Dynex Capital's Q3 2025 Performance: Strategic Positioning in a Shifting CRE Finance Landscape

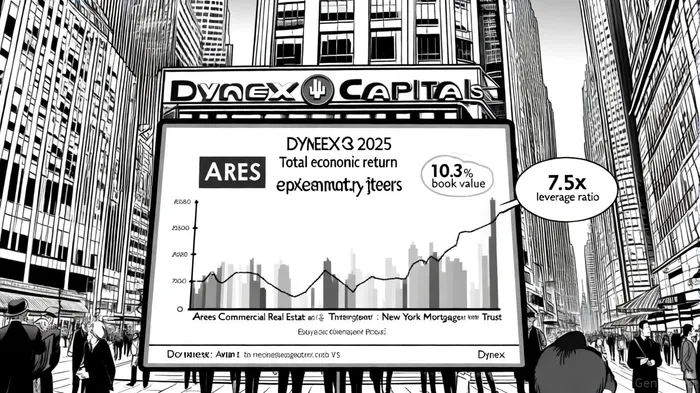

Dynex Capital's Q3 2025 results underscore its aggressive capital deployment strategy and disciplined execution in a volatile commercial real estate (CRE) finance environment. The company reported a total economic return of $1.23 per common share, translating to a 10.3% return on beginning book value-a figure driven by a $0.72 increase in book value per share and $0.51 in dividends declared, as noted in its press release. This performance outpaces industry benchmarks, particularly as peers like Ares Commercial Real Estate (ACRE) reported GAAP net losses in the same period, according to an Investing.com transcript.

Strategic Capital Deployment and Leverage

Dynex's operational momentum is anchored in its ability to scale its portfolio while maintaining liquidity. During Q3, the company raised $254 million in equity capital via at-the-market (ATM) programs, bringing year-to-date capital raises to $776 million, according to its earnings report. These funds were deployed into $2.4 billion in Agency RMBS and $464 million in Agency CMBS, expanding total assets to $14.16 billion as of September 30, 2025, per the MBA CREF25 takeaways. This aggressive growth was financed through a 36.7% increase in repurchase agreement borrowings, pushing leverage to 7.5x shareholders' equity. While elevated leverage introduces refinancing risks-67% of repurchase agreements mature in less than 30 days-the company's liquidity buffer of over $1 billion provides a critical safety net.

Industry Tailwinds and Sector Diversification

The CRE finance sector in 2025 is characterized by divergent performance across property types. Industrial and multifamily assets remain resilient, with CMBS originations projected to grow 33% year-over-year due to strong demand and tighter credit spreads, according to MarketBeat. Dynex's focus on Agency RMBS and CMBS aligns with this trend, as these instruments offer liquidity and transparency in a market where traditional lenders face Basel III Endgame constraints, noted in the CRE capital markets outlook. Conversely, the office sector continues to struggle, with vacancy rates exceeding 20% and delinquency risks rising, as discussed on the AcuityKP blog. Dynex's portfolio, however, is insulated from these headwinds, as its Agency securities are backed by government guarantees, reducing exposure to sector-specific downturns.

Competitive Edge and Financial Metrics

Dynex's financial metrics highlight its superior positioning relative to peers. Its net margin of 7.44% dwarfs Ares Commercial Real Estate's -4.66%, while its 10.38% return on equity (ROE) reflects efficient capital utilization, according to a TradingView report. Additionally, Dynex's 12.80% dividend yield-well above the industry average of 6.85%-attracts income-focused investors, supported by five consecutive years of dividend growth. This contrasts with Redwood Trust (RWT), which reported a $98.5 million net loss in Q3 2025 due to investment fair value declines, as discussed in a CMBS outlook.

Strategic Hedging and Forward-Looking Outlook

Management's proactive adjustments to hedging strategies further reinforce resilience. Dynex increased interest rate swap notional amounts by nearly 10% while reducing short U.S. Treasury futures exposure, mitigating risks from potential rate volatility. Looking ahead, the Federal Reserve's September 2025 rate cut is expected to boost net interest margins in Q4, as tighter spreads and lower borrowing costs take effect. However, deferred tax hedge gains of $688 million-projected to be recognized through 2028-pose a long-term overhang on distributable earnings.

Risk Considerations and Market Position

Despite its strengths, Dynex's high leverage and short-term refinancing obligations demand close monitoring. The company's 7.5x leverage ratio, while optimal for capital efficiency, amplifies sensitivity to liquidity shocks. Additionally, the CRE sector's "wall of maturities"-over $1 trillion in commercial mortgages maturing in 2025-could strain capital markets if refinancing conditions deteriorate, as outlined in the commercial real estate loans guide. Dynex's liquidity position and access to alternative capital sources (e.g., private credit funds) will be critical in navigating this challenge.

Conclusion: A Leader in a Fragmented Market

Dynex Capital's Q3 2025 results affirm its leadership in the CRE finance sector, combining aggressive growth with disciplined risk management. By capitalizing on favorable interest rate dynamics and sector-specific tailwinds, the company has outperformed peers while maintaining a robust liquidity profile. However, investors must weigh its elevated leverage and refinancing risks against its strong dividend yields and strategic agility. As the industry navigates a bifurcated recovery, Dynex's focus on Agency securities and proactive hedging positions it to capitalize on near-term opportunities while mitigating long-term vulnerabilities.

Comentarios

Aún no hay comentarios