European Market Volatility and Near-Term Investment Opportunities: Navigating Sector Rotation in a Slowing Stoxx 600

The Stoxx 600, a barometer of European equities, has entered a period of heightened volatility as trade tensions, monetary policy uncertainty, and sector-specific headwinds collide. For investors, the challenge lies in identifying opportunities amid the noise. The index's mixed performance in Q3 2025—driven by divergent sector rotations—offers a blueprint for strategic positioning. According to a report by Charles Schwab, the S&P 500's 11 sectors have been assigned a “Marketperform” rating, reflecting the difficulty of predicting winners and losers in an environment of escalating U.S. tariffs and ECBXEC-- rate cuts[4]. Yet, within this uncertainty, certain sectors are emerging as relative safe havens or high-conviction plays.

Sectoral Divergence: Winners and Losers in Q3 2025

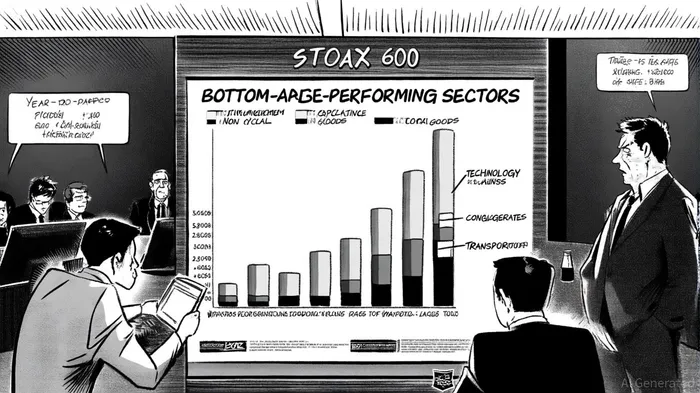

The Stoxx 600's year-to-date performance underscores a sharp bifurcation. Consumer Non Cyclical, Capital Goods, and Technology sectors have surged by 20.58%, 14.95%, and 14.84%, respectively, while Conglomerates and Transportation have plummeted by -5.91% and -3.00%[1]. Within industries, the Computer Peripherals & Office Equipment sector has soared 56.51%, a testament to the resilience of tech-driven demand. Conversely, Oil Well Services & Equipment and Coal Mining have cratered by -32.75% and -29.07%, reflecting the waning relevance of fossil fuels in a decarbonizing economy[1].

This divergence is not random. The ECB's cautious monetary policy, including a 25-basis-point rate cut in June 2025, has provided a floor for equity markets[4], but its impact has been uneven. Sectors reliant on global supply chains—such as automotive and industrial manufacturing—remain vulnerable to U.S. tariffs, which threaten to erode margins and disrupt trade flows[1]. Meanwhile, defensive sectors like consumer staples and technology have benefited from their resilience to macroeconomic shocks.

Macro Drivers: ECB Policy and Trade Tensions

The ECB's 2025 strategy has been defined by a balancing act. With interest rates held at 2% amid “exceptionally uncertain” conditions[1], the central bank has prioritized liquidity support over aggressive rate hikes. This approach has stabilized markets but has not eliminated volatility. As noted in the ECB's Financial Stability Review, trade tensions pose a dual threat: deflationary pressures from a stronger euro and inflationary risks from fragmented supply chains[3].

The U.S. tariff regime, particularly the 25% levy on EU goods, has compounded these challenges. European automakers like BMW and Volkswagen face existential threats, with analysts projecting a 10-15% decline in EU exports to the U.S. and potential job losses in manufacturing[3]. Similarly, the technology sector—already grappling with tariffs on Chinese components—now contends with higher costs for U.S.-bound parts[1]. For investors, the message is clear: sectors exposed to transatlantic trade are underperforming, while those insulated from these frictions are gaining ground.

Sector Rotation Strategies: Where to Allocate Capital

Given this landscape, a disciplined sector rotation strategy is essential. Here are three key recommendations:

Overweight Defensive and Tech-Driven Sectors: Consumer Non Cyclical and Technology sectors have demonstrated resilience. The former benefits from stable demand for essentials, while the latter thrives on innovation cycles and AI-driven growth. As the OECD forecasts a eurozone slowdown to 1.0% in 2026[2], these sectors offer a buffer against macroeconomic headwinds.

Underweight Trade-Exposed Industries: Sectors like Automotive and Industrial Goods remain at risk. The 25% U.S. tariff on cars and parts has created a “tariff cliff” for European manufacturers[1], with ripple effects across supply chains. Investors should avoid overexposure to these industries unless there is a clear path to cost mitigation or market share gains.

Monitor ECB Policy and Geopolitical Catalysts: The ECB's data-dependent approach means further rate cuts are likely if trade tensions persist. A 25-basis-point cut at each meeting through June 2026 could push the deposit rate to 1.5%, providing a tailwind for equities[4]. However, investors must remain agile, as a sudden resolution to trade disputes or a surge in inflation could reverse this trajectory.

Conclusion: Balancing Caution and Opportunity

The Stoxx 600's volatility is a product of both structural and cyclical forces. While trade tensions and ECB policy dominate the headlines, the underlying story is one of sectoral realignment. Investors who prioritize defensive sectors, hedge against trade risks, and stay attuned to monetary policy shifts will be best positioned to navigate this environment. As the OECD warns of a “slowdown driven by tariffs and geopolitical uncertainty”[2], the key to success lies in agility and a nuanced understanding of sector dynamics.

Comentarios

Aún no hay comentarios