Fidelis Insurance Group's Q3 2025 Earnings Outlook: Strategic Performance and Market Positioning in a Competitive Landscape

Historically, FIHL'sFIHL-- earnings announcements have shown a modest positive trend. A backtest from 2022 to 2025 reveals that a simple buy-and-hold strategy following these events yielded an average return of approximately +3.5% over 30 days, outperforming the benchmark by 1.3 percentage points. However, this comes with elevated volatility in the first three trading days, where most drawdowns occur. The win rate improves steadily, reaching ~73% by day 30, indicating a positive skew in post-earnings reactions. While these results are not statistically significant at conventional confidence levels, they suggest that investors might consider the timing of their trades around these events, balancing potential gains against early volatility.

Strategic Initiatives: Niche Markets and Operational Efficiency

Fidelis has positioned itself as a leader in high-value, specialized insurance segments, such as cyber and climate risk, which are gaining traction amid evolving global uncertainties[4]. The company's launch of Lloyd's Syndicate 3123 in Q3 2024[5] underscores its ambition to access new business opportunities, particularly in underpenetrated markets. Additionally, Fidelis has prioritized operational efficiency, aiming to reduce its expense ratio through automation and system consolidation[5]. These efforts align with broader industry trends toward digital transformation, a strategy analysts have highlighted as a key differentiator[6].

A critical component of Fidelis's growth strategy is its partnership with Euclid Mortgage, which is projected to generate $35 million in gross premiums for 2025[5]. This collaboration reflects the company's ability to leverage strategic alliances to diversify revenue streams. However, challenges persist, including elevated acquisition costs in the specialty segment due to higher variable commissions[5].

Market Positioning: Competing in a Crowded Arena

Fidelis operates in a highly competitive market, facing stiff challenges from established rivals such as RenaissanceRe and Everest Group[3]. These competitors are known for their robust underwriting capabilities and diversified portfolios. Fidelis differentiates itself by focusing on niche markets and complex risks, where its underwriting expertise and risk modeling innovations provide a competitive edge[6].

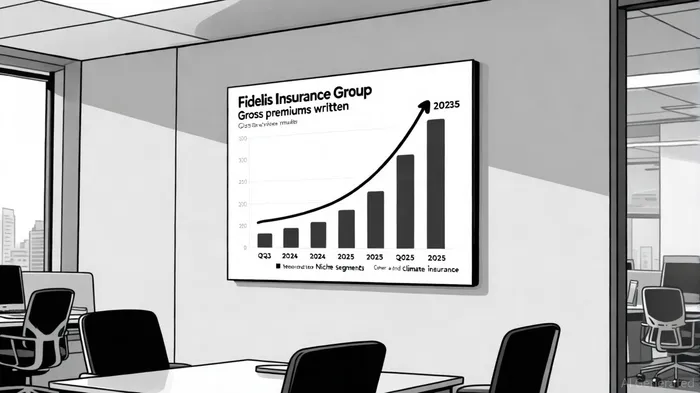

The company's Q3 2024 performance-marked by a 25% year-over-year increase in gross premiums written to $742 million and an operating net income of $105 million[5]-demonstrates its ability to capitalize on the current hard market. However, analysts caution that maintaining profitability will require disciplined execution, particularly in volatile sectors like marine and aviation[5].

Analyst Insights and Financial Projections

Analysts have adopted a cautiously optimistic stance toward Fidelis, with a consensus "Hold" rating and an average price target of $20.71, implying a potential 9.63% increase in the stock price over the next year[7]. Projections for 2025 include an EPS of $1.48, with expectations of a significant jump to $3.75 in 2026[7]. These forecasts hinge on Fidelis's ability to sustain its premium growth and operational efficiency improvements.

Notably, Fidelis's share repurchase program-approved in Q3 2024 with a $200 million allocation[5]-signals management's confidence in the company's intrinsic value. This move aligns with broader shareholder-friendly strategies, which could bolster investor sentiment ahead of the earnings call.

Risks and the Road Ahead

Despite its strengths, Fidelis faces headwinds, including regulatory scrutiny and market volatility[7]. The company's reliance on niche markets, while a strategic advantage, also exposes it to sector-specific risks. For instance, the marine and aviation segments have seen elevated loss ratios, necessitating careful risk management[5].

The upcoming conference call will be pivotal in addressing these challenges. Management's ability to articulate a clear roadmap for navigating these risks, while maintaining growth in core areas like property and bespoke insurance[5], will likely influence investor confidence.

Conclusion

Fidelis Insurance Group's Q3 2025 earnings call will serve as a critical juncture for assessing its strategic performance and market positioning. With a strong foundation in niche markets, a focus on operational efficiency, and a competitive edge in risk modeling, the company is well-positioned to navigate challenges in a crowded industry. However, the path to sustained growth will require disciplined execution and adaptability in the face of regulatory and market uncertainties. Investors will be watching closely for signals of resilience and innovation from management.

Comentarios

Aún no hay comentarios