Energys Group's 10x Valuation: A Mispricing in a Deteriorating Sector

The Valuation Disconnect

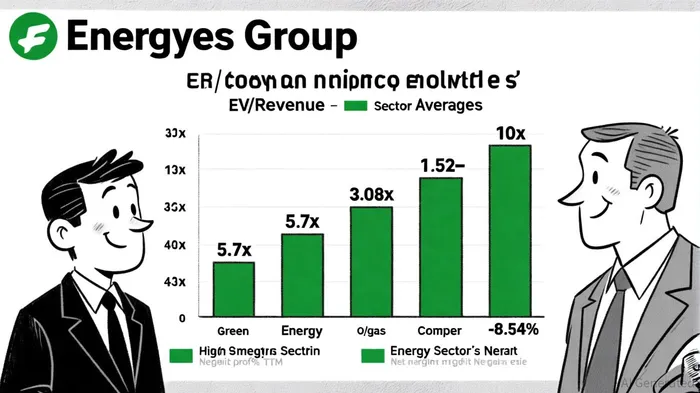

Energys Group's 10x enterprise value-to-revenue (EV/Revenue) multiple starkly diverges from industry benchmarks. According to a report by Finerva, the Green Energy sector's median EV/Revenue multiple in Q4 2024 was 5.7x, a 5-year low driven by high interest rates and policy uncertainty post-2024 [2]. Meanwhile, traditional energy subsectors like "Oil/Gas (Integrated)" traded at a mere 1.52x EV/Sales in 2025 [1]. Energys Group's 10x multiple is not only double the Green Energy sector average but also 6.6x higher than the most leveraged oil/gas peers. This disconnect suggests an overvaluation fueled by speculative growth narratives rather than fundamentals.

Financial Disciplines: A House of Cards

Energys Group's financials reveal a company struggling to translate revenue growth into profitability. Its EBITDA margin of 2.69% in 2025 [2] lags far behind the Energy Sector's 16.85% TTM EBITDA margin [1], while its net profit margin of -8.54% indicates a company hemorrhaging cash [2]. The Debt/EBITDA ratio of 23.21x [2]—a metric that measures leverage—is astronomically high, dwarfing the sector's average debt-to-equity ratio of 0.36 [1]. A negative debt-to-equity ratio of -3.95 [2] further underscores its precarious capital structure, where liabilities exceed equity. Such metrics signal a high-risk profile, yet the market persists in rewarding it with a premium multiple.

Operational Performance: Growth Without Profitability

While Energys GroupENGS-- boasts a 59.67% revenue CAGR through June 2024 [3], its earnings trajectory tells a different story. The company's average annual earnings growth of -14.8% [2] contrasts sharply with the Construction industry's 18.2% growth, highlighting operational inefficiencies. Even its recent free cash flow of -$710,708 [2]—driven by negative capital expenditures—fails to justify optimism. In a sector where Q2 2025 net margins rose 11.27% sequentially [1], Energys Group's losses per share have only stabilized marginally, offering no assurance of sustainable improvement.

Conclusion: A Correction Looms

Energys Group's 10x valuation is a mispricing born of misplaced optimism. With EBITDA margins, profitability, and leverage metrics far below sector averages, the company lacks the financial discipline or operational efficiency to justify such a premium. As macroeconomic headwinds persist and sector multiples normalize, investors are likely to reassess, triggering a valuation correction. For now, the 10x multiple remains a statistical anomaly—unsustainable in a market increasingly focused on fundamentals.

Comentarios

Aún no hay comentarios