The Fed's Rate-Cutting Riddle: How Inflation Data and Jobs Reports Shape Equity Market Volatility

The Federal Reserve faces a classic balancing act: tame inflation without smothering a labor market that, while slowing, still shows signs of resilience. With the latest CPI data and August jobs report in hand, investors must grapple with a pivotal question: How should equity portfolios be positioned ahead of the next rate-cutting decision? The answer lies in dissecting the interplay between sticky inflation, softening employment, and historical market behavior.

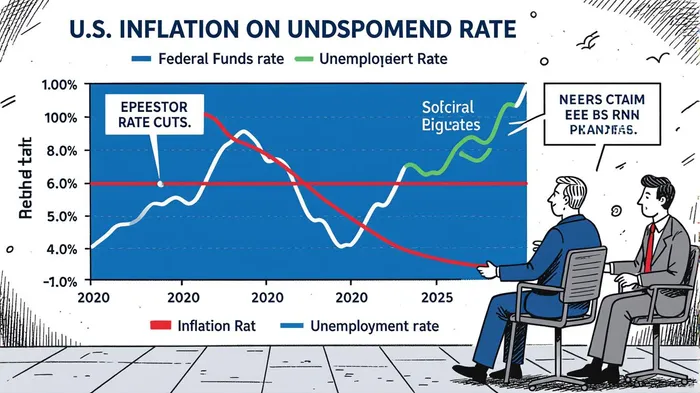

The Inflation Conundrum: Core CPI Sticks Above 3%

. While energy prices have cooled, —particularly in healthcare, housing, and transportation—continues to drag on household budgets. The Fed's 2% target feels like a distant mirage, yet the central bank is unlikely to overreact to short-term volatility. Tariff-driven price pressures and supply chain bottlenecks are still embedded in the system, and the Fed's dual mandate demands a careful calibration.

The Jobs Report: A Labor Market Losing Steam

The August nonfarm payrolls report delivered a jolt. , . While healthcare and social assistance sectors added jobs, manufacturing and wholesale trade saw significant declines. .

This data amplifies the case for a September rate cut. , . The Fed's dilemma? Cutting too aggressively risks reigniting inflation, while delaying could deepen labor market weakness.

Historical Precedent: Rate Cuts and Sectoral Shifts

History offers a playbook. During the 2001 dot-com crash and 2008 , rate cuts initially stabilized markets but failed to prevent prolonged downturns. However, .

Key lessons for 2025:

1. outperform: Utilities, real estate, and healthcare have historically gained during rate-cutting cycles due to their stable cash flows.

2. face headwinds.

3. matters.

Strategic Portfolio Positioning: Navigating the Riddle

Given the Fed's likely September cut, investors should adopt a dual strategy:

- Defensive tilt: Overweight utilities (e.g., NextEra Energy), healthcare (e.g., UnitedHealth Group), and real estate (e.g., Prologis). These sectors benefit from lower discount rates and stable demand.

- Quality large-cap exposure: Focus on companies with strong balance sheets and predictable earnings, such as MicrosoftMSFT-- and Johnson & Johnson.

- Hedge against volatility: Allocate to short-duration bonds and gold to offset potential equity market swings.

Avoid overexposure to rate-sensitive sectors like industrials and consumer discretionary. While the Fed's easing may eventually boost growth stocks, the path will be bumpy.

The Road Ahead: Risks and Opportunities

The Fed's credibility is at stake. Politically motivated rate cuts—such as those potentially influenced by —could undermine long-term inflation control. Additionally, a prolonged labor market slowdown might force the Fed to cut more aggressively than markets expect, creating a "buy the dip" scenario for equities.

Final Takeaway

The Fed's rate-cutting riddle is far from solved, but the data points to a September easing. Investors who position portfolios for a defensive, quality-driven approach will be better prepared for the volatility ahead. As always, stay nimble—markets rarely follow scripts, and the Fed's next move could reshape the landscape overnight.

Comentarios

Aún no hay comentarios