Euro-Denominated Stablecoins and the Future of European Fintech: Strategic Institutional Adoption and Its Impact on Digital Currency Valuation Models

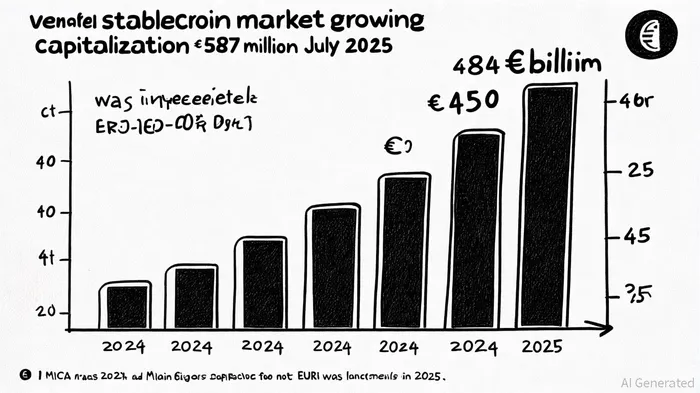

The European fintech landscape is undergoing a seismic shift as euro-denominated stablecoins emerge as a cornerstone of institutional finance. By Q3 2025, these tokens—pegged to the euro and operating under the Markets in Crypto-Assets (MiCA) regulatory framework—have captured 0.2% of the global stablecoin market, with a total capitalization of €484–587 million, up 60% since December 2024 [1]. This growth is not merely speculative; it reflects a strategic alignment between institutional adoption, regulatory clarity, and evolving valuation dynamics.

Institutional Adoption: A Catalyst for Market Legitimacy

Institutional adoption of euro-stablecoins has surged due to three key drivers: regulatory certainty, infrastructure readiness, and competitive pressures. The ECB's MiCA regulation, which came into force in December 2024, has provided a structured environment for stablecoin issuance, mandating 1:1 reserve backing, quarterly audits, and licensing as either e-money institutions (EMIs) or credit institutions [2]. This has spurred the launch of MiCA-compliant tokens like EURI (issued by Banking Circle) and EURC (Circle's euro-backed stablecoin), which now dominate 25% of EU trading volume [3].

Institutions are leveraging these tokens for cross-border payments, B2B settlements, and liquidity optimization. For example, Fireblocks reports $5.7 billion in B2B transactions processed via euro-stablecoins in 2025, driven by telecom and e-commerce sectors [1]. The telecom industry, in particular, has adopted stablecoins to reduce settlement times and operational costs, with 58% of EU firms already using or planning to use them for payment processing [4].

Regulatory Compliance and Valuation Metrics

MiCA's stringent requirements have directly influenced digital currency valuation models. By enforcing reserve transparency and liquidity safeguards, the regulation has reduced liquidity premiums for euro-stablecoins. For instance, EURC's liquidity premium has dropped by 15% since MiCA's implementation, as investors perceive lower insolvency risks compared to non-compliant tokens like USDTUSDT-- [5].

Risk-adjusted returns have also improved. MiCA-compliant stablecoins are now seen as safer assets, with 37% of European institutions citing enhanced security as a key benefit [4]. However, the regulation's requirement to hold 60% of reserves in low-yielding bank deposits has created a yield disadvantage compared to U.S. dollar-stablecoins, which can diversify into higher-yielding assets [6]. This trade-off between safety and yield is a critical consideration for institutional investors.

Case Studies: Compliance as a Competitive Edge

Banking Circle's EURI exemplifies how MiCA compliance can drive institutional adoption. As the first MiCA-compliant stablecoin, EURIEURI-- offers instant settlement and programmable features for cross-border transactions. By Q3 2025, EURI's market cap has surged by 150%, with 85% of European firms reporting infrastructure readiness for stablecoin integration [3].

Quantoz's EURD further illustrates the strategic value of compliance. Backed by the Dutch Central Bank and integrated with 21X's atomic settlement platform, EURD facilitates tokenized securities trading while adhering to MiCA's reserve requirements. This has attracted institutional investors seeking secure, regulated liquidity solutions [7].

Challenges and Future Outlook

Despite progress, challenges persist. The dominance of U.S. dollar-stablecoins (99.85% of the global market) threatens the euro's role in cross-border commerce, prompting the ECBXEC-- to launch initiatives like Project Pontes to integrate blockchain protocols like XRPL and Corda for wholesale use cases [1]. Additionally, liquidity risks remain, with analysts estimating a 3–4% annual run probability for major stablecoin issuers [8].

However, the ECB's dual-track strategy—promoting euro-stablecoins while developing a digital euro—positions Europe to balance innovation with monetary sovereignty. By 2026, the euro-stablecoin market is projected to reach €450 billion, driven by institutional demand for programmable, compliant digital assets [3].

Conclusion

Euro-denominated stablecoins are reshaping European fintech by bridging the gap between traditional finance and digital innovation. Institutional adoption, fueled by MiCA compliance and infrastructure partnerships, has not only enhanced market legitimacy but also redefined valuation metrics like liquidity premiums and risk-adjusted returns. While challenges remain, the strategic integration of stablecoins into cross-border payments and institutional portfolios signals a transformative era for digital currency valuation models.

Comentarios

Aún no hay comentarios