ECB's Rate Halt: A Strategic Buying Opportunity in the Eurozone

The European Central Bank's (ECB) decision to maintain its key interest rates unchanged in November 2025, despite a softening inflation outlook, has created a compelling case for a tactical shift toward eurozone assets. With the ECB signaling a data-dependent, meeting-by-meeting approach to policy and upgrading its growth and inflation projections, investors are presented with a unique window to capitalize on undervalued European equities and bonds amid divergent global monetary policies.

A Hawkish Pause Amid Uncertainty

The ECB's latest policy statement left its Deposit Facility, Main Refinancing Operations, and Marginal Lending Facility rates unchanged at 2.00%, 2.15%, and 2.40%. While the Governing Council emphasized its commitment to achieving a 2% inflation target, it explicitly rejected pre-committing to a specific rate path, citing heightened uncertainties from global trade tensions and geopolitical risks which the ECB now projects inflation to average 2.1% in 2025. This "hawkish pause" reflects a recalibration of expectations: the ECB now projects inflation to average 2.1% in 2025, 1.9% in 2026, and 1.8% in 2027, with a return to 2.0% by 2028 according to revised projections. Such a trajectory, combined with a revised Eurozone growth outlook of 1.4% in 2025, underscores the ECB's confidence in the region's resilience despite external headwinds.

This cautious yet optimistic stance contrasts sharply with the U.S. Federal Reserve's more aggressive rate-cutting trajectory. As of late 2025, U.S. 30-year Treasury yields peaked at 4.99%, while the ECB's 2% deposit rate-effectively a near-zero real rate-has anchored eurozone bond yields according to market analysis. This divergence, driven by divergent economic fundamentals (weaker U.S. labor markets versus Eurozone domestic demand resilience), has created a yield differential that favors eurozone assets.

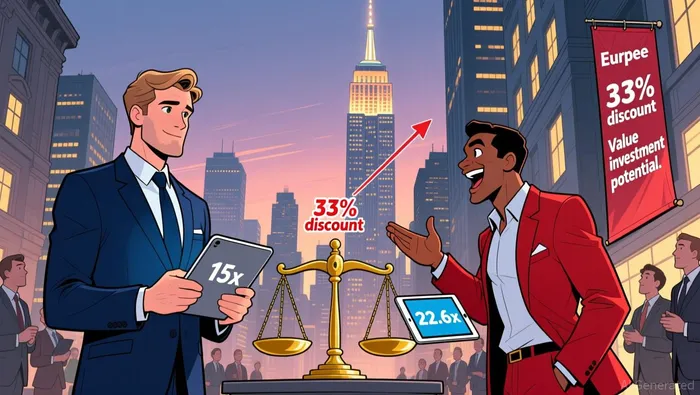

Undervalued Equities: A 33% Discount to U.S. Peers

European equities trade at a significant valuation discount to their U.S. counterparts, with a forward price-to-earnings (P/E) ratio of 15.1x compared to the S&P 500's 22.6x according to AllianzGI analysis. This 33% gap is particularly striking given European markets' outperformance in 2025, driven by fiscal stimulus, improved Chinese economic data, and geopolitical stability in Germany. For instance, the STOXX Europe 600's 15x forward P/E versus the S&P 500's 22x highlights a 30% valuation disparity, exacerbated by U.S. tariffs dampening export-exposed sectors like healthcare and technology.

Specific sectors offer even more compelling opportunities. The European healthcare sector, for example, trades at a multi-decade low of 12x P/E, with pharmaceutical giants like Sanofi and Thermo Fisher offering discounted valuations despite robust long-term fundamentals according to TrustNet reporting. Similarly, the industrials sector, supported by reshoring trends and a forward P/E of 19.5x, has shown resilience amid global supply chain shifts according to TrustNet analysis. These sectors, coupled with a projected 12% earnings growth in 2026, suggest European equities are poised for a re-rating.

Bond Yields and Fiscal Reforms: A Path to Stability

Eurozone government bond yields have also become increasingly attractive. While U.S. Treasuries face pressure from persistent fiscal deficits and external financing needs, European countries are addressing deficits through infrastructure and defense spending, which could drive bond yields lower in 2026. The narrowing spreads between core and peripheral bonds-such as the reduced gap between German Bunds and Italian BTPs-further signal improved fiscal coordination and risk-sharing.

The ECB's forward guidance, which remains open-ended, adds to the appeal. By avoiding pre-commitment to rate cuts, the ECB has created a policy environment where yields are broadly anchored, offering investors a stable backdrop for long-term holdings according to Morningstar analysis. This contrasts with the U.S., where political pressures and fiscal sustainability concerns have weakened the dollar's safe-haven status, prompting a reassessment of capital flows.

Strategic Implications for Investors

The ECB's rate hold and hawkish revisions, combined with the ECB's focus on structural reforms to boost competitiveness, present a strategic buying opportunity. European equities, trading at a material discount to U.S. peers, offer exposure to sectors poised for earnings growth, while eurozone bonds benefit from a more stable fiscal outlook and narrower risk spreads.

However, investors must remain mindful of currency risks and geopolitical uncertainties. The euro's weakness, while boosting the valuation of European assets in foreign currency terms, could also amplify volatility. Yet, given the ECB's commitment to a data-dependent approach and the Eurozone's stronger growth trajectory, the case for a tactical shift into eurozone assets is compelling.

As the ECB navigates a complex global landscape, its policy flexibility and the undervaluation of European assets suggest that now is the time to rebalance portfolios toward the eurozone. The market's current discount reflects not a lack of potential, but a mispricing of risk-a mispricing that history suggests will correct as fundamentals align with valuations.

Comentarios

Aún no hay comentarios