Evaluating Independence Realty Trust's (IRT) Dividend Sustainability and Strategic Position in Non-Gateway Markets

In the current rising interest rate environment, income-focused investors face a critical question: Can real estate investment trusts (REITs) like Independence Realty TrustIRT-- (IRT) maintain their dividend payouts while delivering long-term growth? IRTIRT--, a multifamily REIT with a 3.77% yield, has positioned itself in non-gateway U.S. markets, a strategy that could insulate it from the volatility of coastal economies. However, its dividend sustainability hinges on a delicate balance between cash flow generation and leverage management.

Dividend Sustainability: A Double-Edged Sword

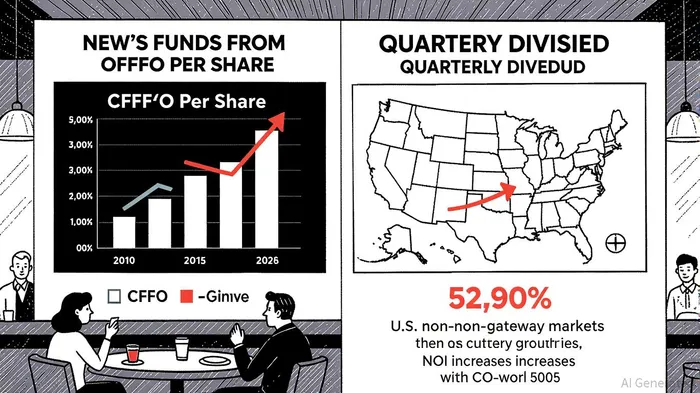

IRT’s quarterly dividend of $0.17 per share, which translates to an annual payout of $0.68, appears robust on the surface. Yet, the company’s payout ratio—calculated using Core Funds from Operations (CFFO) rather than net income—stands at 52% for Q2 2025 [1]. This metric, while high, is more representative of a REIT’s operational cash flow than net income, which for IRT was a mere $0.03 per share in the same period [1]. By contrast, peer Realty Income CorporationO-- (O) operates with a payout ratio of 308.01% based on net income, highlighting IRT’s relative prudence [2].

However, IRT’s leverage remains a concern. Its net debt-to-adjusted EBITDA ratio of 5.9x at year-end 2024 [3] suggests moderate debt levels for a REIT but leaves room for improvement. Rising interest rates could strain fixed-rate liabilities, reducing free cash flow and increasing refinancing risks. For context, AT&T’s recent $3.1 billion free cash flow and $119.1 billion net debt illustrate the scale of liquidity challenges in high-rate environments [4]. IRT’s BBB credit rating and renewed unsecured credit line provide some cushion, but its interest coverage ratio—indicating how well earnings cover interest payments—remains under pressure [5].

Strategic Position in Non-Gateway Markets

IRT’s focus on non-gateway markets like Atlanta, Louisville, Memphis, and Raleigh offers a compelling counterpoint to its leverage risks. These Sunbelt and Midwest regions have seen robust population migration and economic growth, driving 3.2% same-store net operating income (NOI) growth in 2024 [3]. The company’s value-add program, which renovated 1,671 units at a 15.7% return on investment, further amplifies its growth potential [3].

This strategy contrasts with peers like Federal Realty Investment TrustFRT-- (FRT-PC), which targets affluent submarkets in non-gateway areas but relies more heavily on retail assets [6]. IRT’s multifamily focus aligns with demographic trends, as millennials and remote workers increasingly prioritize affordability and access to emerging job hubs. While IRT’s 0.44% revenue growth for the 3MMMM-- period ending March 2025 lags slightly behind industry benchmarks [5], its disciplined capital allocation and lower market saturation in non-gateway areas suggest long-term upside.

Interest Rate Sensitivity and Risk Mitigation

Rising rates pose a dual threat to IRT: higher borrowing costs and reduced asset valuations. The company’s exposure to fixed-rate debt could amplify these risks, as its cash conversion cycle (CCC)—a measure of liquidity efficiency—becomes more critical in high-rate environments [7]. However, IRT’s 2025 guidance for earnings per diluted share ($0.19–$0.22) and CFFO per share ($1.16–$1.19) indicates confidence in maintaining its payout [3]. Analysts remain cautiously optimistic, with a 12-month price target averaging $22.50 [5], though the stock’s market cap remains below industry averages [5].

Conclusion: A High-Yield Bet with Caveats

IRT’s 3.77% yield and non-gateway strategy make it an attractive income play for investors willing to tolerate moderate leverage risks. Its CFFO-based payout ratio of 52% is sustainable in the short term, particularly given its strong same-store performance and value-add initiatives. However, the REIT’s interest rate sensitivity and relatively high payout ratio compared to peers like RLJ Lodging TrustRLJ-- (forecasted to raise dividends by 13.3% in Q3 2025) [8] warrant caution. For those seeking a balance between income and growth, IRT’s strategic positioning in high-growth Sunbelt markets could justify the risks—provided the company continues to execute its renovation programs and debt refinancing plans effectively.

Source:

[1] Independence Realty Trust Announces Second Quarter 2025 Financial Results [https://investors.irtliving.com/press-releases/press-release/2025/Independence-Realty-Trust-Announces-Second-Quarter-2025-Financial-Results/default.aspx]

[2] Realty Income Corporation (O) Dividend Date & History [https://www.koyfin.com/company/o/dividends/]

[3] Independence Realty Trust Announces Fourth Quarter and Full Year 2024 Financial Results [https://investors.irtliving.com/press-releases/press-release/2025/Independence-Realty-Trust-Announces-Fourth-Quarter-and-Full-Year-2024-Financial-Results/default.aspx]

[4] AT&T Delivers Strong First-Quarter Financial Performance [https://about.att.com/story/2025/1q-earnings.html]

[5] 4 Analysts Have This To Say About Independence Realty Trust [https://www.nasdaq.com/articles/4-analysts-have-say-about-independence-realty-trust]

[6] Federal Realty Investment Trust (FRT-PC) Q2 2025 Earnings Call Transcript [https://mlq.ai/stocks/FRT-PC/earnings-call-transcript/Q2-2025]

[7] 10 Cash Flow Metrics Every Business Must Track [https://ramp.com/blog/cash-flow-metrics]

[8] 18 US REITs forecast to boost dividends in Q3 2025 [https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/7/18-us-reits-forecast-to-boost-dividends-in-q3-2025-91428549]

Comentarios

Aún no hay comentarios