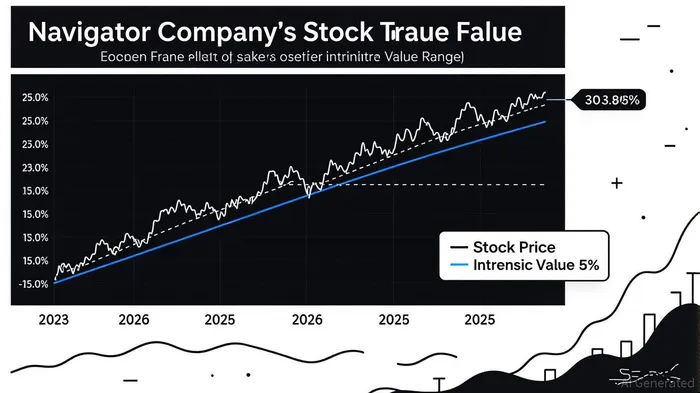

Re-evaluating Navigator Company’s Intrinsic Valuation Amid Muted Price Action

The Navigator CompanyNVGS-- (ENXTLS:NVG) has long been a subject of debate among value investors, oscillating between periods of optimism and skepticism. As of September 2025, the stock has experienced muted price action, trading 30.8% below its estimated fair value [1]. This divergence between intrinsic valuation and market price warrants a closer look, particularly given the company’s robust financial metrics and forward-looking growth projections.

Valuation Metrics: A Case for Undervaluation

Navigator’s trailing price-to-earnings (PE) ratio of 11.01 and forward PE of 9.20 position it as a discount relative to broader market averages [2]. These figures suggest that the market is pricing in pessimism about future earnings, despite the company’s strong operational performance. The enterprise value-to-sales (EV/Sales) ratio of 1.53 and EV/EBITDA of 6.95 further underscore its affordability, as both multiples are well below historical averages for the materials sector [2].

From a solvency perspective, Navigator’s debt-to-equity ratio of 0.74 and interest coverage ratio of 9.1 indicate a healthy balance sheet, capable of weathering economic headwinds [2]. Meanwhile, profitability metrics like a 15.84% return on equity (ROE) and 7.85% return on invested capital (ROIC) highlight efficient capital allocation and operational discipline [2]. These fundamentals collectively suggest that the company’s intrinsic value is not only intact but potentially undervalued by current market pricing.

Operational Performance: Mixed Signals

Navigator’s recent earnings reports tell a nuanced story. First-quarter 2025 results showed a dip in earnings per share (EPS) to €0.068 from €0.09 in the same period in 2024 [1]. However, Q2 2025 results painted a more optimistic picture: the company exceeded expectations, reporting EPS of €0.31 against a forecast of €0.32 and revenue of $146.67 million versus an estimate of $133.48 million [2]. Fleet utilization improved to 90% in July 2025 from 84% in Q2, signaling operational resilience [2].

The conflicting data—where one source cites a 9.38% EPS surprise [2] and another claims a -61.11% earnings shortfall [3]—highlights the need for caution. Such discrepancies may stem from differing methodologies or timing of data collection. Investors should await the July 24, 2025, Q2 earnings release to clarify these inconsistencies [1].

Future Outlook: Growth Potential vs. Market Realities

Analysts project NavigatorNVGS-- to grow earnings by 6% annually and revenue by 2.6%, with EPS expanding at 1% per year [2]. These forecasts, coupled with a projected ROE of 16.1% in three years [2], suggest a path to value creation. However, the company’s intrinsic value estimates vary widely: some models suggest it is 54–78% above the current share price [1], while others imply a 30.8% discount [1]. This range reflects uncertainty about macroeconomic conditions and the company’s ability to execute its ammonia-fueled carrier investments [2].

Strategic Considerations for Investors

Navigator’s intrinsic valuation appears compelling, but investors must weigh several factors:

1. Debt Management: While the debt-to-equity ratio is manageable, rising interest rates could pressure leverage metrics.

2. Capital Allocation: The company’s $50 million share repurchase program and dividend payouts demonstrate shareholder-friendly policies, but reinvestment in ammonia-fueled carriers may require additional capital.

3. Market Volatility: The materials sector remains sensitive to commodity cycles, which could amplify price swings.

Conclusion

Navigator Company’s intrinsic valuation suggests a compelling risk-reward profile for long-term investors. With a forward PE of 9.20, strong profitability metrics, and a projected ROE of 16.1%, the stock appears undervalued relative to its fundamentals [2]. However, recent earnings volatility and conflicting data points necessitate a wait-and-see approach. Investors who can tolerate short-term uncertainty may find Navigator’s muted price action an opportunity to acquire a fundamentally sound business at a discount—provided the company can sustain its operational momentum and capitalize on its strategic investments.

Source:

[1] Navigator Company (ENXTLS:NVG) - Stock Analysis, [https://simplywall.st/stocks/pt/materials/eli-nvg/navigator-shares]

[2] Navigator Company Future Growth, [https://simplywall.st/stocks/pt/materials/eli-nvg/navigator-shares/future]

[3] Navigator HoldingsNVGS-- (NVGS) Q2 Earnings and Revenues Lag, [https://finance.yahoo.com/news/navigator-holdings-nvgs-q2-earnings-215502449.html]

Comentarios

Aún no hay comentarios