Eurozone Fiscal Divergence Risks: Sovereign Bond Yield Spreads as Leading Indicators of Market Stress

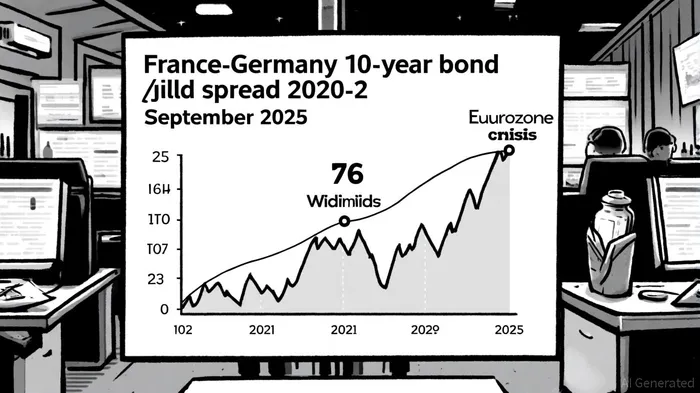

In the Eurozone, where fiscal unity has long been an aspiration rather than a reality, the widening gap between France's and Germany's 10-year sovereign bond yields has emerged as a stark warning sign. By September 2025, the spread had reached 76 basis points, its widest level in three weeks, driven by investor concerns over France's deteriorating fiscal health and political instability, as noted in a Tradeweb government bond update. This development underscores a troubling trend: the re-emergence of fiscal divergence as a systemic risk for the single currency bloc.

A Barometer of Distrust

Sovereign bond yield spreads have long served as a canary in the coal mine for Eurozone stability. The France-Germany spread, in particular, has historically reflected shifting perceptions of risk. As of September 2025, France's 10-year yield stood at 3.45%, compared to Germany's 2.71%, a differential that, while slightly lower than the 83.3 basis points recorded in late September, remains significantly above the long-term average of 0.71% (as shown in YCharts data), and has been described as the highest in more than a decade by Brussels Signal. This widening is not merely a statistical anomaly but a signal of deepening skepticism about France's ability to manage its €3.4 trillion debt load, which now carries a higher cost of borrowing than its German counterpart, according to TradingEconomics data.

The catalysts are clear. Fitch's downgrade of France's sovereign rating to A+ from AA- in September 2025, followed by Morningstar DBRS's cut to AA from AA (high), has amplified fears of a fiscal misstep, according to the Tradeweb update. Meanwhile, political turbulence-exemplified by a government lacking a parliamentary majority and a contentious budget vote-has further eroded confidence. As Bloomberg noted in August 2025, the spread climbed to 80 basis points amid speculation that Prime Minister Francois Bayrou's budget plan could face a confidence vote. Analysts warn that a further downgrade, particularly if Fitch acts on its scheduled review in late September, could push the spread toward 100 basis points for the first time since 2012.

Historical Parallels and Policy Lessons

The current situation bears unsettling similarities to the 2012 Eurozone crisis, when France's yield spread against Germany hit crisis-level highs. Then, as now, political dysfunction and fiscal profligacy fueled market anxiety. However, the policy toolkit has evolved. The European Central Bank (ECB) now has the Transmission Protection Instrument (TPI) to counter market dysfunction, and the Next Generation EU (NGEU) mechanism has introduced a degree of fiscal solidarity through shared debt issuance, a point discussed in a ScienceDirect study. Yet these tools remain untested in a scenario where a core Eurozone economy, rather than a periphery nation, faces scrutiny.

The ECB's hands may also be tied. Unlike 2012, when the institution intervened aggressively to stabilize markets, today's tighter monetary policy environment limits its capacity to act. As one observer noted, "The ECB is unlikely to step in to support French bonds immediately, as this could create moral hazard." This restraint leaves France's borrowing costs increasingly at the mercy of market sentiment, a precarious position for a country already forecasting meager 0.7% growth in 2025.

Implications for the Eurozone and Investors

The implications of this divergence are far-reaching. For France, higher borrowing costs threaten to stifle public investment and strain fiscal consolidation efforts. For the Eurozone, the risk of fragmentation looms large. While countries like Spain and Italy have shown improved fiscal discipline, France's struggles have upended historical risk hierarchies, with its yield spread now exceeding that of Greece-a reversal unthinkable a decade ago, according to that study.

Investors, meanwhile, face a dilemma. On one hand, the situation appears contained, with no immediate signs of a full-blown crisis. On the other, the crowded positioning in French debt markets means any further political or fiscal missteps could trigger sharp volatility. Citigroup has flagged the possibility of the spread reaching 100 basis points, a level that would signal a loss of market confidence akin to 2012.

A Test of Unity

The France-Germany yield spread is more than a technical metric; it is a litmus test for the resilience of the Eurozone's fiscal architecture. While policy tools have advanced since 2012, political will remains fragmented. For France, the path forward requires not only fiscal discipline but also a restoration of governance credibility. For the Eurozone, the challenge is to reconcile divergent national priorities with the collective interest-a task that grows harder with every widening basis point.

As markets watch closely, one truth remains: in a currency union without fiscal union, bond yields will always be the most honest conversation.

Comentarios

Aún no hay comentarios