Federated Hermes Premier Municipal Income Fund (FMN): A Tax-Advantaged Income Play Amid Shifting Leverage Dynamics?

The Federated HermesFHI-- Premier Municipal Income Fund (FMN) has emerged as a focal point for income investors seeking tax-advantaged yields in a volatile market environment. Recent developments, including a modest dividend increase and shifts in its leverage costs, have sparked debate about whether FMNFMN-- presents a compelling opportunity—or a risky proposition. This analysis evaluates FMN's appeal through the lens of its dividend dynamics, valuation metrics, leverage structure, and credit quality, offering insights for income-focused investors.

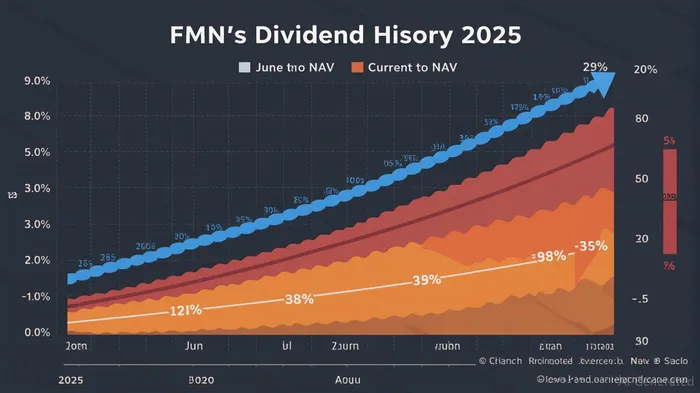

The Dividend Catalyst: A Modest Hike, But Meaningful for Tax Efficiency

FMN's June 2025 dividend increase to $0.0450 per share from $0.0400—a $0.0050 rise—marks a strategic pivot as the fund capitalizes on declining leverage costs and accumulated undistributed income. While the hike is small in absolute terms, its significance lies in its tax-free nature for federal income and AMTAMT-- purposes. The trailing 12-month yield of 4.5% (as of June 2025) positions FMN competitively against taxable bond alternatives, especially for investors in high tax brackets.

However, the fund's dividend history reveals volatility. Over the past three years, FMN has raised dividends three times but cut them twice, underscoring the fragility of income streams in a closed-end fund (CEF) structure. Investors should note that dividend sustainability hinges on FMN's ability to manage its leverage costs and portfolio returns.

Valuation: A Discounted Entry Point, but Risks Linger

FMN currently trades at a 7.78% discount to its NAV ($11.73 share price vs. $12.72 NAV as of July 2025), aligning with its historical average of around -12% over the past year. This discount creates a potential buying opportunity for long-term investors, particularly if the fund's performance improves. However, CEF discounts can widen sharply during market stress, as seen in 2020.

Leverage Structure: A Double-Edged Sword

FMN's 37.72% effective leverage ratio—driven by $88.6 million in preferred shares and $17.1 million in debt—amplifies both rewards and risks. The recent dividend increase was partly enabled by lower leverage costs, but this structure carries inherent dangers:

- Volatility Multiplier: Changes in FMN's NAV are magnified for common shareholders, as preferred shareholders absorb no risk. A 1% drop in NAV could translate to a larger loss for investors.

- Income Uncertainty: Preferred shares carry variable dividend rates, which could squeeze common shareholders' payouts if rates rise.

- Credit Exposure: Up to 20% of assets are allocated to non-investment-grade securities (“junk bonds”), introducing liquidity and default risks.

Credit Quality and Interest Rate Dynamics

FMN's portfolio includes state and municipal bonds, with credit ratings from agencies like S&P and Moody'sMCO--. While these ratings apply only to the underlying securities, they offer some comfort. However, the 20% allocation to non-investment-grade bonds remains a wildcard.

The fund's recent dividend boost reflects lower leverage costs, a trend that could persist if interest rates stabilize or decline. Conversely, rising rates might reverse this benefit, tightening the fund's profit margins.

Tax Efficiency: A Key Selling Point

FMN's tax-exempt status is its standout feature. Dividends are free from federal income tax and AMT, though state taxes may still apply. For investors in high-tax states like California or New York, this advantage could offset risks.

Risks to Consider

- Leverage-Induced Volatility: FMN's shares could swing sharply if interest rates rise or credit markets sour.

- Discount Widening: CEF discounts often expand during market downturns, eroding returns.

- Credit Downgrades: A default in the non-investment-grade portion of the portfolio could pressure NAV and dividends.

Investment Recommendation

FMN presents a mixed picture for income investors:

- Bull Case: The current discount and tax-free yield make it attractive for long-term holders willing to tolerate volatility. The recent dividend increase signals management's focus on income stability, and Federated Hermes' $839.8 billion asset base adds operational credibility.

- Bear Case: Leverage and credit risks could backfire if rates rise or economic conditions deteriorate.

Actionable Takeaway:

- Buy: Investors seeking tax-free income and willing to accept moderate leverage risk may find FMN's 7.78% discount appealing. Monitor the discount trend and leverage costs closely.

- Avoid: Aggressive investors or those averse to CEF risks should steer clear until the fund's leverage ratio or credit quality improves.

Final Thoughts

FMN's recent dividend hike and valuation discount offer a tantalizing entry point for income-focused investors, particularly those in high tax brackets. Yet its reliance on leverage and exposure to junk bonds demands vigilance. As interest rates stabilize and municipal markets recover, FMN could reward patience—but investors must remain mindful of its structural risks. Always pair this holding with broader diversification to mitigate concentrated exposure to municipal debt and leverage-driven volatility.

Comentarios

Aún no hay comentarios