Ferguson Enterprises' $750M Senior Unsecured Notes Offering: A Strategic Move for Capital Structure Optimization and High-Yield Investor Confidence

Ferguson Enterprises Inc.'s recent $750 million senior unsecured notes offering, announced in October 2024, represents a calculated step toward optimizing its capital structure while navigating a challenging high-yield debt market. The issuance of 5.000% notes due 2034, priced at a yield that reflects investor appetite for mid-cap industrial debt, underscores the company's ability to balance growth ambitions with financial prudence.

Capital Structure Optimization: Leverage Metrics and Strategic Refinancing

According to a report by the company's investor relations division, Ferguson's net debt to adjusted EBITDA ratio stood at 1.1x as of July 31, 2025, a metric that remains well within the “investment-grade” range for industrial firms[1]. This low leverage, combined with a debt-to-equity ratio of 0.88[3], suggests a capital structure that prioritizes flexibility. The $750M offering, while increasing total debt to $4.3 billion by Q2 2025 from $3.9 billion[1], is strategically positioned to prepay existing term loans and fund long-term growth initiatives.

The offering also follows a significant corporate restructuring in 2024, wherein FergusonFERG-- redomesticated its parent company to the United States, shifting from a Jersey-based entity[3]. This move likely enhanced the company's credit profile by aligning its governance and tax structures with U.S. market expectations, a critical factor for high-yield investors. By assuming the role of parent guarantor, Ferguson EnterprisesFERG-- Inc. streamlined its obligations, reducing complexity in its capital structure and potentially improving covenant terms[3].

Investor Confidence in High-Yield Markets

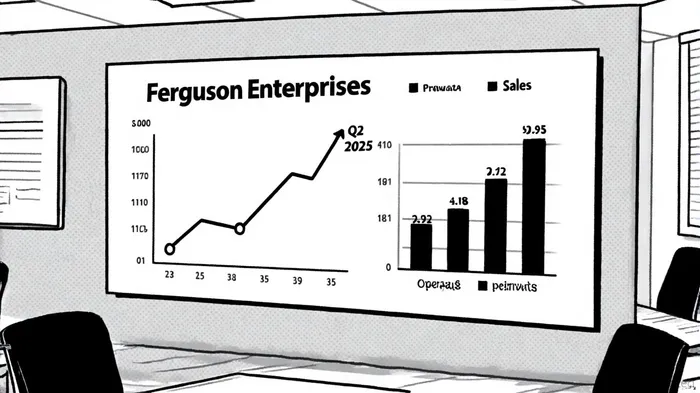

The 5% coupon on the 2034 notes, while modest compared to recent volatile market conditions, reflects strong demand for industrial sector debt. As stated by Bloomberg, the notes were priced at a spread that aligns with mid-tier investment-grade benchmarks, indicating investor confidence in Ferguson's stable cash flows[2]. The company's recent financial performance further supports this optimism: for the fiscal year ending July 31, 2025, Ferguson reported a 3.8% sales increase to $30.8 billion and a 59% surge in diluted earnings per share to $9.32[1].

However, Q2 2025 results revealed margin pressures, with operating profit declining 14% to $410 million due to 2% price deflation in the U.S. market[1]. This highlights the delicate balance between leveraging debt for growth and maintaining profitability. The proceeds from the notes offering, intended for general corporate purposes, could mitigate short-term margin compression by refinancing higher-cost debt or funding margin-enhancing acquisitions.

Risks and Long-Term Implications

While the offering strengthens Ferguson's liquidity, investors must monitor its ability to sustain EBITDA growth. A 0.7% drop in gross margin during Q2 2025[1] signals vulnerability to input cost inflation and competitive pricing pressures. If sales growth slows, the company's net debt/EBITDA ratio could rise beyond 1.5x, triggering tighter covenant constraints. Yet, given its current leverage profile and robust cash flow generation ($685 million in net operating cash flow for the first half of 2025[1]), Ferguson retains ample capacity to service its debt.

Conclusion

Ferguson's $750M notes offering exemplifies disciplined capital structure management in a high-yield environment. By leveraging its investment-grade profile to secure favorable terms, the company positions itself to navigate macroeconomic headwinds while funding strategic initiatives. For investors, the transaction underscores the importance of aligning debt maturities with long-term cash flow visibility—a lesson particularly relevant in today's rate-sensitive markets.

Comentarios

Aún no hay comentarios