DXP Enterprises (DXPE): Navigating Short-Term Volatility Amid Long-Term Growth Potential

DXP Enterprises (DXPE): Navigating Short-Term Volatility Amid Long-Term Growth Potential

In the past week, DXP EnterprisesDXPE-- (DXPE) has seen its stock price tumble nearly 6%, mirroring broader market anxieties about inflation and the sustainability of the AI-driven rally, according to a Yahoo Finance report. While the short-term pain is real, investors would be wise to separate the noise from the fundamentals. DXP's long-term trajectory-marked by robust revenue growth, margin expansion, and a clear-eyed strategy for industrial innovation-suggests that this volatility may be a buying opportunity rather than a warning sign.

Short-Term Volatility: A Symptom of Macro Fears

The recent selloff in DXPEDXPE-- shares is part of a larger narrative. A Yahoo Finance report noted the stock fell 5.8% on October 7, 2025, as rising inflation expectations and concerns about an overextended AI sector spooked investors. The fear is not unfounded: AI-driven stocks have surged ahead of tangible earnings, creating a fragile ecosystem where any hint of a slowdown could trigger a cascade. For DXPDXPE--, an industrial distributor with exposure to manufacturing and energy, the worry is that a broader economic slowdown could dampen demand for its services.

This anxiety was compounded by a weaker-than-expected U.S. consumer confidence report in early October, which saw the Conference Board's index drop to 94.2-the lowest since April 2025, the Yahoo Finance report added. While DXP's business is more B2B than B2C, a slowdown in corporate spending or capital expenditures could ripple through its supply chain.

Long-Term Fundamentals: A Story of Resilience and Growth

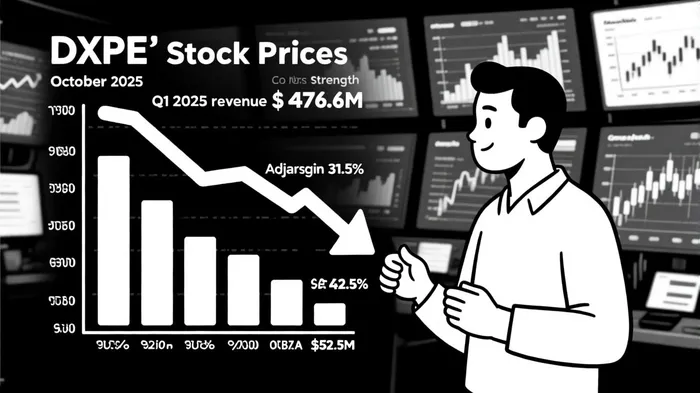

Yet, for all the near-term jitters, DXP's underlying business remains strong. The company's Q1 2025 results, reported in June, tell a tale of disciplined execution. Revenue hit $476.6 million, a 15.5% year-over-year increase, with organic sales growth of 11.1%, as shown in Investing.com slides. Gross margins expanded to 31.5% from 29.5% in Q1 2023, and adjusted EBITDA surged to $52.5 million, a 30% year-over-year jump. These metrics suggest a company that is not only surviving but thriving in a competitive industrial landscape.

Historical backtesting of DXPE's earnings events since 2022 reveals mixed results. While the 30-day post-earnings cumulative return averaged ~5.3%, the S&P 500 benchmark averaged ~6.4% over the same period. With only five earnings events in the sample, the data lacks statistical significance, and no daily horizon showed a reliably exploitable edge. This suggests that while DXP's fundamentals are strong, its stock price may not consistently outperform the broader market following earnings releases.

DXP's capital allocation strategy further underscores its long-term vision. The company has allocated 58% of its capital to net debt repayment, 37% to capital expenditures, and 5% to M&A-a balanced approach that prioritizes both stability and growth. Its recent acquisition of Arroyo Process Equipment, for instance, has bolstered its Innovative Pumping Solutions segment, which now boasts a 15.5% operating margin-the highest of its three business lines.

Strategic Positioning: Digital Transformation and Market Expansion

What sets DXP apart is its proactive approach to digital transformation. The company is investing heavily in automation, IoT-driven predictive maintenance, and e-commerce platforms to streamline operations and enhance customer experience. These initiatives are not just cost-saving measures; they position DXP as a leader in the industrial sector's shift toward data-driven efficiency.

Geographically, DXP is expanding its footprint through a mix of organic growth and strategic acquisitions. Its goal to reach $2 billion in revenue by 2026 is ambitious but achievable, given its current trajectory, according to a SWOT profile. The company's focus on becoming a "national industrial solutions platform" aligns with broader industry trends, where companies are increasingly seeking integrated, end-to-end services.

The Verdict: Volatility as a Filter

For investors, the key is to distinguish between transient market fears and enduring business value. While DXP's short-term volatility reflects macroeconomic uncertainties, its long-term fundamentals-strong revenue growth, margin expansion, and a clear strategic vision-suggest that the company is well-positioned to weather the storm.

Analysts remain cautiously optimistic, with one Wall Street analyst maintaining a "Buy" rating and a 12-month price target of $95, despite the current stock price of $119.49, per Investing.com. This implies a potential 19% downside, but it also reflects confidence in DXP's ability to deliver value over time.

In the end, DXP's story is a reminder that volatility is not the enemy-it's a filter. For those with a long-term horizon, the recent dip may offer an opportunity to invest in a company that is not only adapting to change but leading it.

Comentarios

Aún no hay comentarios