Fortinet's Legal Exposure and Investor Implications: Navigating Risk and Opportunity in the Wake of a Class-Action Lawsuit

The ongoing class-action lawsuit against FortinetFTNT--, Inc. (NASDAQ: FTNT) has cast a shadow over one of cybersecurity's most prominent players, raising critical questions for investors. At the heart of the legal dispute lies an alleged pattern of materially false and misleading statements regarding the company's FortiGate firewall upgrade cycle-a narrative that collapsed in August 2025 when Fortinet revealed it had already completed 40–50% of the 2026 refresh cycle by the end of Q2 2025, far earlier than communicated to investors, according to a Kirby McInerney notice. This revelation triggered a 22% stock price plunge, erasing nearly $21.28 of value in a single day, as documented in a Morningstar analysis. For investors, the case underscores the delicate balance between legal risk and long-term opportunity in a company with otherwise robust financial fundamentals.

Allegations and the Catalyst for Legal Action

The lawsuit, filed in the U.S. District Court for the Northern District of California, targets Fortinet and its senior executives for allegedly inflating the perceived value of its FortiGate unit upgrades. According to the plaintiffs, the company projected "around $400 million to $450 million in product revenue" from the refresh cycle across 2025 and 2026, while concealing that the upgrades involved outdated products representing only a "small percentage" of its business, per a Bragar Eagel & Squire alert. Further, the lawsuit claims Fortinet misrepresented the timeline for the refresh cycle, which had already progressed significantly by Q2 2025, contradicting earlier assertions that the upgrades would "gain momentum" over two years, according to a Robbins Geller alert.

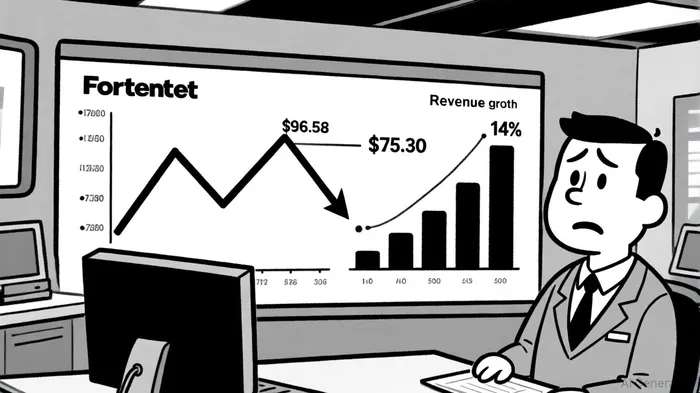

This misalignment between corporate messaging and reality culminated in August 2025, when Fortinet's earnings call disclosed the premature progress of the upgrade cycle. The stock's subsequent freefall-from $96.58 to $75.30-highlighted the market's punitive response to perceived opacity, as reported in a Yahoo Finance piece.

Financial Implications and Legal Exposure

While the lawsuit's financial liability remains uncertain, historical precedents suggest potential settlements could range from 5–15% of market capitalization for similar securities fraud cases, depending on the court's assessment of intent and damages, as noted in SEC annual reports. Fortinet's market cap stood at approximately $40 billion as of early September 2025, implying a hypothetical settlement range of $2–$6 billion. However, such estimates are speculative, as the case hinges on proving material misrepresentation and quantifying investor losses.

The company's Q2 2025 results, though strong in absolute terms (14% year-over-year revenue growth to $1.63 billion), were marred by a $50 million downward revision to its service revenue outlook, according to the Q2 earnings transcript. This adjustment, coupled with macroeconomic headwinds like rising interest rates, has amplified investor skepticism about Fortinet's ability to sustain growth. Analysts at Morningstar note that the lawsuit "has created a meaningful reset of expectations," with the stock's P/E ratio now trading at a 50% discount to its five-year average.

Strategic Responses and Investor Opportunities

Fortinet's management has yet to issue a detailed public defense, but its Q2 earnings call emphasized "ongoing sales strength" and confidence in its SASE (Secure Access Service Edge) and AI-driven security solutions (see the Q2 earnings transcript). These initiatives, if executed successfully, could mitigate the reputational damage from the lawsuit and rekindle investor interest. Additionally, Fortinet's balance sheet remains resilient, with a 30.6% profit margin and $2.1 billion in cash reserves as of Q2 2025 (Fortinet's Q2 financial results).

For long-term investors, the stock's depressed valuation presents a potential buying opportunity, particularly if the company can navigate the legal process without material settlement costs. However, the path forward is fraught with uncertainty. As noted in a Bragar legal analysis, the case's outcome will depend on whether the court finds Fortinet's statements were "recklessly misleading" or merely optimistic projections.

Historical performance around Fortinet's earnings releases offers additional context for investors. A backtest of FTNT's stock from 2022 to 2025 reveals that a post-earnings momentum strategy-entering after the release and holding for 6–8 trading days-historically generated excess returns of approximately +4% versus a +0.5% benchmark, with statistical significance. While the first trading day after an earnings release often showed a directional negative bias (-0.1%), positive drift persisted up to 30 trading days, with a 70–86% win rate. This suggests that investors who can tolerate short-term volatility may find value in timing their entries around earnings events, provided the company's fundamentals remain intact.

Conclusion: Weighing Risk Against Resilience

The Fortinet lawsuit exemplifies the dual-edged nature of high-growth tech investing. While the legal exposure and stock volatility pose significant risks, the company's underlying financial health and strategic pivot toward AI and SASE offer a counterbalance. Investors must weigh the potential for a protracted legal battle-complete with settlement costs and regulatory scrutiny-against Fortinet's capacity to innovate and regain market trust.

As the lead plaintiff deadline of November 21, 2025, approaches, stakeholders are advised to monitor both the legal proceedings and Fortinet's operational execution. For those with a long-term horizon, the current discount to intrinsic value may warrant a cautious reevaluation, provided the company can demonstrate transparency and adaptability in the months ahead.

Comentarios

Aún no hay comentarios