The Fed's Policy Path: Why a Major Easing Cycle Remains Distant

The Federal Reserve's policy trajectory in 2025 remains anchored by a complex interplay of inflationary pressures, labor market fragility, and political dynamics. Despite persistent calls for monetary easing, the central bank's cautious approach underscores the likelihood of a prolonged tightening cycle. This analysis examines the structural and political headwinds constraining policy flexibility, the mixed signals from regional labor markets, and the implications for investors navigating a high-interest-rate environment.

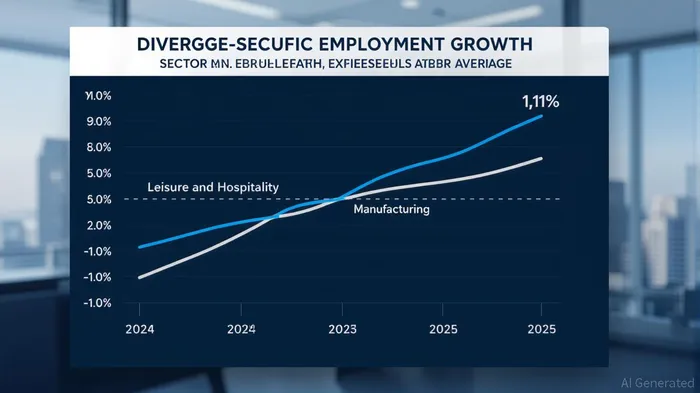

Labor Market Divergence and Policy Constraints

Recent employment data from the Dallas-Fort Worth-Arlington metropolitan area highlights the uneven recovery across sectors. Total nonfarm employment surged by 46,800 jobs year-over-year in May 2025, driven by gains in leisure and hospitality, education, and health services [2]. However, declines in professional and business services and manufacturing sectors reveal underlying fragility. Such divergence complicates the Fed's assessment of national labor conditions, as regional disparities may mask broader trends. For instance, while the national average job growth rate of 1.1% aligns with the Dallas-Fort Worth experience, sector-specific weaknesses—particularly in manufacturing—signal vulnerabilities that could reignite inflationary pressures if left unaddressed.

The Federal Reserve's September 2025 Beige Book further underscores this tension, noting anecdotal reports of “modest wage growth in service sectors but persistent price pressures in goods-producing industries” [2]. These mixed signals reinforce the central bank's reluctance to pivot toward easing, as premature rate cuts risk destabilizing hard-won progress in curbing inflation.

Inflationary Pressures and Policy Uncertainty

The absence of granular September 2025 CPI/PCE data complicates precise inflation forecasting, but broader trends suggest lingering risks. The widespread implementation of Trump-era tariffs has exacerbated supply-side bottlenecks, pushing up input costs and embedding inflationary expectations into long-term contracts [2]. According to a report by the Bureau of Labor Statistics, the typical release schedule for CPI data (mid-October) means September 2025 figures will remain unavailable until late Q4 [1]. This lag creates a policy blind spot, forcing the Fed to rely on forward-looking indicators such as producer price indices and wage growth, which currently point to a “stickier” inflation environment than previously anticipated.

Moreover, the confirmation of Stephen Miran—a top economic adviser to President Trump—as a Federal Reserve governor on September 15, 2025, has introduced political uncertainty. Miran's dual role in the White House (on unpaid leave) and the Fed raises questions about the central bank's independence, particularly as Trump's protectionist policies continue to distort price signals. While the Fed's dual mandate of stable prices and full employment remains unchanged, Miran's appointment may delay consensus on rate cuts, as policymakers navigate the delicate balance between political influence and economic pragmatism [2].

Market Expectations and Investment Implications

Despite these challenges, financial markets have priced in a modest probability of rate cuts by mid-2026, as reflected in Fed funds futures. However, this optimism may be premature. Historical precedents suggest that central banks often overcorrect in response to inflation, extending tightening cycles beyond initial forecasts. For example, the Fed's 2023-2024 rate hikes were prolonged by persistent services-sector inflation, a pattern that could repeat in 2025 given the current policy environment.

Investors should prioritize risk management strategies that account for prolonged tightening. Defensive asset classes—such as short-duration bonds and equities in sectors insulated from interest rate sensitivity (e.g., healthcare and utilities)—offer resilience in a high-rate environment. Conversely, cyclical sectors like industrials and real estate face headwinds from elevated borrowing costs and geopolitical uncertainties tied to Trump's trade policies.

Conclusion

The Federal Reserve's policy path in 2025 is shaped by a confluence of structural and political factors that delay the onset of a major easing cycle. While regional labor markets show pockets of strength, sectoral imbalances and inflationary tailwinds necessitate a measured approach. For investors, this environment demands a focus on liquidity, diversification, and sectoral selectivity to mitigate risks in a landscape where monetary policy normalization remains elusive.

Comentarios

Aún no hay comentarios