Fastenal's Q3 2025 Earnings: A Resilient Player in a Transforming Industrial Distribution Sector

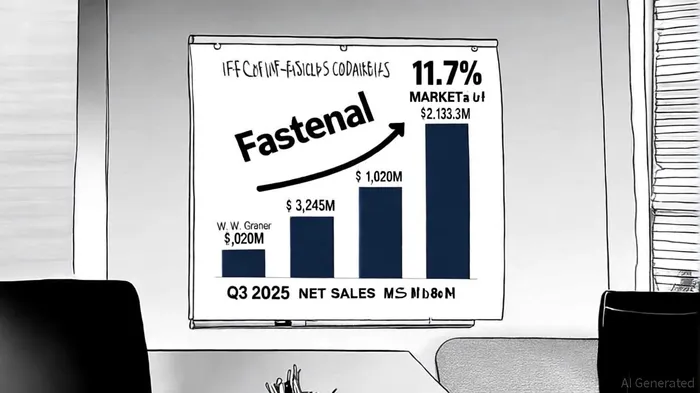

Fastenal Co. (FAST) delivered a standout performance in Q3 2025, reporting net sales of $2,133.3 million-a 11.7% year-over-year increase-and net income of $335.5 million, up 12.6% from the prior year, according to Fastenal's Q3 earnings release. These results underscore the company's ability to navigate a challenging industrial landscape while outpacing broader market trends. As the industrial distribution sector faces headwinds such as a contracting manufacturing environment and rising input costs, Fastenal's strategic focus on digital transformation and customer acquisition positions it as a compelling player in a $8.43 trillion market projected to grow at a 5.41% CAGR through 2030, according to an industrial distribution market report.

Competitive Positioning: Fastenal's Strengths in a Fragmented Market

Fastenal's Q3 performance reflects its disciplined approach to market share expansion. The company added 15.4% more high-value customers (those spending $50K+ monthly), growing its base from 2,401 to 2,771 sites, the Q3 release said. This metric is critical in an industry where customer retention and cross-selling drive profitability. By contrast, larger rivals like W.W. Grainger (market share: 5.91%) and MSC Industrial Direct (1.33%) have seen slower growth in recent quarters, according to CSIMarket data. Fastenal's 2.86% market share, while smaller than Grainger's, is bolstered by its agility in adopting digital tools to optimize inventory and enhance customer experience, according to an industry trends report.

The industrial distribution sector is undergoing a digital renaissance, with companies leveraging AI-driven analytics and e-commerce platforms to streamline operations. Fastenal's investment in its digital infrastructure-evidenced by improved product availability in distribution centers-has directly contributed to its sales growth, as the Q3 release notes. Meanwhile, competitors like Grainger are focusing on mergers and acquisitions to scale, a strategy that carries higher integration risks. Fastenal's organic growth model, combined with its 12.3% increase in diluted EPS to $0.29 reported in Q3, suggests a more sustainable path in a sector where operational efficiency is paramount.

Navigating Industry Challenges: Resilience Amid Contraction

The U.S. industrial manufacturing environment remains fragile, with the PMI averaging 48.6 in Q3 2025-a contractionary reading the company noted in its Q3 release. Yet FastenalFAST-- managed to grow 75% of its sales in manufacturing, a segment typically sensitive to macroeconomic shifts. This resilience contrasts with broader industry trends, where distributors are grappling with workforce shortages and volatile input costs for materials like steel and copper, as highlighted in the industry trends report. Fastenal's ability to maintain margins despite these pressures-its operating margin expanded to 15.7% in Q3-highlights its pricing power and supply chain agility, the Q3 release shows.

The company's focus on nearshoring and domestic production aligns with sector-wide efforts to mitigate global supply chain risks, as noted in a Top 7 industrial trends piece. While larger players like Grainger have diversified through international acquisitions, Fastenal's localized distribution network reduces exposure to geopolitical uncertainties. This strategy also resonates with growing ESG (Environmental, Social, and Governance) priorities, as domestic logistics lower carbon footprints-a factor increasingly valued by institutional investors.

Investment Implications: A Strong Earnings Catalyst

Fastenal's Q3 results validate its position as a top-tier industrial distributor, but the company's growth trajectory depends on its ability to sustain innovation. The industrial distribution sector is expected to grow at a 5.41% CAGR through 2030, according to the industrial distribution market report, driven by automation and infrastructure spending. Fastenal's digital-first approach positions it to capture a larger slice of this growth, particularly as smaller competitors struggle with legacy systems.

However, risks remain. The sector's reliance on manufacturing demand means Fastenal's performance could soften if the PMI remains below 50. Additionally, rising interest rates may pressure capital-intensive rivals, though Fastenal's strong cash flow ($335.5M net income) provides a buffer. For investors, the key takeaway is Fastenal's disciplined execution: its 11.7% sales growth outpaced the sector's projected CAGR, and its customer-centric strategy has created a durable competitive moat.

Comentarios

Aún no hay comentarios