federal borrowing to primary balances, a feature discussed in that Goldman Sachs report. Italy, meanwhile, has surprised observers with a credible path to reduce its deficit below the EU's 3% threshold by 2026, bolstered by political stability and targeted spending cuts, according to a Politico report. The U.S., in contrast, faces growing concerns over debt sustainability, with primary deficits unlikely to improve significantly under current policies, per a Lombard Odier analysis.

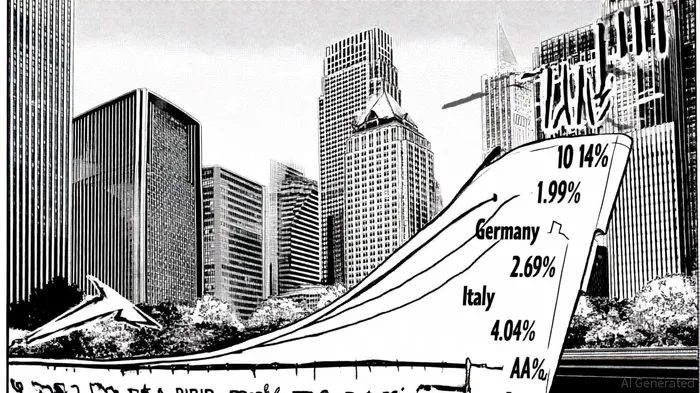

Credit ratings reflect these divergences. France retains an "AA-" rating from Fitch but faces a "Negative" outlook, while Germany's "AAA" rating underscores its fiscal prudence, as shown by TheBanks. Italy's "BBB" rating (Fitch) and 3.47% bond yield highlight its precarious position, yet recent political stability has improved market sentiment, according to a Reuters report. The U.S., despite an "AA-" rating from S&P, sees its 4.04% bond yield signal investor caution amid rising debt levels, as reflected in Bloomberg data.

Market Confidence: Volatility and Investor Sentiment

Market confidence in France remains mixed. While the government's fiscal discipline has stabilized bond yields (3.48% in 2025), political tensions-including wealth tax debates and infrastructure disruptions-have dented investor sentiment, as shown by Permutable's indicators. The Political Tension Index for France ranks higher than Germany and Italy, reflecting public backlash against austerity measures, according to the CBRE survey.

In contrast, Germany's industrial sector shows renewed optimism, with the Manufacturing Sentiment Index stabilizing after 25 months of contraction, per a Savills report. Italy, though volatile, benefits from European investors seeking value-add opportunities in repriced assets, as noted by CBRE. The U.S., meanwhile, faces a paradox: 54% of consumers expect global economic improvement in 2025, yet bond markets punish fiscal uncertainty with elevated yields, illustrated in a Visual Capitalist chart.

Risks and Opportunities for Investors

For investors, France's fiscal strategy presents a dual-edged sword. On one hand, the government's commitment to reducing deficits and addressing climate and cybersecurity risks aligns with IMF calls for "pragmatic multilateralism," as discussed in the Funds Protector analysis. On the other, political fragmentation and reliance on temporary measures could undermine long-term credibility.

Comparatively, Germany's Debt Brake and Italy's consolidation plans offer clearer frameworks, while the U.S. remains exposed to policy shocks from trade wars and partisan gridlock. Investors must weigh these factors against sector-specific vulnerabilities-for example, France's aerospace and pharmaceutical industries face higher exposure to U.S. trade disruptions, a point underscored by the Banque de France report.

Conclusion

France's 2025 fiscal consolidation is a critical step toward restoring credibility, but its success hinges on navigating political and economic headwinds. While it lags behind Germany and Italy in fiscal discipline, it outperforms the U.S. in deficit reduction and market resilience. For investors, the key lies in balancing short-term volatility with long-term structural reforms, ensuring that France's fiscal strategy remains credible in an increasingly uncertain world.

Comentarios

Aún no hay comentarios