Eurozone Resilience and Equity Opportunities in the Post-Election Landscape

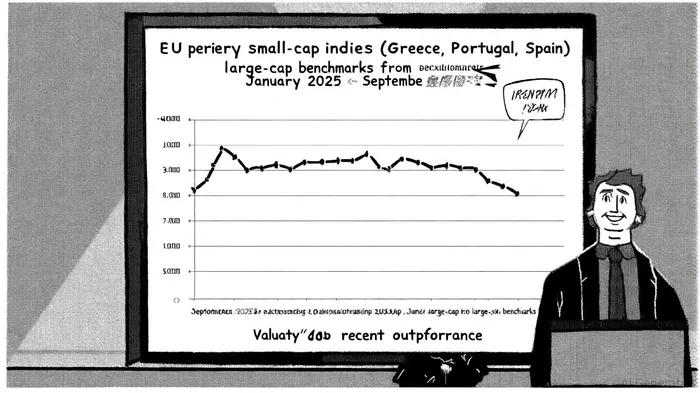

The post-2025 election landscape in the EU's southern periphery—Greece, Portugal, and Spain—has revealed a compelling narrative for small-cap equity investors. Despite broader eurozone stagnation, these markets are demonstrating resilience, driven by favorable valuations, policy tailwinds, and sector-specific growth catalysts. Small-cap stocks in these regions are trading at historically low forward earnings multiples (14.2x as of late 2024) compared to large-cap peers, creating a valuation gap that suggests potential for a rebound[4]. This undervaluation is compounded by structural reforms, EU recovery funding, and sectoral shifts toward renewable energy and infrastructure, which position small-cap firms as key beneficiaries of the region's economic rebalancing.

Valuation Arbitrage and Macroeconomic Catalysts

The EU periphery's small-cap markets have long been overlooked due to historical volatility and economic fragility. However, recent data indicates a shift. For instance, Greece's small-cap equities are trading at a 30% discount to their 10-year average price-to-earnings (P/E) ratio, supported by a surge in renewable energy investments and tourism-driven GDP growth[3]. Similarly, Portugal's small-cap value indices are at record lows relative to large-cap benchmarks, with analysts noting an inflection pointIPCX-- for earnings growth as the country achieves 81% renewable electricity generation in Q1 2025[5].

Policy interventions have further amplified this opportunity. The European Commission's Omnibus IV Simplification Package, which reduces regulatory burdens on small and mid-cap companies, is projected to save EU businesses €400 million annually in compliance costs[1]. In Spain, a 62% increase in grid investment caps through 2030—spurred by lessons from the April 2025 blackout—has accelerated funding for battery storage and green hydrogen projects[2]. These reforms create a fertile ground for small-cap firms to scale operations without the overhead constraints typical of larger corporations.

Sector-Specific Opportunities

Renewable Energy: Spain and Greece are leading the EU's green transition, with Spain targeting 76 GW of solar capacity by 2030 and Greece aiming for 82% renewable electricity generation[6]. Small-cap players like R Energy 1 (Greece) and Geoskop (Spain) are leveraging these targets to expand solar and wind projects. For example, R Energy 1's 600 MW offshore wind initiative in Evros, Greece, is backed by EU recovery funds, while Geoskop's climate intelligence platform is attracting institutional investors seeking data-driven renewable energy solutions[7].

Construction and Infrastructure: The Spanish construction sector is projected to grow by 3.9% in 2025, fueled by EUR67 billion in green transition funding under the Recovery and Resilience Plan[8]. Small-cap firms specializing in sustainable construction, such as BM2Solar (Portugal), are capitalizing on demand for energy-efficient buildings. In Spain, the 2025 grid modernization push has spurred activity in local distribution networks, with companies like Acciona Construcción securing contracts for smart grid upgrades[9].

Hospitality and Tourism: Portugal's hospitality sector, a cornerstone of its economy, has rebounded sharply post-2025 elections, with occupancy rates in Lisbon and Porto reaching 85% in Q2 2025[10]. Small-cap hoteliers and property developers, such as Nyab (Portugal), are benefiting from a surge in domestic and international tourism, supported by government incentives for green certifications and digitalization.

Risks and Mitigants

While the outlook is optimistic, challenges persist. High unemployment (12% in Spain and 9% in Portugal) and fragmented political dynamics in Spain's regional elections could dampen momentum[11]. However, these risks are offset by the EU's coordinated fiscal support and the inherent agility of small-cap firms to adapt to localized demand shifts. For instance, Greece's tourism-driven GDP growth of 5.9% in 2022[3] demonstrates how niche sectors can outperform despite macroeconomic headwinds.

Conclusion

The EU periphery's small-cap markets are emerging as a compelling asset class for investors seeking undervalued exposure to structural growth. With policy tailwinds, sector-specific catalysts, and a widening valuation gap, these markets offer a unique opportunity to capitalize on the eurozone's asymmetric recovery. As the ECB's rate-cut cycle and EU simplification measures gain traction, small-cap equities in Greece, Portugal, and Spain are poised to outperform, making them a cornerstone of a diversified European equity strategy.

Comentarios

Aún no hay comentarios