Fed Policy Divergence: Navigating the New Monetary Landscape for Tactical Gains

The Federal Reserve's divergent policy path in 2023–2025 has created a seismic shift in global financial markets, forcing investors to rethink their tactical allocations. While the ECB, BoE, and BoJ have embraced rate cuts to stimulate growth or combat deflation, the Fed has stubbornly clung to higher rates, prioritizing inflation control over economic momentum. This divergence isn't just a technicality-it's a game-changer for currencies, bonds, and equities. Let's break it down.

The Fed's Lone Stand: A Policy Divergence Unveiled

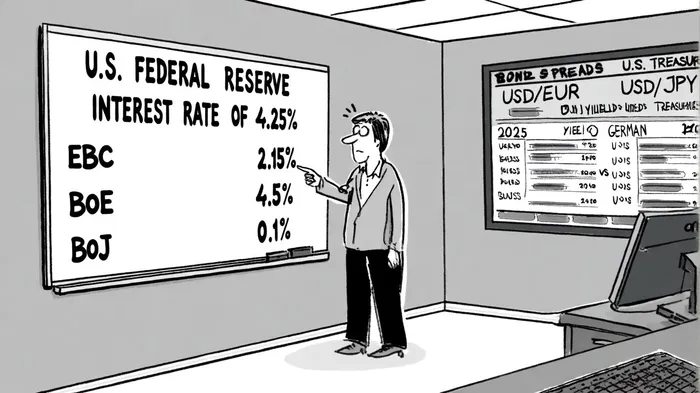

According to a Forbes report, the Fed's refusal to join the ECB and BoE in aggressive rate cuts has left U.S. interest rates significantly higher than their European counterparts. As of June 2025, the Fed's target rate remains at 4.25%, while the ECB slashed its rate to 2.15% and the BoE trimmed its rate by 75 basis points since mid-2024. Meanwhile, the BoJ's ultra-loose policy-stuck at 0.1%-has exacerbated yield differentials, creating a "Goldilocks" scenario where U.S. assets appear both safe and lucrative, as noted by Saffron Capital.

This divergence isn't accidental. The Fed's hawkish stance reflects its battle with sticky inflation and the looming threat of tariff-driven price pressures, while the ECB and BoE have prioritized growth in weaker eurozone and UK economies, according to a BIS working paper. The result? A U.S. dollar that's held its ground against the euro and yen, and Treasury yields that tower over European and Japanese bonds-trends highlighted in Saffron Capital's tactical piece.

Currency Wars: Dollar Dominance and the Cost of Divergence

The Fed's policy divergence has turbocharged the U.S. dollar's strength. Data from the Federal Reserve's 2024 analysis shows that unexpected U.S. rate hikes or prolonged hawkish stances correlate with dollar rallies against the euro and yen, even as global risk appetite wanes (discussed in the Forbes report). For investors, this means hedging strategies are now critical. A dollar-long position could amplify returns in U.S. equities and bonds but risks underperformance in international markets.

The ECB's rate cuts, meanwhile, have softened the euro, making European exports more competitive but squeezing import-dependent sectors. The BoJ's inaction has left the yen as a "currency of convenience," with Japanese investors flocking to higher-yielding U.S. assets-a trend that could accelerate if the BoJ finally tapers its yield curve control, as Saffron Capital's analysis suggests.

Bonds and Equities: The New Yield Hierarchy

The Fed's higher-for-longer rates have pushed U.S. Treasury yields above 4.5%, creating a stark contrast with European and Japanese bonds. As noted by the BIS, U.S. monetary policy shocks have asymmetrically influenced global bond yields, with tightening cycles causing hump-shaped increases in the 5–10 year segment. This has made intermediate-duration bonds (3–7 years) a sweet spot for income seekers, a point echoed in investor portfolio guides.

Equity markets, however, are split. Growth stocks-particularly in AI infrastructure and software-have thrived on lower discount rates, while value sectors face headwinds from higher borrowing costs. Saffron Capital's analysis underscores a rotation into quality growth equities and small-cap cyclicals, provided macroeconomic data stabilizes. International equities, meanwhile, are gaining traction as the dollar weakens, offering diversification and exposure to global growth (as the Forbes report describes).

Tactical Allocations: Balancing the Divergence

To capitalize on this environment, investors must adopt a multi-asset playbook:

1. Bonds: Focus on intermediate-duration Treasuries and investment-grade corporates to balance income and rate risk. Avoid long-end duration, which is vulnerable to Fed policy shifts.

2. Equities: Overweight U.S. growth stocks (tech, AI) and international equities (Europe, Asia) for diversification. Defensive sectors like healthcare and utilities offer resilience in a stagflationary scenario.

3. Real Assets: Gold and real estate are must-haves. Gold benefits from falling real rates, while real estate thrives on cheap financing and inflation hedging (points raised in the Forbes report).

4. Currencies: Hedge dollar exposure in international portfolios, but consider dollar-long positions for U.S.-centric strategies.

The Road Ahead: When Will the Fed Join the Herd?

The Fed's reluctance to cut rates until late 2025 or early 2026 hinges on inflation data and trade policy outcomes. If tariffs spark a surge in import prices, the Fed may be forced to pivot. Until then, investors should prepare for a prolonged period of divergence. As Atlantic Council's Econographics blog notes, the ECB's rate-cutting cycle is likely to end by mid-2025, while the BoE may follow the Fed's cautious path (the BIS working paper discusses related dynamics).

In this fragmented landscape, agility is key. Diversify across asset classes, stay nimble with sector rotations, and keep a close eye on the Fed's next move. After all, in markets, it's not just about where rates are-it's about where they're going.

References (first mentions linked in text):

- Forbes report: https://www.forbes.com/councils/forbesfinancecouncil/2024/03/28/fed-versus-ecb-a-comparison-of-monetary-policies-over-the-last-year/

- Saffron Capital analysis: https://saffroncapital.com/2025/08/positioning-for-fed-rate-cuts-tactical-allocations/

- BIS working paper: https://www.bis.org/publ/work1195.htm

Comentarios

Aún no hay comentarios