Dynex Capital's October 2025 Dividend and Its Implications for REIT Investors

Dynex Capital, Inc. (DX) has once again reaffirmed its commitment to income-focused investors by declaring a monthly dividend of $0.17 per share for October 2025, payable on November 3 to shareholders of record as of October 23, according to a Yahoo Finance report. This consistent payout, translating to an annualized yield of approximately 15.5%, was reported in a MarketMinute article, and underscores the company's role as a high-yield option in a market where traditional REITs struggle to maintain returns. However, the sustainability of this dividend-and its implications for investors-hinges on a delicate balance between capital resilience, debt management, and the risks posed by a high-interest-rate environment.

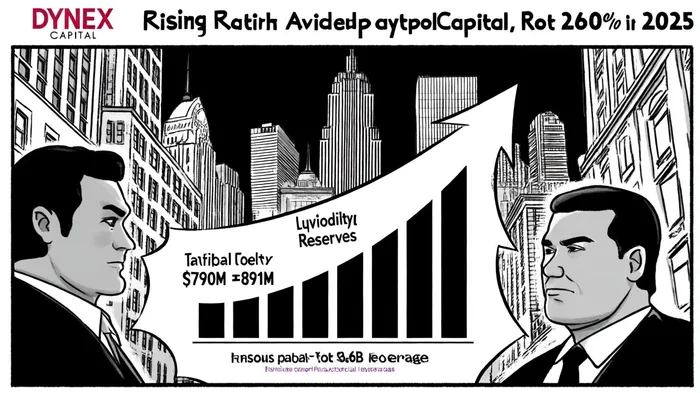

Financial Resilience and Capital Raising: A Double-Edged Sword

Dynex Capital has demonstrated aggressive capital-raising efforts in 2025, securing $240 million in Q1 and $560 million in Q2 through common stock issuances, according to a Dynex press release. These actions bolstered liquidity reserves to $790 million by March 31 and $891 million by June 30, providing a buffer against short-term volatility. The company also expanded its portfolio to $14 billion in Agency RMBS and TBA securities, leveraging its internally managed structure to capitalize on market opportunities.

Yet, these gains come with caveats. As of June 30, 2025, Dynex reported total assets of $11.31 billion, driven by a surge in mortgage-backed securities, while liabilities-including $8.6 billion in repurchase agreements-highlighted a reliance on short-term financing, as shown on the company balance sheet. This leverage, combined with a projected 2025 interest expense of $314 million, raises questions about the company's ability to navigate rising borrowing costs. Analysts note that while the capital-raising strategy provides flexibility, it also amplifies exposure to refinancing risks, particularly as $3.9 billion in repurchase agreements mature within 30 days, according to a StocksToday analysis.

Dividend Sustainability: A Payout Ratio in Peril

The $0.17 monthly dividend, while attractive, is supported by a payout ratio exceeding 260%-a figure that signals a disconnect between earnings and distributions, which StocksToday highlighted. This metric, coupled with a Q2 2025 comprehensive loss of $0.10 per share noted by the same coverage, has led some observers to question the long-term viability of the dividend. Dynex has historically relied on deferred tax hedge gains to supplement distributions, with $100 million projected for 2025, but such gains are not a sustainable earnings substitute.

Despite these concerns, the company's hedging strategies and internally managed structure are viewed as mitigants. By locking in long-term hedges and adjusting its portfolio duration, Dynex aims to reduce sensitivity to interest rate fluctuations, a point also emphasized in the MarketMinute article. Analysts remain cautiously optimistic, with some raising price targets based on the belief that the company's liquidity and capital-raising prowess will offset short-term headwinds.

Implications for REIT Investors in a High-Rate World

For income-focused investors, Dynex Capital's dividend presents a paradox: a high yield paired with structural risks. The 15.5% annualized yield is among the most attractive in the REIT sector, per the MarketMinute article, but it comes at the cost of elevated volatility. In a high-interest-rate environment, where refinancing costs and mortgage prepayment risks are magnified, Dynex's heavy leverage and high payout ratio could lead to dividend cuts or capital preservation measures.

Investors must weigh these risks against the company's proactive capital-raising and portfolio growth. While the "Moderate Buy" rating from some analysts was reported by StocksToday and suggests confidence in management's ability to navigate challenges, the path forward is far from certain. For those with a high-risk tolerance and a focus on income, Dynex could offer compelling returns-but only if the company's financial engineering can outpace macroeconomic headwinds.

Conclusion

Dynex Capital's October 2025 dividend announcement reaffirms its position as a high-yield REIT, but the sustainability of this payout remains contingent on its ability to manage debt, hedge against rate risks, and maintain liquidity. While the company's capital-raising efforts and strategic portfolio adjustments provide a degree of resilience, the high payout ratio and refinancing challenges pose significant threats. For REIT investors, the key takeaway is clear: the allure of a 15.5% yield must be balanced against the realities of a leveraged, high-interest-rate environment.

Comentarios

Aún no hay comentarios