Evaluating Gamehaus Holdings (GMHS): Is the Share Buyback Justified Amid Volatility and Declining Revenue?

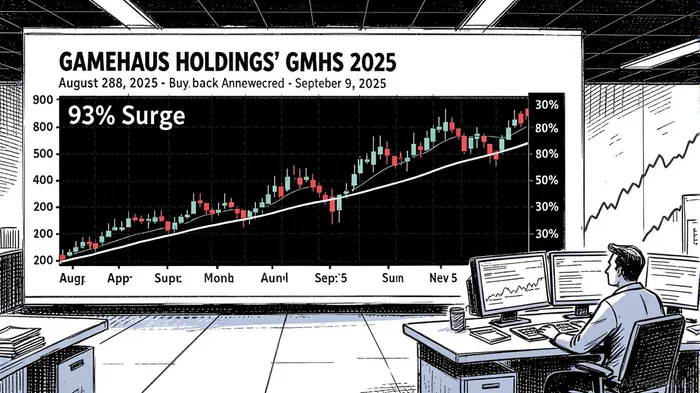

In late August 2025, Gamehaus HoldingsGMHS-- (GMHS) announced a $5 million share repurchase program, a move that sent its stock surging 93% in a single day[3]. The buyback, funded by existing cash reserves and operational cash flow, reflects management's belief that the stock is undervalued and aligns with its “balanced capital allocation strategy”[1]. However, this decision comes amid a backdrop of declining earnings in the first nine months of fiscal 2025 and heightened stock volatility. This analysis evaluates whether the buyback is a prudent strategic move or a risky gamble, focusing on valuation metrics, financial health, and long-term risks.

Strategic Risk: A Double-Edged Sword

Gamehaus's Q2 2025 results highlight both strengths and vulnerabilities. Revenue rose 48.37% year-over-year to $45.58 million, driven by growth in mobile gaming, while net income exploded by 3,787.97% to $3.05 million[4]. Yet, earnings for the nine months ending May 19, 2025, fell to $2.37 million from $5.69 million in the prior year[4]. This divergence suggests uneven performance across quarters, raising questions about the sustainability of growth.

The buyback program, while signaling confidence, introduces strategic risks. By allocating $5 million to repurchases, GamehausGMHS-- reduces its cash reserves, which stood at $18.52 million as of March 31, 2025[4]. While the company's debt-to-equity ratio of 0.01 underscores its financial flexibility[2], the high weekly stock volatility (27.5% average movement) could amplify downside risks if market conditions deteriorate[3]. A prolonged revenue slump or unexpected operational costs might strain liquidity, particularly if the buyback is executed at inflated prices during short-term rallies.

Valuation Analysis: A Discounted but Uncertain Proposition

Gamehaus's trailing P/E ratio of 18.8x is significantly lower than the peer average of 32.4x and the US Entertainment industry average of 36.7x[1]. This suggests the stock trades at a discount relative to competitors, potentially justifying the buyback as a value-creation tool. Chairman Feng Xie explicitly stated that the current share price “does not fully reflect the company's fundamentals or growth trajectory”[1], a common rationale for repurchase programs.

However, intrinsic value estimates remain elusive. Analysts have yet to assign price targets for GMHSGMHS-- in 2025[2], and discounted cash flow (DCF) models struggle to account for the company's recent revenue declines and strategic shifts, such as pivoting to RPG and puzzle genres[5]. The lack of consensus highlights uncertainty about future cash flows. Meanwhile, GameSquareGAME-- Holdings (GAME), a peer in the gaming sector, has a clearer valuation profile, with analysts projecting an 185.71% upside from its current price[5]. This contrast underscores the challenges investors face in assessing GMHS's long-term potential.

Management's Leverage: Confidence vs. Market Skepticism

The buyback announcement aligns with broader investor sentiment. Following the repurchase plan, analysts noted that Gamehaus was “demonstrating commitment to returning value to shareholders while maintaining flexibility for growth investments”[4]. Yet, the market's mixed reaction—while the stock surged post-announcement, underlying revenue trends remain weak—reflects skepticism.

A critical question is whether the buyback addresses structural issues. For instance, Gamehaus's reliance on virtual item sales and advertising exposes it to cyclical demand shifts. The company's recent cost-cutting measures and genre diversification aim to mitigate this, but their success is unproven[5]. The buyback, while beneficial for short-term shareholder value, may not resolve these vulnerabilities.

Conclusion: A Calculated Bet with Caveats

Gamehaus's $5 million buyback is a calculated move to stabilize its share price and signal confidence in its long-term prospects. The company's low leverage, strong Q2 performance, and discounted P/E ratio provide a rationale for the program. However, the declining nine-month earnings, high volatility, and lack of analyst coverage introduce significant uncertainty. Investors should monitor the Q4 2025 earnings report, scheduled for September 9, 2025[3], to gauge whether the buyback aligns with improved fundamentals. For now, the repurchase appears justified as a strategic hedge against undervaluation but carries risks if growth stagnates.

Comentarios

Aún no hay comentarios