U.S. Fiscal Sustainability Risks and Strategic Asset Allocation in a Debt-Crisis Scenario

The U.S. fiscal landscape is at a precarious inflection point, with Ray Dalio's warnings about a looming "debt-induced heart attack" resonating across financial circles. According to a Fortune article, Dalio has sounded the alarm on unsustainable borrowing, noting that the U.S. government spends 40% more than it collects in revenue, with monthly interest expenses exceeding $60 billion-a figure that now outpaces revenue from tariffs. The Congressional Budget Office estimates that the Trump-era One Big Beautiful Bill Act (OBBBA) will add $3.4 trillion to the national debt, further straining fiscal sustainability, as reported in the Fortune article. These dynamics, coupled with a debt-to-GDP ratio projected to surpass 202% by 2025, underscore the urgency for investors to rethink strategic asset allocation.

Historical Precedents and Policy Responses

Past fiscal crises offer instructive parallels. During the 2008 Global Financial Crisis, the Federal Reserve's purchase of distressed debt stabilized markets but also expanded its balance sheet to unprecedented levels. Similarly, the 2020 pandemic response prioritized direct fiscal support-such as stimulus checks-to sustain consumer spending, accelerating recovery despite a surge in public debt, according to a CME Group report. However, post-2010 quantitative easing (QE), which focused on government bonds, failed to meaningfully boost economic growth or inflation, revealing a decoupling between asset prices and real economic outcomes, as the CME GroupCME-- report argues.

A critical lesson from these episodes is the role of investor confidence. As Dalio warns in a Quantified Strategies analysis, a loss of faith in U.S. debt could trigger a self-reinforcing spiral: falling demand for Treasuries would force higher interest rates, exacerbating fiscal deficits and further eroding confidence. This scenario mirrors the 2025 trade conflict, where tariff-driven inflation and geopolitical uncertainty caused immediate stock market declines and widened sovereign risk premiums, according to J.P. Morgan's asset-allocation views.

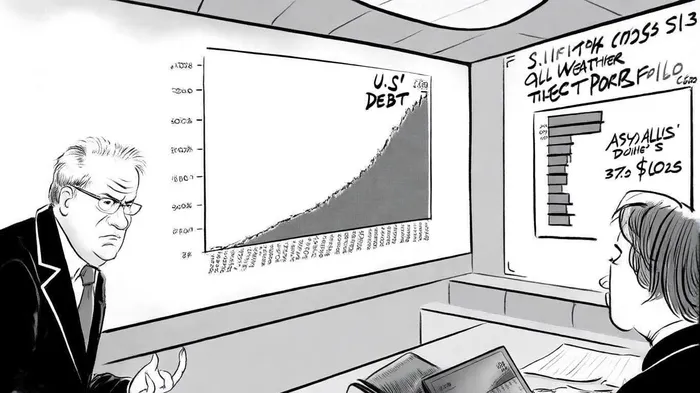

Strategic Asset Allocation in a Debt-Crisis Framework

Ray Dalio's principles, honed at Bridgewater Associates, provide a roadmap for navigating such risks. His All Weather Portfolio, designed to perform across inflationary, deflationary, and stagflationary environments, allocates 55% to bonds, 30% to stocks, and 15% to commodities and hard assets, as Dalio outlines in the Fortune article. This risk-parity approach balances volatility across asset classes rather than relying on capital allocation, mitigating the impact of any single market shock. During the 2020 pandemic, the portfolio declined only 6% versus a 30% drop in the S&P 500, demonstrating its defensive resilience, a point noted in the Fortune article.

For a debt-crisis scenario, Dalio emphasizes three pillars:

1. Inflation Hedges: Treasury Inflation-Protected Securities (TIPS) and gold, which he advocates holding at 10–15% of a portfolio, offer protection against currency devaluation, consistent with J.P. Morgan's asset-allocation guidance.

2. Diversification Across Macroeconomic Cycles: Bridgewater's Pure Alpha strategy, which leverages macroeconomic insights to adjust positions in sovereign bonds, currencies, and commodities, thrived during 2008 by being long on Treasuries and the yen while shorting risky assets, as documented in the Quantified Strategies analysis.

3. Alternative Assets: Institutions increasingly favor private equity, real estate, and commodities to reduce correlation with traditional markets, a strategy validated by Yale University's endowment model in a MarketClutch analysis.

J.P. Morgan's 2025 asset allocation recommendations echo these principles, advocating an overweight in sovereign bonds (e.g., Italian BTPs, UK Gilts) and a cautious stance on credit due to tight spreads. Meanwhile, LPL Research's Strategic Asset Allocation Committee (STAAC) favors emerging market equities and TIPS over expensive domestic growth stocks, reflecting a focus on value and inflation resilience.

Institutional Adaptation and Forward-Looking Strategies

The 2008 crisis instilled a heightened awareness of liquidity risk, prompting investors to stress-test portfolios and reduce leverage. For example, post-2008, major institutions adopted dynamic asset allocation frameworks, adjusting exposures based on real-time macroeconomic signals, as described in the MarketClutch analysis. This adaptability is critical today, as the U.S. faces a "very dangerous inflection point" where declining tax revenues and rising interest costs could trigger a fiscal reckoning within two to three years, a concern highlighted in the Fortune article.

Investors must also contend with shifting global dynamics. Foreign holdings of U.S. debt have dwindled, with China and Japan now holding less than 5% of public debt-a trend that could amplify volatility if confidence wanes, the CME Group report notes. In this context, diversifying into non-U.S. assets and hedging against dollar depreciation becomes paramount.

Conclusion

The U.S. fiscal trajectory, as outlined by Dalio and corroborated by historical precedents, demands a proactive approach to asset allocation. While the immediate risk of a sudden debt crisis remains low, the long-term erosion of bond values and rising interest rate volatility necessitate portfolios that prioritize resilience over returns. By integrating inflation hedges, macroeconomic diversification, and alternative assets-principles championed by Bridgewater and other institutions-investors can navigate the uncertainties of a debt-laden world. As Dalio's warnings crystallize into reality, the markets will reward those who anticipate the next inflection point.

Comentarios

Aún no hay comentarios