Fed's Rate-Cut Gambit: Navigating a Cooling Labor Market and Sectoral Shifts

The Federal Reserve's September 2025 decision to cut the federal funds rate by 25 basis points to 4.00–4.25% marked a pivotal shift in monetary policy, responding to a labor market that has cooled sharply. With nonfarm payrolls adding just 22,000 jobs in August—well below the 75,000 forecast and a stark decline from the upwardly revised 79,000 in July—the U.S. economy is signaling fragility[3]. The unemployment rate rose to 4.3%, driven by a combination of weak job creation and a shrinking labor force participation rate[1]. These developments, compounded by a massive downward revision of 911,000 jobs in the 12 months through March 2025, underscore a labor market that is far weaker than previously understood[1].

A Policy Pivot Amid Diverging Signals

The Fed's rate cut reflects a delicate balancing act. While inflation remains elevated, the central bank has prioritized addressing the labor market's deterioration. The decision to cut rates—though smaller than the 50-basis-point reduction advocated by dissenting governor Stephen Miran—signals a growing consensus that further tightening would risk a sharper slowdown[1]. The Summary of Economic Projections now anticipates two more cuts in 2025 and one in 2026, a trajectory that aligns with the Fed's dual mandate of price stability and maximum employment[3].

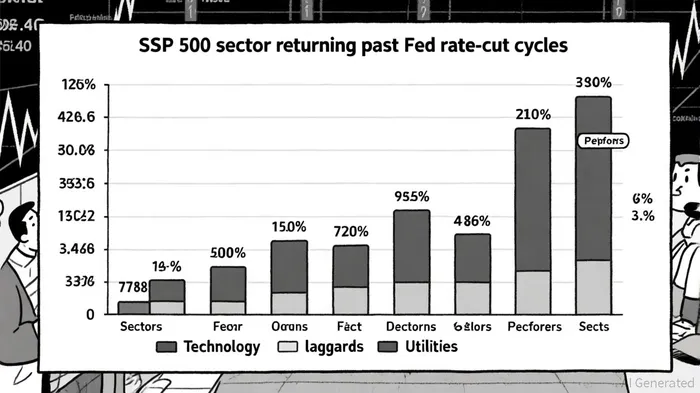

Historically, such easing cycles have yielded mixed outcomes. The 1995 rate cuts, for instance, preceded a robust market rally, with the S&P 500 returning 19.93% annually in the year following the first reduction[4]. Conversely, the 2019–2020 cycle, which included three rate cuts before the pandemic-induced recession, saw the Technology sector outperform due to secular trends like AI adoption, while Energy and Utilities lagged[1]. These divergent outcomes highlight the importance of macroeconomic context in shaping the efficacy of rate cuts.

Sectoral Implications: Winners and Losers

The September 2025 rate cut is poised to reshape sector dynamics. Sectors sensitive to borrowing costs, such as Real Estate and Homebuilding, stand to benefit as mortgage rates decline, potentially reigniting demand for housing and construction[2]. Similarly, Consumer Discretionary stocks could thrive as lower rates boost disposable income and spending on non-essentials.

Technology and growth stocks are also likely beneficiaries. Lower discount rates enhance the present value of future earnings, a critical factor for high-growth companies. This dynamic mirrors the 2019–2020 period, when AI-driven innovation propelled Tech sector gains despite broader economic headwinds[1].

Conversely, Financials face headwinds. Banks and insurers, which rely on net interest margins, may see profitability erode as rate spreads compress. Savers, too, will contend with diminished returns on cash instruments like money market funds[2].

Investment Positioning: Lessons from History

Investors navigating this rate-cut cycle should consider historical patterns. During the 1995 easing, sectors with strong balance sheets—such as Health Care and Utilities—outperformed, while Financials struggled[4]. In contrast, the 2019–2020 cycle saw Consumer Cyclical stocks gain traction as the economy showed early signs of strength[1].

The current environment suggests a hybrid approach. While the Fed's easing aims to avert a recession, persistent inflation and weak labor market data introduce uncertainty. A diversified portfolio emphasizing Technology, Real Estate, and Consumer Discretionary—while hedging against Financials—could position investors to capitalize on both cyclical and secular trends.

Conclusion: A Delicate Tightrope

The Fed's rate-cut cycle is a response to a labor market that has proven more fragile than initially reported. While historical data offers guidance, the path ahead remains uncertain. Investors must weigh the potential for a soft landing against the risk of prolonged inflation or a sharper slowdown. As the central bank continues to navigate this tightrope, sectoral positioning will be key to capturing opportunities in a shifting economic landscape.

Comentarios

Aún no hay comentarios