U.S. Economic Momentum and Cyclical Sector Viability: Navigating Fed Policy and Industrial Trends in 2025

The U.S. economy in late 2025 is navigating a delicate balancing act between tightening labor markets, persistent inflation, and sector-specific industrial trends. For cyclical sector investors, the interplay between Federal Reserve policy and industrial production data offers critical insights into near-term opportunities and risks.

Industrial Sector Performance: Mixed Signals Amid Structural Shifts

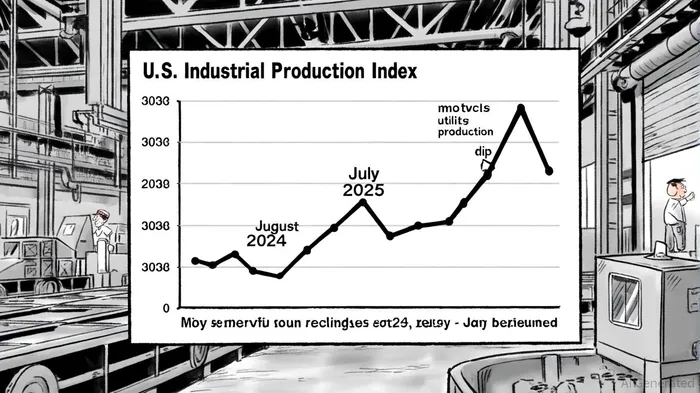

The Federal Reserve's latest Industrial Production data reveals a nuanced picture. In August 2025, the U.S. Industrial Production Index rose by 0.1%, driven by a 2.6% surge in motor vehicle and parts manufacturing and a 0.9% increase in mining output, according to the Federal Reserve's industrial production release. However, utilities production fell by 2.0%, reflecting seasonal declines in electric utilities, as that release shows. Capacity utilization for manufacturing remained at 77.4%, still 2.2 percentage points below its long-run average, suggesting underutilized capacity but also lingering constraints from labor and supply chain bottlenecks noted in the same release.

Sector-specific trends further complicate the outlook. The September 2025 Manufacturing Business Outlook Survey highlights divergent performance: durable goods manufacturing (e.g., electrical equipment, aerospace) grew by 0.3%, while nondurable goods contracted by 0.4%, according to the Philadelphia Fed's Manufacturing Business Outlook Survey. Meanwhile, the Philadelphia Fed's survey notes a shift toward automation and local supply chains, with firms leveraging AI to offset labor shortages, a trend also discussed in the Boston Fed's Beige Book. However, tariffs on electronic components and raw materials continue to strain input costs, particularly for chemicals and plastics producers, the Fourth District Beige Book reports.

Fed Policy: A Pivotal Shift in Monetary Stance

The Federal Reserve's September 2025 FOMC meeting marked a pivotal shift. After months of maintaining a hawkish stance, the central bank cut the federal funds rate by 0.25 percentage points, bringing the target range to 4.00%-4.25%, according to the Fed's FOMC statement. This was the first rate cut since December 2024 and reflects growing concerns over a cooling labor market-job gains have slowed, and the unemployment rate has edged upward, though it remains near historical lows, the statement noted. The FOMC also signaled two additional rate cuts in 2025 and one in 2026, though internal divisions were evident: newly appointed Governor Stephen Miran dissented, advocating for a larger 0.50-point cut, as the FOMC statement indicated.

The policy pivot is a direct response to inflationary pressures. While core PCE inflation has moderated to 2.8%, it remains above the Fed's 2% target, with input price pressures persisting in manufacturing, as a MarketMinute article notes. The central bank's dual mandate-balancing employment and price stability-now leans toward supporting growth, as downside risks to the labor market have risen per the FOMC statement.

Cyclical Sector Investment Viability: Weighing Stimulus and Structural Headwinds

For cyclical sectors, the Fed's easing cycle and industrial trends present a mixed outlook. On the positive side, lower interest rates should boost demand for capital-intensive industries like construction, machinery, and transportation equipment. The August 2025 rebound in motor vehicle production (up 2.6%) and the Philadelphia Fed's survey of rising new orders and shipments suggest resilience in consumer-driven sectors. Additionally, automation adoption could enhance productivity, mitigating some labor constraints, a point also emphasized in the Beige Book.

However, structural headwinds persist. Tariffs on critical inputs-such as electronic components and metals-are squeezing margins, particularly in chemicals and plastics, as the Fourth District Beige Book highlights. Capacity utilization rates remain suboptimal, with 86% of firms in the September 2025 survey citing uncertainty as a constraint, according to the Manufacturing Business Outlook Survey. Furthermore, the utilities sector's decline underscores the vulnerability of energy-dependent industries to regulatory and environmental shifts, as the industrial production release shows.

Strategic Implications for Investors

Cyclical sector investments in 2025 require a granular approach. Sectors poised to benefit from the Fed's easing cycle-such as machinery, construction, and AI-driven manufacturing-offer compelling opportunities, particularly for firms with strong balance sheets to navigate near-term volatility. Conversely, industries facing tariff-driven cost pressures (e.g., chemicals, plastics) and overhanging capacity constraints may require caution.

The key to success lies in aligning with structural trends. Automation and digital transformation, as highlighted in the Beige Book, are reshaping industrial productivity. Investors should prioritize firms leveraging AI and local supply chains to offset labor and input costs. Additionally, the Fed's projected rate cuts may provide a tailwind for cyclical equities, but their effectiveness will depend on whether the broader economy avoids a recessionary downturn.

Conclusion

The U.S. economy stands at a crossroads in late 2025. While the Fed's policy pivot and industrial sector rebounds offer hope for cyclical growth, structural challenges-including tariffs, labor shortages, and capacity underutilization-remain significant hurdles. For investors, the path forward demands a balanced strategy: capitalizing on rate-sensitive sectors while hedging against sector-specific risks. As the October 2025 data releases approach, continued vigilance on both industrial production trends and central bank signals will be essential.

Comentarios

Aún no hay comentarios