FactSet's Valuation and Operational Challenges: A Case for Undervaluation in the Data Analytics Sector

In the rapidly evolving data and analytics sector, identifying undervalued firms requires a nuanced understanding of both financial metrics and operational dynamics. FactSetFDS-- (FDS), a leader in financial data and analytics, presents a compelling case for investors seeking opportunities amid broader market shifts. While the company has demonstrated resilience in revenue growth and client expansion, its valuation metrics and operational challenges suggest it may be undervalued relative to peers like MSCIMSCI-- and S&P GlobalSPGI--.

Financial Performance: Growth Amid Margin Pressures

FactSet's Q4 2025 results underscored its ability to navigate a competitive landscape. GAAP revenues rose 6.2% year-over-year to $596.9 million, driven by robust growth in institutional buy-side and wealth segments[1]. Organic Annual Subscription Value (ASV) reached $2.37 billion, reflecting a 5.7% year-over-year increase[1]. However, profitability metrics tell a more complex story. GAAP operating margins expanded to 29.7% in Q4, up 700 basis points from the prior year, but adjusted operating margins dipped to 33.8% due to higher technology expenses and a lower bonus accrual[1]. For fiscal 2025, GAAP operating margins hit 32.2%, yet adjusted margins fell to 36.3%, signaling underlying cost pressures[2].

Earnings per share (EPS) growth remained strong, with GAAP diluted EPS surging 73.7% to $4.03 and adjusted EPS rising 8.3% to $4.05 in Q4[1]. However, the stock dropped 6.62% post-earnings after missing adjusted EPS forecasts, reflecting investor concerns about margin sustainability[3]. Historical backtesting of FDS's performance following earnings misses since 2022 reveals that while the immediate reaction is typically negative, the stock has shown modest mean reversion over time. On average, FDSFDS-- shares declined by -0.16% on the first trading day after a miss but recovered to post a +1.81% return over a 30-day window, outperforming the S&P 500 benchmark[4].

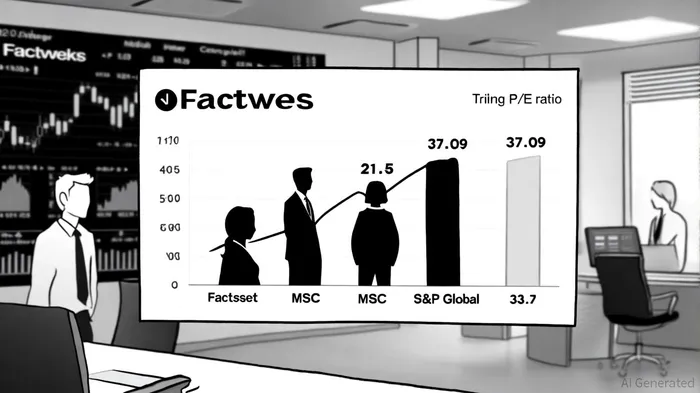

Peer Comparison: A Valuation GapGAP-- Emerges

FactSet's valuation metrics starkly contrast with those of its peers. As of September 2025, FactSet's trailing P/E ratio stood at 21.5, significantly lower than MSCI's 37.09 and S&P Global's 33.7[4]. MSCI, for instance, reported Q1 2025 operating revenues of $745.8 million, a 9.7% year-over-year increase, with operating margins of 50.6% and an adjusted EBITDA margin of 57.1%[5]. S&P Global, meanwhile, maintained a P/S ratio of 10.26 and a P/B ratio of 3.97, but its operating margin of 34.51% lagged behind MSCI's performance[6].

FactSet's EV/EBITDA ratio of 22.86 for fiscal 2025[2] appears reasonable compared to MSCI's 27.56[5], suggesting a more attractive valuation for investors prioritizing earnings multiples. Yet, FactSet's margin compression—particularly in adjusted operating income—raises questions about its ability to match the profitability of peers.

Operational Challenges: Navigating AI Disruption and Client Constraints

FactSet's leadership has emphasized AI integration and client diversification as strategic priorities[2]. While AI contributed meaningfully to Q4 sales, the company faces headwinds from extended sales cycles and rigorous client approval processes[3]. Higher technology expenses and a conservative 2026 guidance (4–6% ASV growth and $2.423–$2.448 billion in GAAP revenues[1]) reflect these challenges.

Moreover, FactSet operates in a sector where client budget constraints and AI-driven disruption are reshaping demand. Competitors like MSCI have leveraged asset-based fee growth (up 18.1% in Q1 2025[5]) to offset these pressures, while S&P Global's diversified revenue streams provide stability. FactSet's focus on wealth and institutional segments, though growing, may limit its exposure to higher-margin opportunities.

The Case for Undervaluation

Despite these challenges, FactSet's fundamentals suggest it is undervalued. Its 5.7% ASV growth and 9.5% year-over-year client count increase[1] demonstrate organic traction, while its 6% dividend hike in May 2025[2] underscores commitment to shareholder returns. The stock's recent underperformance—driven by short-term margin concerns—may have created an entry point for long-term investors.

Relative to peers, FactSet's lower P/E ratio and EV/EBITDA suggest the market is discounting its growth potential. If the company can stabilize adjusted operating margins and capitalize on AI-driven efficiencies, its valuation could converge with industry averages.

Conclusion

FactSet's operational challenges and valuation gap present a nuanced investment opportunity. While margin pressures and competitive dynamics persist, its strong revenue growth, strategic AI initiatives, and undervalued metrics make it a compelling candidate for investors seeking exposure to the data analytics sector. As the market recalibrates to broader AI and macroeconomic shifts, FactSet's ability to balance innovation with profitability will be critical to unlocking its full potential.

Comentarios

Aún no hay comentarios