Evaluating North West Company's 2.5% Dividend Hike Amid Q2 Earnings Softness

The market is always watching for companies that can defy the odds—especially when it comes to dividend growth. North West Company’s recent 2.5% dividend hike, announced despite Q2 earnings softness, has sparked debate. But let’s cut through the noise: this move is not reckless. It’s a calculated bet on a company that has systematically fortified its financial foundation over the past five years.

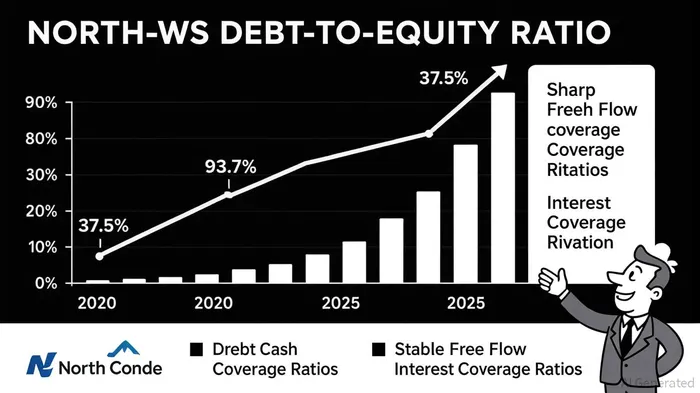

Debt Reduction: The Unsung Hero of Dividend Resilience

North West’s debt-to-equity ratio has plummeted from a bloated 93.7% in 2020 to a manageable 37.5% as of Q2 2025 [1]. This isn’t just a number—it’s a testament to disciplined capital management. With total shareholder equity of CA$783.3MMMM-- and total liabilities of CA$722.5M, the company’s balance sheet now boasts a net asset position of CA$60.8M [2]. This structural shift means North West is no longer a high-risk bet; it’s a stable, cash-flow-driven entity.

Cash Flow Coverage: The Real Engine of Sustainability

A healthy dividend requires more than just earnings—it needs robust cash flow. North West’s operating cash flow comfortably covers its debt obligations, with a coverage ratio of 91.7% [1]. Even more compelling is its interest coverage ratio of 11.9x [2], which indicates the company can easily service its CA$293.9M in debt. These metrics suggest that even if earnings dip further, the dividend remains well-anchored.

Payout Ratios: A Balancing Act

Critics might argue that a 2.5% dividend hike strains North West’s finances. But the data tells a different story. The company’s dividend payout ratio sits at 55% [3], well below the 75% threshold that typically raises red flags [4]. This leaves ample room for growth without jeopardizing financial stability. For context, a 55% payout ratio means North West retains 45% of its earnings to reinvest in operations, pay down debt, or weather economic headwinds.

Resilience in a Tough Climate

Let’s not ignore the broader picture. North West operates in a cyclical retail sector, yet its cash reserves—CA$74.3M in short-term investments [2]—provide a buffer against downturns. The company’s total assets of CA$1.5B also dwarf its liabilities, creating a margin of safety that few peers can match. In an era of rising interest rates and inflationary pressures, this kind of financial fortitude is rare.

The Verdict: A Dividend Hike with Legs

North West’s 2.5% dividend hike is a signal of confidence—not hubris. The company has done its homework: it’s de-leveraged, cash-flow secure, and operating with a payout ratio that leaves room for both growth and prudence. For income-focused investors, this is a stock that checks all the boxes. Yes, Q2 earnings were soft, but the underlying business is stronger than ever. In a market where dividends are under siege, North West is a rare winner.

Source:

[1] North West (NWC) Balance Sheet & Financial Health Metrics [https://simplywall.st/stocks/ca/consumer-retailing/tsx-nwc/north-west-shares/health]

[2] NWC.CA | North West Co. Inc. Financial Statements [https://www.wsj.com/market-data/quotes/CA/XTSE/NWC/financials?gaa_at=eafs&gaa_n=ASWzDAgyl9nYclWL1-PEUb_ZvoNsy5_eFkdEt7HOHAg9Y88sNVpDkEg7dR87&gaa_sig=H-5Ez7ELVmWZ72k-2u6cQL_oFbUMQM5_EVZz547uQprD9YIAxflaamQCUMbj7vURFFXJHWUDPs78qVPMPGXRVg%3D%3D&gaa_ts=68bfaf6e]

[3] North West (TSX:NWC) Dividend Yield, History and Growth [https://simplywall.st/stocks/ca/consumer-retailing/tsx-nwc/north-west-shares/dividend]

[4] North West (NWC) Stock Price, News & Analysis [https://www.marketbeat.com/stocks/TSE/NWC/]

Comentarios

Aún no hay comentarios