European Dividend Champions in October 2025: A Resilient Income Strategy in a Rising Rate World

In a world where central banks continue to tighten monetary policy, income-focused investors are increasingly drawn to equities that combine high yields with financial resilience. As of October 2025, European dividend champions-companies with decades of uninterrupted or growing dividend payments-stand out as compelling candidates. These stocks, spanning sectors from energy to healthcare, have demonstrated an ability to navigate macroeconomic turbulence while rewarding shareholders. This analysis evaluates their balance sheet strength, historical performance during past rate hikes, and sector-specific advantages to build a case for their inclusion in a rising rate environment.

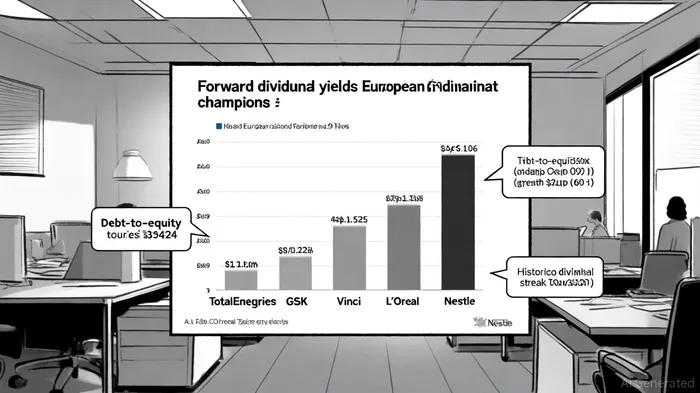

Sectoral Strength: Energy, Healthcare, and Consumer Staples Lead the Way

The energy sector, represented by TotalEnergies (FRA:TOTA), offers one of the highest forward dividend yields, at 6.36%, according to TotalEnergies' dividend history. TotalEnergies' debt-to-equity ratio of 0.53, reflected in its balance-sheet health profile, demonstrates a disciplined approach to leverage, while its liquidity position-current assets nearly matching liabilities-ensures short-term stability, as shown in its financial ratios. This resilience is critical in a sector historically sensitive to interest rate shifts, as higher borrowing costs could strain cash flows. Yet TotalEnergies' ability to maintain a yield above the energy sector average of 6.28% is apparent in Macrotrends' debt-equity chart, underscoring its operational efficiency and pricing power.

In healthcare, GlaxoSmithKline (GSK) presents a mixed profile. While its 4.31% yield is attractive, its debt-to-equity ratio of 1.17, per Macrotrends' GSK data, and weak liquidity metrics (current ratio 0.87, quick ratio 0.57) shown in GSK's financial ratios raise concerns about its capacity to sustain payouts during prolonged rate hikes. However, GSK's post-divestiture earnings profile and focus on high-margin pharmaceuticals could mitigate these risks, as noted in Morningstar's list.

Consumer staples giants like L'Oréal and Nestlé exemplify defensive qualities. L'Oréal's dividend has grown from €0.88 in 2003 to €6.60 in 2023, according to Revenue.land's dividend history, while Nestlé's payout surged from CHF 0.72 to CHF 3.00 over the same period (per the same Revenue.land dataset). These companies operate in sectors with inelastic demand, ensuring stable cash flows even as rates rise. Their balance sheets, though not explicitly detailed in recent reports, are historically robust, with decades of uninterrupted dividend growth serving as a proxy for financial discipline.

Historical Resilience: Lessons from Past Rate Cycles

European dividend champions have repeatedly proven their mettle during monetary tightening. During the 2022–2023 rate hikes, NN Group (a Dutch insurer) raised dividends by double-digit percentages for a decade, achieving an 8% yield, according to a DividendHike profile. Similarly, Rubis, a French energy logistics firm, maintained a 29-year dividend streak despite sector headwinds, a resilience also documented by DividendHike. These examples highlight the importance of business models that generate consistent cash flows-such as insurance underwriting or essential commodity distribution-in sustaining payouts.

The 2008 financial crisis further reinforced sectoral trends. Pharmaceutical leaders like Roche and Novartis avoided dividend cuts, leveraging their pricing power in life-saving drugs, as discussed in Aalto's historical study. In contrast, banks-reliant on net interest margins-saw widespread suspensions. This historical divide underscores the value of investing in sectors with structural advantages, such as pricing power or low capital intensity.

Balance Sheet Metrics: The Unsung Heroes of Resilience

A company's ability to withstand rate hikes hinges on its financial flexibility. VINCI, a construction and engineering firm with a 4.11% yield, exemplifies this. Its debt-to-equity ratio of 2.66, reported in VINCI's 2024 financial statements, appears high, but its liquidity position-current assets (€46.2B) exceeding liabilities (€54.5B)-provides a buffer, as outlined in VINCI's dividend policy. This contrasts with GSK's liquidity constraints, where current assets fall short of obligations as shown in GSK's financial ratios.

TotalEnergies' balance sheet further illustrates the interplay between leverage and liquidity. While its debt-to-equity ratio of 0.53 is modest (see Macrotrends' debt-equity chart), its current ratio of 1.00 and quick ratio of 0.81, visible in its financial ratios, suggest a tight but manageable short-term outlook. For energy firms, access to long-term project financing often offsets immediate liquidity pressures, enabling consistent dividend distributions.

The Case for Income Investors in 2025

As central banks remain hawkish, European dividend champions offer a dual benefit: income preservation and downside protection. The MSCI Europe's projected dividend payouts of €459 billion in 2025, highlighted in an AllianzGI press release-with yields outpacing long-term government bonds-highlight their appeal. For investors, prioritizing companies in sectors with structural demand (consumer staples, healthcare) and conservative balance sheets (TotalEnergies, Nestlé) is key.

However, caution is warranted for high-yield stocks with weak liquidity, such as GSK. Diversification across sectors and rigorous scrutiny of payout ratios can mitigate risks. Ultimately, European dividend champions are not a one-size-fits-all solution but a curated set of equities that reward patience and selectivity.

Comentarios

Aún no hay comentarios