U.S. Equity Market Volatility and Sector Rotation Amid Escalating Tariff Threats

The U.S. equity market has entered a period of heightened volatility as 2025's escalating tariff threats reshape trade dynamics and investor sentiment. With the average effective tariff rate surging to 17.4% by September 2025—up from below 2% in early 2024—the S&P 500 has experienced sharp sectoral rotations, reflecting both the costs of protectionism and the market's adaptive strategies[3]. This analysis examines how tariff-driven uncertainty has altered momentum patterns, disproportionately impacted industries, and forced a recalibration of portfolio allocations.

Sectoral Vulnerabilities and Winners

The Trump administration's sector-specific tariffs—ranging from 100% on branded pharmaceuticals to 25% on heavy trucks—have created a bifurcated landscape. Sectors deeply embedded in global supply chains, such as information technology, automotive, and consumer electronics, face acute headwinds. For instance, automakers like General MotorsGM-- and FordF-- grapple with 25% tariffs on Canadian steel and Mexican cement, inflating production costs and forcing price hikes for consumers[1]. Similarly, semiconductor firms like NvidiaNVDA-- and AMDAMD-- confront bottlenecks from tariffs on imported components, compounding their reliance on foreign foundries[1].

Conversely, defensive sectors and commodity-linked industries have thrived. Health care and utilities, with their low cyclicality, outperformed in Q1 2025, rising 6.1% and 4.1%, respectively, as investors sought stability[3]. Gold miners like Newmont Corp surged amid a record $3,167.57/ounce price, driven by tariffs spooking global growth prospects[4]. Even retail giants like Ross Stores benefited from shifting consumer behavior, as tariffs on Chinese goods pushed demand toward domestic or diversified suppliers[2].

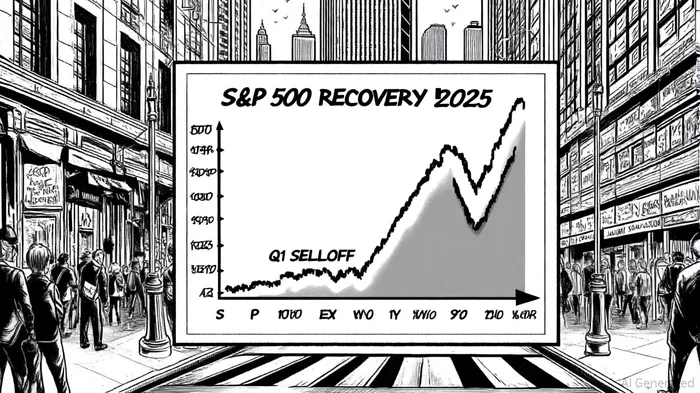

S&P 500 Momentum: A Tale of Two Quarters

The S&P 500's trajectory in 2025 underscores the market's sensitivity to tariff-related news. In Q1, the index plummeted 12.8% as the information technology sector—home to 30% of the index's weight—crashed 20% on losses in Apple (-10.7%) and NVIDIA (-20.3%)[3]. Consumer discretionary (-14%) and financials (-4.46 σ P/E deviation) also faltered, reflecting recession fears and margin pressures[1].

However, a 90-day tariff pause and strong Q2 earnings triggered a 10.94% rebound by May 2025. Technology and communication services led the recovery, surging 23.71% and 18.49%, as trade tensions eased and AI-driven demand offset some tariff costs[1]. Energy, which had gained 4.7% in Q1, reversed course in Q2, declining 8.56% as crude prices slumped amid fears of a global slowdown[3].

Strategic Rotation and Long-Term Implications

Investor behavior has shifted toward hedging against trade policy risks. Defensive allocations to healthcare (P/E 38.09) and utilities (P/E 28.45) have risen, while growth stocks face valuation corrections[1]. Meanwhile, companies leveraging automation and AI—such as Palantir Technologies—have gained traction, as firms seek to mitigate labor and supply chain costs[2].

The economic toll of tariffs, however, remains severe. Global welfare losses are projected to reach 2% under a “full + retaliation” scenario, with U.S. welfare declining by nearly 4%[3]. Retaliatory measures from China, Canada, and the EU have further muddied the outlook, pushing gold and Treasury bonds to record inflows[4].

Conclusion: Navigating a Fragmented Landscape

For investors, the 2025 tariff saga underscores the need for agility. Sectors insulated from global supply chains—such as healthcare, gold, and infrastructure—offer relative safety, while tech and manufacturing remain exposed to policy-driven volatility. As the Federal Reserve adjusts inflation forecasts and companies delay capital investments[2], the S&P 500's path will hinge on whether trade tensions abate or escalate.

Brokerages remain cautiously optimistic, projecting resilient earnings and a stable U.S. economy[2]. Yet, with global markets like Germany and Brazil outpacing U.S. growth[3], the long-term costs of protectionism loom large. For now, the market's resilience—evidenced by its rapid recovery—suggests that volatility, while persistent, may be manageable for those prepared to adapt.

Comentarios

Aún no hay comentarios