The Fed's Inflation Concerns and Their Implications for Equity and Fixed Income Markets

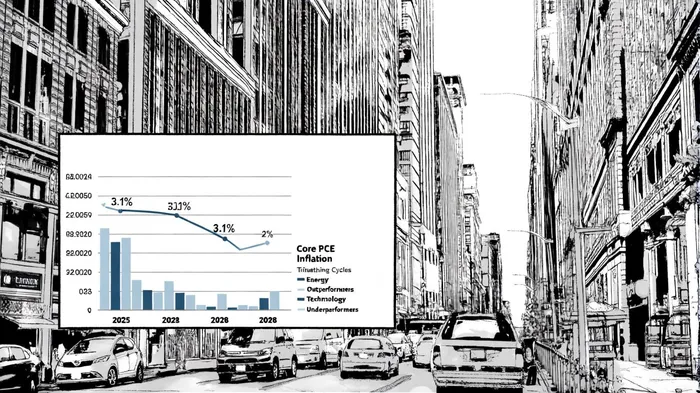

The Federal Reserve's September 2025 Summary of Economic Projections reveals a prolonged inflationary trajectory, with core PCE inflation expected to remain above 2% until 2028. The median projection of 3.1% for 2025 underscores persistent pressures in housing and wage growth, delaying the disinflation process [1]. This extended timeline has significant implications for equity and fixed income markets, particularly as the Fed navigates a tightening policy environment with a projected federal funds rate decline from 3.6% in 2025 to 3.1% by 2028 [2].

Historical Sector Rotation in Tightening Cycles

Historical data from 12 Fed tightening cycles since 1965 reveals consistent patterns in sectoral performance. During tightening phases, sectors with high sensitivity to interest rates—such as financials and energy—tend to outperform, while growth-oriented sectors like technology often underperform [3]. For example, during the 2022–2025 tightening cycle, energy stocks surged over 50% as inflationary pressures and supply constraints drove demand for commodities, whereas technology stocks faced sharp corrections due to rising discount rates [5].

Conversely, easing cycles historically favor equities and fixed income. A report by JPMorganJPM-- notes that non-recessionary rate-cutting periods have delivered positive returns for both asset classes, with large-cap and quality stocks outperforming small-cap and cyclical peers [3]. This dynamic is evident in the current cycle, where the Fed's September 2025 rate cut of 25 basis points triggered a rally in the S&P 500 and Russell 2000, as reduced borrowing costs boosted small-cap profitability and refinancing opportunities [2].

Recent Sector Performance and Strategic Implications

The 2022–2025 tightening cycle has amplified sectoral divergences. Growth stocks in technology, such as Microsoft and NVIDIA, have rebounded post-rate cuts due to lower discount rates enhancing the present value of future earnings [2]. Meanwhile, consumer discretionary stocks have benefited from sustained spending, reflecting the U.S. economy's resilience amid tightening [2].

However, the banking sector faces headwinds as lower rates threaten net interest margins, a concern highlighted by Wedbush analysts [3]. Similarly, commercial real estate may see a rebound, with CBRE projecting a 15% increase in investment volume as borrowing costs decline [5]. For investors, these dynamics underscore the importance of sector rotation strategies. Historical evidence suggests that disciplined rotation—shifting capital to defensive sectors like healthcare and utilities during tightening—can enhance risk-adjusted returns, with some strategies outperforming buy-and-hold by 2.8% annually [1].

Navigating Risk-Adjusted Returns

A balanced approach to portfolio construction is critical. During tightening cycles, prioritizing quality and profitability—favoring large-cap over small-cap stocks—can mitigate volatility. For fixed income, short-duration bonds are better positioned to capitalize on falling rates, while equities in sectors like energy and financials offer upside potential [4].

The Fed's prolonged inflation trajectory also necessitates vigilance. While the labor market softening and rate cuts have spurred optimism, the D'Amico and King model warns that downward pressure on GDP and CPI remains underappreciated, particularly in employment [1]. Investors must monitor leading indicators such as the ISM PMI and yield curve inversion risks to time rotations effectively [1].

Conclusion

The Fed's inflation concerns and gradual policy normalization are reshaping market dynamics. By leveraging historical sector rotation patterns and adapting to current macroeconomic signals, investors can optimize risk-adjusted returns. As the Fed's easing cycle gains momentum, a strategic tilt toward growth stocks, small-cap equities, and short-duration fixed income appears warranted—provided the economic expansion holds. However, the path forward remains contingent on the Fed's ability to balance inflation control with growth preservation, a challenge that will define market rotations in the years ahead.

Comentarios

Aún no hay comentarios