Value Factor ETFs Outperform S&P 500: Structural Undervaluation and Cyclical Re-Rating Potential

The Resurgence of Value: A Structural Shift or Cyclical Fluke?

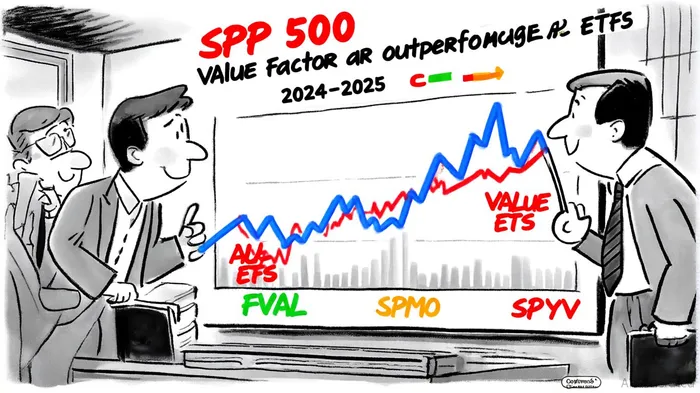

The past two years have witnessed a dramatic reversal in the fortunes of value factor ETFs, with many outperforming the S&P 500 despite macroeconomic headwinds. According to a report by Forbes Advisor, value ETFs like the Fidelity Value Factor ETF (FVAL) and Invesco S&P 500 Momentum ETF (SPMO) have delivered annualized returns of 7.55% and 18.4%, respectively, from 2023 to 2025—far exceeding the S&P 500's 12.9% over the same period [1]. This outperformance, however, is not merely a function of luck. It reflects a deeper structural undervaluation of value stocks and a re-rating driven by macroeconomic repositioning.

Structural Undervaluation: The Foundation for Re-Rating

Value ETFs have historically traded at discounts to their intrinsic worth, a trend exacerbated by the low-interest-rate environment post-2020. As noted by Research Affiliates, the prolonged underperformance of value stocks since 2007—part of a "longer and deeper drawdown" than historical cycles—has created a fertile ground for re-rating [2]. This undervaluation is particularly pronounced in sectors like technology and healthcare, where traditional metrics like book-to-market ratios fail to capture the value of intangible assets [3]. For instance, FVAL's focus on high-growth sectors with sound balance sheets has allowed it to capitalize on this mispricing, delivering robust returns even amid volatility [1].

The structural discount is further supported by valuation metrics. The Vanguard Value ETF (VTV), with a price-to-earnings (P/E) ratio of 25.9 and a 2% yield, trades at a significant discount to the S&P 500's P/E of 30.3 and 1.3% yield [4]. This gap suggests that value stocks are being priced for pessimism, offering a margin of safety for investors willing to ride out short-term turbulence.

Macroeconomic Drivers: Rate Cuts and Sector Rotation

The Federal Reserve's rate-cutting cycle, which began in mid-2025, has accelerated the re-rating of value stocks. Historically, value stocks—particularly large-cap ones with strong cash flows—outperform during rate-cutting periods due to their resilience to interest rate fluctuations [5]. For example, the SPDR Portfolio S&P 500 Value ETF (SPYV), with its low 0.04% expense ratio and exposure to large-cap value stocks, has gained 9.11% over three years, outpacing the S&P 500's 3.7% return in 2025 [1].

Sector rotation has also played a critical role. The VanEck Semiconductor ETF (SMH), which combines value and momentum characteristics, has surged 24.7% annually over five years, driven by AI demand and macroeconomic stabilization [1]. Similarly, the Financial Select Sector SPDR Fund (XLF), with a P/E of 17, has benefited from a strong economic environment and favorable interest rate projections [4]. These trends underscore how value ETFs are not just reacting to macroeconomic shifts but actively shaping them.

Cyclical Re-Rating: A Long-Term Play

While short-term gains are compelling, the long-term re-rating potential of value ETFs is even more significant. Academic research suggests that the underperformance of value stocks since 2007 may be cyclical rather than structural [2]. For instance, the Morningstar US Value Index outperformed the US Growth Index by over 9 percentage points in 2025, signaling a potential inflection point [5]. This re-rating is further supported by the historical outperformance of value stocks—$131,534 versus $11,744 for growth stocks since 1926—indicating that the current undervaluation is likely temporary [6].

Investors seeking to capitalize on this re-rating should focus on ETFs with diversified, low-cost exposure to both domestic and international value stocks. The Dimensional International Value ETF (DFIV), for example, offers access to small- and mid-cap value stocks outside the U.S., with a 20.8% one-year return and a 3.56% yield [6]. Such funds provide a hedge against U.S.-specific risks while tapping into global value opportunities.

Conclusion: A Strategic Case for Value

The outperformance of value factor ETFs relative to the S&P 500 is not a fluke but a reflection of structural undervaluation and macroeconomic repositioning. As interest rates normalize and sector-specific tailwinds gain momentum, value ETFs are poised to deliver sustained returns. For investors, the key lies in selecting ETFs that balance low costs, diversified exposure, and sector-specific re-rating potential. In a market increasingly defined by volatility and uncertainty, value investing is proving to be a resilient and rewarding strategy.

Comentarios

Aún no hay comentarios