Ferguson's Strategic Shift and Earnings Outperformance Signal Long-Term Growth Potential

In a macroeconomic environment marked by inflationary pressures and supply chain volatility, FergusonFERG-- (NYSE: FERG) has distinguished itself through disciplined capital allocation and strategic market positioning. The industrial distributor's third-quarter 2025 results underscore its ability to navigate headwinds while delivering robust financial performance, with net sales rising 4.3% year-over-year to $7.6 billion and an operating margin of 9.4%—a 20-basis-point expansion[1]. This outperformance reflects a recalibration of priorities that balances shareholder returns with long-term growth, positioning the company to capitalize on evolving demand in the maintenance, repair, and operations (MRO) sector.

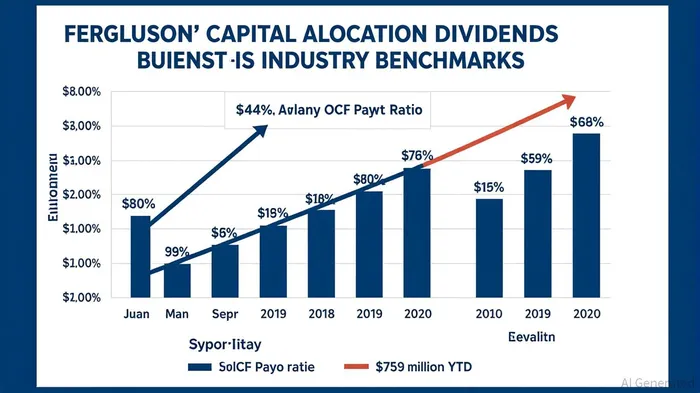

Capital Allocation: Balancing Returns and Resilience

Ferguson's capital allocation strategy has evolved to prioritize flexibility and sustainability. For the quarter, the company returned $251 million to shareholders via share repurchases and maintained a quarterly dividend of $0.83 per share, a 5% increase from the prior year[1]. While the operating free cash flow (OFCF) payout ratio stands at 44%, a level analysts deem sustainable[2], the company has increasingly leaned on buybacks to enhance per-share value. Year-to-date, $759 million has been allocated to repurchases, supported by a $1 billion extension of its authorization in March 2025[2]. This shift aligns with broader industry trends, as the average U.S. publicly traded company distributes 23% of earnings to shareholders[3], but Ferguson's approach—prioritizing buybacks over dividends during periods of cash flow volatility—demonstrates a nuanced understanding of shareholder preferences.

The company's liquidity position further reinforces confidence in its capital return strategy. With $519 million in cash and equivalents and a $1.5 billion undrawn credit facility[1], Ferguson has the flexibility to navigate macroeconomic uncertainty while funding strategic initiatives. Notably, it fully repaid a $500 million term loan, reducing leverage to a net debt-to-adjusted EBITDA ratio of 1.2x[4], a level that balances debt management with growth opportunities.

Market Positioning: Leveraging High-Growth Segments

Ferguson's strategic focus on high-margin, high-growth segments within the MRO industry has been pivotal to its outperformance. The U.S. segment, which accounts for the majority of its revenue, saw 4.5% sales growth in Q3, driven by non-residential demand in large capital projects and civil infrastructure[1]. The HVAC customer group, in particular, delivered 10% revenue growth, fueled by geographic expansion and counter-conversion initiatives[5]. These efforts align with broader industry tailwinds: the global MRO distribution market, valued at $673 billion in 2024, is projected to grow at a 2.8% CAGR through 2034[6], driven by industrial and manufacturing sector demand.

Ferguson's recent acquisitions and product diversification further strengthen its positioning. Three acquisitions in Q3 expanded its HVAC and Waterworks portfolios[4], while the newly launched Ferguson Home initiative targets residential renovation markets—a sector that now accounts for 40% of its sales[7]. This diversification mitigates exposure to cyclical fluctuations in commercial construction and positions the company to benefit from the $400 billion U.S. home improvement market[8].

Strategic Restructuring: Driving Efficiency

Operational efficiency remains a cornerstone of Ferguson's strategy. The company incurred $68 million in non-recurring charges in Q3 for branch consolidations and workforce reductions[1], initiatives expected to generate $100 million in annualized savings. These cost-saving measures, combined with margin expansion to 31.0%[1], highlight a disciplined approach to managing deflationary pressures and optimizing pricing power. Such restructuring is critical in an industry where gross margins typically hover around 25-30%[9], underscoring Ferguson's ability to outperform peers through operational rigor.

Future Outlook: Navigating Uncertainty with Confidence

Ferguson's full-year guidance—low to mid-single-digit revenue growth and an operating margin range of 8.5% to 9.0%—reflects cautious optimism[1]. The company plans to invest $300 million to $350 million in capital expenditures, targeting digital transformation and supply chain modernization[5]. These investments, paired with its focus on HVAC and Waterworks, position Ferguson to capture market share in sectors with structural growth potential.

Conclusion

Ferguson's strategic shift—from a capital-intensive growth model to a balanced approach emphasizing shareholder returns and operational efficiency—has enabled it to outperform in a challenging macro environment. By leveraging high-growth segments, executing disciplined acquisitions, and maintaining a robust liquidity position, the company is well-positioned to sustain its momentum. For investors, Ferguson's combination of resilient cash flow, strategic flexibility, and industry-leading margin expansion offers a compelling case for long-term value creation.

Comentarios

Aún no hay comentarios