Elevance Health: A High-Quality Healthcare Play at a Discounted Valuation

In the evolving healthcare landscape, Elevance HealthELV-- (ELV) emerges as a compelling value investment opportunity. With a market capitalization of $89.92 billion, the company operates at the intersection of health benefits, pharmacy benefit management, and care delivery services. However, its current valuation metrics suggest it is trading at a substantial discount relative to both industry benchmarks and its own historical averages, making it an attractive candidate for long-term investors seeking undervalued quality.

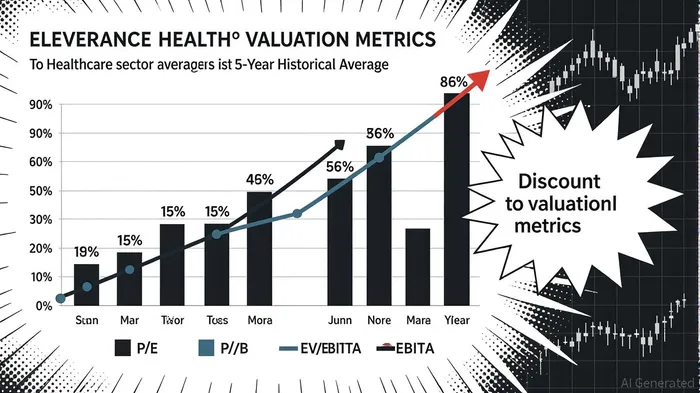

Discounted Valuation: A Case for Value Investing

Elevance Health’s price-to-earnings (P/E) ratio of 13.27 as of September 2025 is 47% lower than the healthcare sector average of 25 [1]. This discrepancy is even more pronounced when comparing its price-to-book (P/B) ratio of 1.61 to its 5-year averages of 2.72 and 2.74 for 3- and 5-year periods, respectively [4]. The company’s enterprise value-to-EBITDA (EV/EBITDA) ratio of 8.04 further underscores its undervaluation, falling into the “Strongly Undervalued” category compared to its 5-year average of 10.34 [4]. These metrics indicate that ElevanceELV-- Health is trading at a discount not only to its historical performance but also to broader industry standards, such as the Nifty Healthcare Index’s P/B ratio of 5.4 [5].

Long-Term Growth Drivers: Strategic Positioning in a Transforming Industry

Elevance Health’s 2025 business strategy is anchored in three pillars: value-based care, AI integration, and strategic acquisitions. The company is expanding its focus on value-based care, which emphasizes coordinated treatment and cost efficiency, particularly in high-growth areas like behavioral health and oncology [1]. Through its Carelon business, Elevance integrates pharmacy, behavioral health, and complex care management, addressing member needs holistically. The 2024 acquisition of CareBridge has further enhanced its capabilities by providing virtual care to Medicaid and Medicare patients, supporting home and community-based services [1].

These initiatives have already driven measurable growth. Medicare Advantage membership increased 11% year-over-year, while total revenues rose 13.4% in the same period [1]. Q2 2025 operating revenue reached $49.4 billion, a 14% year-over-year increase driven by premium yields, acquisitions, and membership growth [4]. Additionally, the acquisition of Granular Insurance Company in 2025 strengthens Elevance’s employer solutions, enabling self-funded employers to access innovative risk management tools [2].

Financial Health and Competitive Positioning

Elevance Health’s financials reflect a balance between disciplined cost management and strategic reinvestment. Its debt-to-equity ratio of 0.69 as of June 2025 is slightly higher than the Healthcare Plans sector median of 0.66 but remains moderate compared to peers [1]. Free cash flow in FY2024 totaled $4.55 billion, a decline from $6.76 billion in 2023, primarily due to elevated working-capital needs and acquisition activities [4]. However, the company’s operating expense ratio improved to 9.9% in Q4 2024 on an adjusted basis, reflecting disciplined cost management [3].

Despite challenges such as rising medical costs in Medicaid and ACA plans, Elevance Health’s operating margins remain resilient. For FY2024, the company reported an 11.4% operating margin for its consolidated enterprise [1]. While Q2 2025 saw a slight dip to 5% due to higher benefit expense ratios, the Carelon segment maintained an adjusted operating margin of 5.2%, demonstrating operational efficiency [2].

Conclusion: A Compelling Value Proposition

Elevance Health’s discounted valuation, robust growth drivers, and strong financial position position it as a high-quality healthcare play. Its strategic focus on value-based care and AI-driven solutions aligns with long-term industry trends, while its disciplined capital allocation—evidenced by $1.8 billion in share repurchases in Q4 2024—reinforces shareholder value [1]. For value investors, the current discount to intrinsic value, as estimated through discounted cash flow and relative valuation models [5], presents an opportunity to capitalize on a company poised for sustained growth in a critical sector.

Source:

[1] ELVELV-- - Elevance Health PE ratio, current and historical [https://fullratio.com/stocks/nyse-elv/pe-ratio]

[2] Elevance Health (ELV): Growth, Market Impact, and Outlook [https://monexa.ai/blog/elevance-health-elv-strategic-growth-market-impact-ELV-2025-03-18]

[3] Elevance Health Reports Fourth Quarter and Full Year 2024 Results [https://www.elevancehealth.com/newsroom/elv-quarterly-earnings-q4-2024]

[4] ELV PE Ratio — ELV Valuation, Is ELV Overvalued [https://intellectia.ai/stock/ELV/valuation]

[5] Nifty Healthcare Index Price to Book Ratio (PB) [https://trendlyne.com/equity/PB/NFTHEALTHC/910417/nifty-healthcare-index-price-to-book-ratio/]

Comentarios

Aún no hay comentarios