Eurozone Inflation Resurgence: Implications for Central Banks and Equities

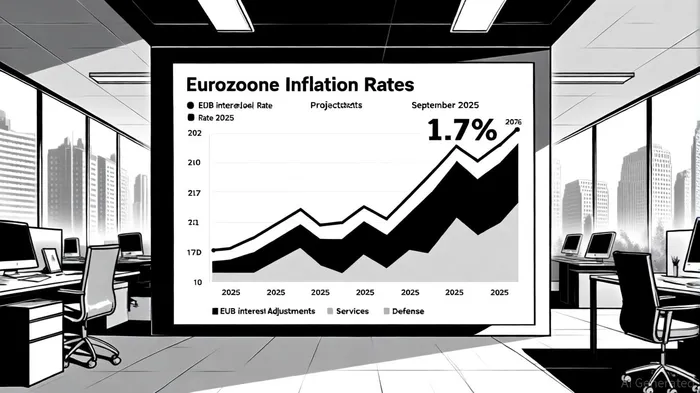

The Eurozone's inflation landscape in 2025 is marked by a delicate balancing act between subdued headline inflation and persistent structural pressures. According to UBSUBS--, the Eurozone inflation rate in September 2025 stood at 1.7% year-over-year, below the European Central Bank's (ECB) 2.3% third-quarter forecast[3]. This divergence signals a potential policy shift as the ECB weighs further rate cuts against the risk of renewed inflationary shocks from external factors such as U.S. tariffs and geopolitical tensions[2]. For investors, the implications span asset allocation strategies and sectoral exposure, with manufacturing, services, and defense sectors emerging as key battlegrounds.

Policy Shifts: From Inflation Control to Growth Support

The ECB's 2025 strategy reaffirms its 2% inflation target but adopts a more flexible approach to address fragmented inflation dynamics. UBS forecasts a total of 125 basis points in rate cuts by year-end, driven by soft inflation readings and slowing GDP growth[2]. This shift reflects the ECB's pivot from tightening to easing, as core inflation nears the target and domestic demand stabilizes[1]. However, the central bank remains cautious: while headline inflation moderates, localized pressures—such as Spain's construction boom and Germany's labor hoarding—threaten to rekindle inflationary risks[6].

The ECB's Transmission Protection Instrument (TPI) will play a critical role in mitigating market fragmentation. By stabilizing sovereign debt markets and preventing unwarranted borrowing cost spikes, the TPI indirectly supports both industrial and service sectors[4]. Yet, its effectiveness hinges on the ECB's ability to balance rate cuts with fiscal normalization, particularly in countries like France, where weak consumer demand could drag growth[3].

Sectoral Performance: Divergence and Resilience

The Eurozone's sectoral performance in Q3 2025 underscores the uneven impact of inflation and policy shifts. Export-dependent manufacturing sectors in Germany and Italy face headwinds from U.S. tariffs on steel and aluminum, which could reduce Eurozone GDP growth by 1.1%[2]. These tariffs are expected to push inflation upward as firms pass costs to consumers, creating a short-term drag on industrial equities[5]. Conversely, service sectors—particularly professional and healthcare services—have shown resilience, supported by robust labor markets and low unemployment rates[1].

Spain and Italy, meanwhile, are grappling with inflationary pressures from domestic factors. Spain's 3% inflation in 2025 is driven by capital-intensive construction projects, while Italy's headline inflation trends upward due to industrial sector investments[3]. These trends highlight the challenge of reconciling country-specific dynamics with the ECB's one-size-fits-all policy framework.

Defense-related equities, however, are bucking the trend. Increased EU and NATO spending—exemplified by Rheinmetall AG's performance—has bolstered defense stocks, with the European Defence Fund allocating €1.065 billion to bolster security[5]. This sector's growth is insulated from broader inflationary risks, making it a strategic allocation for investors seeking resilience in a volatile environment.

Investment Implications: Navigating Uncertainty

For asset allocators, the Eurozone's inflation resurgence demands a nuanced approach. In a “Soft landing” scenario—where inflation eases and growth holds steady—equities could gain up to 14%, particularly in services and defense[2]. Conversely, a “Stagflation” scenario—marked by persistent inflation and weak growth—could erode 10% from diversified portfolios[2]. The ECB's credibility in managing these outcomes will be pivotal.

Investors should prioritize sectors aligned with fiscal and defense spending while hedging against trade-related risks. Defensive plays in services and utilities may offer stability, while exposure to inflation-linked assets (e.g., real estate, infrastructure) can mitigate downside risks[3]. Additionally, the ECB's potential use of non-standard instruments, such as the TPI, could stabilize bond markets and enhance the relative value of government securities[1].

Conclusion

The Eurozone's inflation resurgence in 2025 is a tale of duality: subdued headline inflation coexists with structural pressures that challenge the ECB's policy framework. As central banks navigate this complexity, investors must remain agile, leveraging sectoral divergences and policy signals to optimize returns. The coming months will test the ECB's ability to balance growth and inflation, with equities and asset allocation strategies poised to reflect the outcomes of this delicate balancing act.

Comentarios

Aún no hay comentarios