Driven Brands' $500M Debt Refinancing and Capital Structure Optimization: Strategic Balance Sheet Management in the Automotive Services Sector

Strategic Debt Refinancing and Liquidity Enhancements

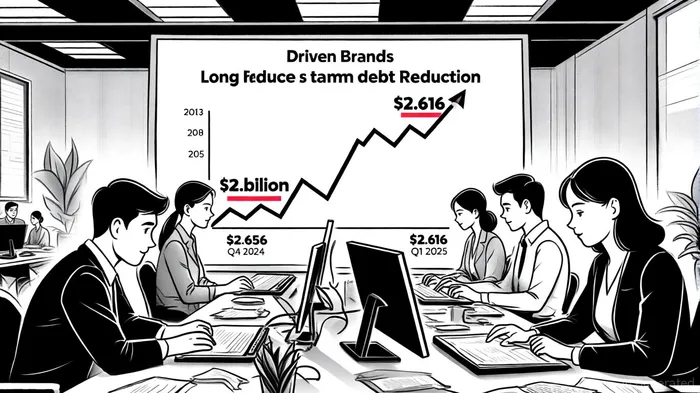

In early 2025, Driven BrandsDRVN-- completed a $500 million term loan, with proceeds allocated to general corporate purposes, including funding future acquisitions, as shown in Driven Brands' Q1 2025 slides. This move followed the successful sale of its car wash business in April 2025 for $385 million, as reported by Autobody News, which directly reduced long-term debt from $2.656 billion to $2.616 billion. The transaction underscores the company's focus on shedding non-core assets to streamline operations and improve financial flexibility.

The refinancing strategy extends beyond the term loan. In July 2024, Driven Brands executed a $275 million securitization issuance to refinance its Series 2018-1 Class A-2 Notes, which carried a 6.372% coupon and a seven-year tenor, according to a Driven Brands press release. Concurrently, the company expanded its Variable Funding Notes capacity by $400 million, refinancing undrawn Series 2019-3 Class A-1 Notes. These actions demonstrate a proactive approach to managing debt maturity profiles and reducing reliance on higher-cost financing.

Leverage Reduction and Credit Market Positioning

Despite these efforts, Driven Brands' leverage remains elevated. As of Q1 2025, the company reported a leverage ratio of 4.3x, driven by total debt of $2.616 billion and adjusted EBITDA of approximately $608 million (calculated from debt-to-EBITDA ratio). However, progress is evident: by Q2 2025, the leverage ratio had improved to 4.1x, with total debt declining to $2.38 billion and adjusted EBITDA rising to $533 million.

The company has set a clear target to reduce leverage to below 3x by the end of 2026, according to its Q1 2025 earnings. This goal aligns with broader industry trends, where automotive service operators are under pressure to demonstrate operational efficiency and debt discipline to maintain favorable credit ratings. Driven Brands' refinancing initiatives, coupled with the car wash divestiture, position it to meet this target while preserving capacity for strategic acquisitions.

Strategic Rationale and Sector Implications

The automotive services sector is highly competitive, with margins often constrained by labor costs and supply chain volatility. Driven Brands' focus on capital structure optimization reflects a recognition of these challenges. By reducing leverage, the company can allocate more resources to enhancing franchisee profitability-a key driver of long-term growth. For instance, the 2025-Q4 strategic plan emphasizes integrating its diverse portfolio to drive operational synergies, as noted in a Driven Brands SWOT.

From a credit market perspective, Driven Brands' actions are likely to improve its borrowing terms in future refinancings. Lower leverage ratios typically result in more favorable interest rates and covenants, which are critical for a company with a history of high debt levels. The recent $500 million securitization under Series 2025-1, which refinanced existing debt and funded general corporate purposes, further illustrates this strategy.

Conclusion

Driven Brands' 2025 debt refinancing and asset divestiture represent a calculated effort to balance growth ambitions with financial prudence. While the company's leverage remains above industry benchmarks, the trajectory of debt reduction and improved liquidity positions it to navigate sector headwinds. For investors, the key takeaway is that Driven Brands is prioritizing long-term stability over short-term expansion, a strategy that could enhance creditworthiness and unlock value as the automotive services sector evolves.

Comentarios

Aún no hay comentarios