Europe's 2025 IPO Slowdown and the Rise of M&A as a Strategic Exit Route

In 2025, Europe's capital markets are undergoing a seismic shift. The IPO market, once a cornerstone of growth financing, has stalled amid geopolitical turbulence and regulatory headwinds. Meanwhile, M&A activity has surged, with European dealmakers outperforming their peers by a staggering 9.4 percentage points in the first half of the year [2]. This divergence reflects a broader recalibration of risk and reward in EMEA, driven by three interlocking forces: market volatility, regulatory complexity, and the emergence of “quality-of-asset filters” that gatekeep access to public markets.

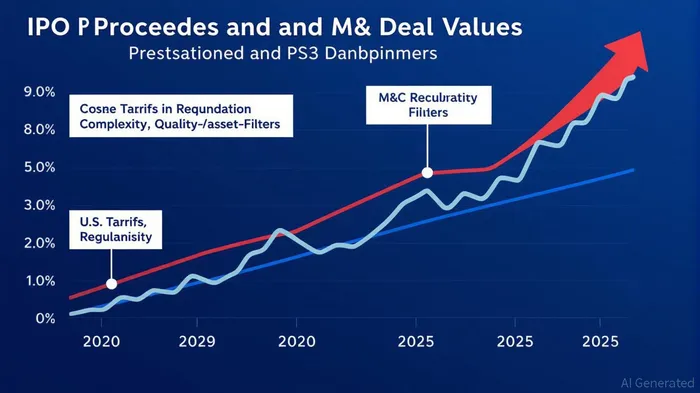

Market Volatility: The IPO's Uninviting Landscape

The European IPO market has become a high-stakes gamble. In Q1 2025, total proceeds from listings fell to $4.59 billion, a 43% drop from the $8.13 billion raised in the same period in 2024 [3]. Smaller companies dominate the listings, but the lack of blockbuster IPOs—such as those seen in the U.S. and Asia—has left investors unimpressed. The root cause? A perfect storm of U.S. trade tariff uncertainty and geopolitical tensions, which have spooked capital flows and eroded confidence in long-term equity valuations [3].

For private equity firms and growth-stage companies, the IPO process itself has become a liability. The average European IPO takes 12–18 months to execute, exposing deals to volatile market conditions that can erase value overnight. As one industry insider notes, “The public markets are now a casino for companies that can't afford to wait for stability” [1]. This has pushed sponsors to pivot toward M&A, where valuations are negotiated privately and exits can be executed in months rather than years.

Regulatory Complexity: A Maze of Compliance

Europe's fragmented regulatory landscape has further tilted the playing field. With 27 national regulators and a patchwork of EU-level rules, cross-border transactions face a labyrinth of compliance hurdles. The European Securities and Markets Authority (ESMA) has intensified scrutiny of digital investment platforms, while the revised Capital Requirements Regulation (CRR3) has made securitisation risk assessments more granular [4].

This complexity disproportionately affects IPO hopefuls. The European Commission's “quality-of-asset filters” demand that companies demonstrate not just profitability but also resilience to macroeconomic shocks—a bar that only 15% of European firms meet [1]. By contrast, M&A allows buyers to structure deals with tailored risk allocations, such as earn-outs and purchase price adjustments, which mitigate regulatory and operational uncertainties [6]. For example, in politically sensitive sectors like energy and AI, buyers are increasingly using earn-outs to align seller incentives with long-term performance, bypassing the rigid scrutiny of public markets [6].

Quality-of-Asset Filters: The New Gatekeepers

The most underappreciated driver of the IPO-M&A shift is the rise of “quality-of-asset filters.” These filters, embedded in both regulatory and investor expectations, demand that companies listed in Europe deliver consistent returns and withstand public market scrutiny. As a result, only a narrow subset of firms—those with durable moats and scalable margins—can secure an IPO.

The skincare company Galderma, backed by EQTEQT--, is a rare success story. Its 2025 IPO demonstrated that high-quality assets can still thrive, but it also underscored the exclusivity of the public markets. For every Galderma, there are dozens of companies that lack the financial or operational rigor to meet these filters [1]. This has created a “gravity well” effect: private equity firms and strategic buyers are now prioritizing M&A as a more certain path to value realization, particularly in sectors like healthcare and infrastructure, where cash flows are predictable and regulatory risks are lower [4].

Long-Term Implications: A Capital Markets Reboot

The 2025 shift from IPOs to M&A signals a deeper transformation in European capital markets. For investors, the implications are twofold:

1. M&A as a Strategic Exit: Private equity and corporate buyers will dominate dealmaking, with a focus on consolidating fragmented industries and leveraging AI-driven operational efficiencies [5].

2. IPOs as a Premium Channel: Public listings will remain a niche option, reserved for companies that can navigate the regulatory and market volatility hurdles. This could accelerate the “Americanization” of European capital markets, where the U.S. remains the go-to destination for high-value listings [1].

However, this trend risks exacerbating inequality in capital access. Smaller companies without strategic buyers may find it harder to scale, while the concentration of power in the hands of a few M&A-savvy firms could stifle innovation. Policymakers must balance regulatory rigor with incentives to diversify exit routes, such as expanding private credit markets or creating hybrid financing instruments that blend the flexibility of M&A with the liquidity of public markets.

Conclusion

Europe's 2025 capital markets story is one of adaptation. As IPOs retreat into a high-threshold niche, M&A has emerged as the dominant vehicle for growth and value capture. For investors, the challenge lies in navigating this new landscape: leveraging the certainty of private deals while keeping a watchful eye on the long-term potential of companies that dare to go public. The winners will be those who recognize that in today's Europe, the path to capital is less about going public and more about going strategic.

Comentarios

Aún no hay comentarios