ECB's Pivot: Navigating EUR Assets in a Low-Inflation Era

The European Central Bank's (ECB) recent shift toward a “mildly supportive” monetary policy stance has sent ripples through EUR-denominated markets, reshaping the outlook for bonds, currencies, and equities. With inflation risks now skewed firmly to the downside, investors must recalibrate strategies to capitalize on yield opportunities while navigating the implications of a potential rate-cut cycle.

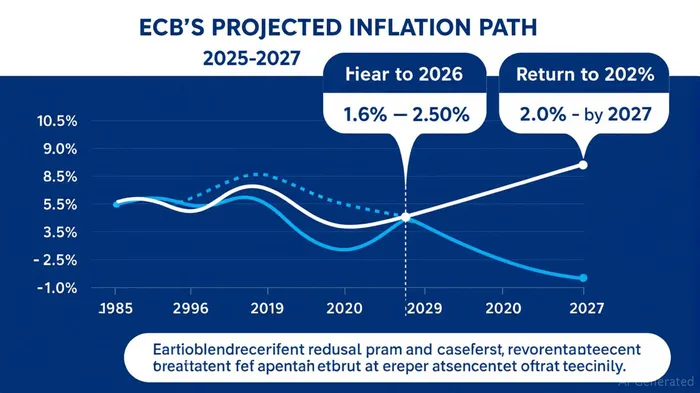

The Inflation Dilemma: Downward Risks and Policy Response

The ECB's June 2025 decision to cut rates by 25 basis points—marking the first easing move since 2023—reflects Governor Pierre Wunsch's emphasis on the asymmetry of inflation risks. Key drivers of this pivot include:

- Falling energy prices: Crude oil prices have declined by ~20% year-to-date, easing input cost pressures.

- Euro strength: The EUR/USD exchange rate has surged to 1.18, its highest since late 2021, dampening import prices and inflation expectations.

- Soft wage growth: Negotiated wage increases have slowed to 2.4% in Q1 2025, down from 4.1% in late 2024, reducing domestic demand-driven inflation.

Fixed-Income Opportunities: Peripheral Bonds and Yield Differentials

The ECB's dovish turn has created a favorable environment for EUR fixed-income investors. Key strategies include:

1. Peripheral debt: The narrowing of yield spreads between Italian and German bonds offers asymmetric upside. For instance, Italian BTPs currently yield 3.8%, versus 2.3% for German Bunds—a 150 basis point premium.

The ECB's Transmission Protection Instrument (TPI) and the region's resilient labor markets (6.2% unemployment) support peripheral debt, even as growth risks linger.

- Duration extension: With inflation expected to average 1.6% in 2026, core EUR bonds are primed for capital gains. The German 10-year Bund's yield has fallen to 2.3% since March, and further easing could push it toward 2.0% by year-end.

Currency: The Weakening EUR as a Strategic Hedge

The euro's appreciation has been a double-edged sword: while it dampens inflation, it risks hurting eurozone exports. Investors can exploit this dynamic through:

- EUR/USD short positions: The pair's rise to 1.18 has outpaced fundamentals, and a potential ECB rate cut could reverse this trend.

- Emerging market currency pairs: The EUR's safe-haven status may wane if global volatility rises, favoring currencies like the USD or GBP.

Equities: Caution on Export-Driven Sectors

While European equities have rallied on fiscal stimulus hopes (e.g., Germany's 3.1% deficit expansion), investors should tread carefully in export-heavy sectors. A stronger euro and tepid global trade volumes could compress margins for companies reliant on foreign sales.

- Overvalued risks: Export-driven stocks, such as automotive and industrial firms, trade at 15-20% premiums to historical averages.

- Alternatives: Defensive sectors like utilities and healthcare, insulated from currency swings, offer steadier returns.

Risk Considerations: Trade Tensions and Supply Shocks

The ECB's outlook hinges on trade policies. Escalating tariffs could trigger a “severe scenario” of lower growth and inflation, while a resolution might boost equities but not significantly pressure rates upward. Investors should monitor:

- U.S. tariff expiration: The July 2025 deadline for suspended steel tariffs poses a wildcard for EUR manufacturing stocks.

- Supply chain disruptions: Risks like rare earth export restrictions could create upside inflation surprises, complicating the ECB's path.

Conclusion: Positioning for a Lower-for-Longer ECB

The ECB's shift underscores a prolonged period of low rates and yield-seeking opportunities. Core and peripheral bonds, paired with EUR currency hedges, form the nucleus of a resilient portfolio. Meanwhile, equity investors should favor domestic-demand sectors and avoid overpaying for export-driven names. As Wunsch noted, the ECB's mandate to anchor inflation expectations at 2% means further easing could be on the table—even as markets price in only one more cut this year.

Investment Advice:

- Aggressive plays: Buy Italian BTPs or short EUR/USD futures.

- Moderate plays: Overweight German Bunds and defensive equities.

- Avoid: Overvalued export stocks until trade risks abate.

The ECB's pivot isn't just about rates—it's a signal to embrace EUR fixed income and remain vigilant on currency and equity exposures.

Comentarios

Aún no hay comentarios