European Fiscal Risks: France's Political Uncertainty vs. Italy's Structural Struggles

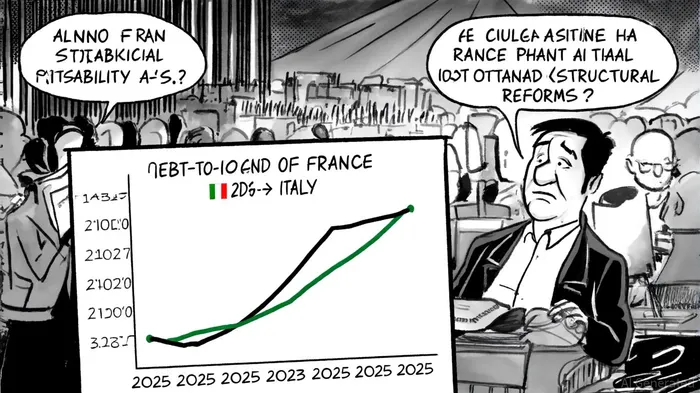

The convergence of France and Italy's 10-year borrowing costs to 3.48% in 2025 marks a pivotal moment in European fiscal dynamics[1]. While this parity might suggest similar risks, the underlying drivers could not be more distinct. France's challenges stem from political instability and unsustainable fiscal policies, whereas Italy's crisis is rooted in structural economic weaknesses. For investors, understanding these nuances is critical to navigating the region's sovereign debt landscape.

France: Political Volatility and Fiscal Uncertainty

France's recent downgrade to “A+” by Fitch Ratings underscores the fragility of its fiscal position[3]. Political turmoil, including the abrupt ousting of the prime minister and the formation of a fragile coalition government, has eroded investor confidence[1]. This instability has hampered reform efforts, leaving public finances exposed. According to a report by Reuters, France's 2025 public debt is projected to reach 118% of GDP, with deficits rising due to tax increases and delayed structural reforms[5]. The IMF has warned that growth is set to slow to 0.6% in 2025, exacerbated by trade tensions and domestic uncertainty[5].

The key risk for France lies in its inability to balance short-term political expediency with long-term fiscal sustainability. Unlike Italy, which has implemented a disciplined consolidation plan, France's repeated policy reversals have created a vacuum of credibility. As one analyst noted, “Investors are pricing in the possibility of further fiscal slippage, not just based on debt levels but on governance quality”[2].

Italy: A Prolonged Crisis, But With Progress

Italy's debt-to-GDP ratio of 145% remains the highest in the eurozone[5], yet its fiscal trajectory has improved markedly. A structural balance improvement of 0.5% annually—exceeding EU requirements—has brought the country close to exiting fiscal disciplinary measures[5]. This progress, though modest, reflects a commitment to stability. Foreign investors have increasingly purchased Italian bonds, signaling renewed confidence despite the nation's demographic headwinds and low growth[1].

Prime Minister Giorgia Meloni's government faces the delicate task of reducing debt without imposing excessive burdens on households. According to Le Monde, Italy is pursuing targeted tax measures and budget cuts to achieve this balance[4]. While structural challenges persist, the political consensus on fiscal discipline has created a more predictable environment for creditors.

Divergent Paths, Shared Risks

The contrasting trajectories of France and Italy highlight a broader truth: sovereign debt sustainability depends as much on governance as on numbers. France's political chaos has amplified risks associated with its moderate debt levels, while Italy's structural weaknesses are mitigated by disciplined fiscal management.

For investors, the takeaway is clear: diversification and nuance matter. France's bonds carry idiosyncratic political risks, whereas Italy's offer exposure to a more stable but economically fragile economy. As the IMF emphasized, both nations require growth-oriented reforms to avoid long-term debt crises[5]. However, Italy's progress suggests that even deeply entrenched fiscal problems can be addressed with consistent policy.

In the coming months, market participants will closely watch France's ability to stabilize its government and implement reforms, while Italy's success in maintaining its consolidation path will determine whether its “ratings boost” becomes a self-fulfilling prophecy[3]. The convergence of their borrowing costs is not a warning of uniform risk but a call to scrutinize the stories behind the numbers.

Comentarios

Aún no hay comentarios