DraftKings and the Impact of Phantom Tax Risks on DFS Operator Valuation

The daily fantasy sports (DFS) industry, once a high-growth frontier for digital entertainment, now faces a perfect storm of regulatory uncertainty and hidden tax liabilities. For operators like DraftKingsDKNG--, these pressures are reshaping stock fundamentals and forcing strategic recalibrations. The Trump administration's 2025 tax overhaul, state-level crackdowns, and evolving compliance costs are creating a landscape where DFS operators must balance innovation with survival.

The Tax Code's Silent Squeeze

The One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, has introduced a seismic shift for DFS operators. By capping gambling861167-- loss deductions at 90%, the law effectively raises the tax burden on bettors who break even or lose money. According to a report by Sportico, this change could deter participation in DFS and other gambling activities, reducing the user base for platforms like DraftKings . For operators, the indirect impact is clear: lower engagement translates to reduced handle and revenue.

Compounding this, the IRS now requires meticulous record-keeping for gambling losses, a bureaucratic hurdle that could drive users to offshore or unregulated platforms . As Kahntaxlaw notes, the provision is expected to generate $1.14 billion in additional tax revenue between 2026 and 2034, but at the cost of stifling legal gambling markets .

State-Level Regulatory Volatility

While federal inaction persists, states are acting unilaterally. California's Attorney General, Rob Bonta, declared DFS illegal in July 2025, vowing to enforce the ban by shutting down operators like DraftKings . This move mirrors similar crackdowns in Texas and New Mexico, where Jackpocket recently exited due to regulatory pressures .

To offset rising state tax rates, DraftKings has pioneered a novel approach: a tax surcharge on winning wagers in high-tax states like New York, Illinois, Pennsylvania, and Vermont . This strategy, while innovative, risks alienating customers and eroding trust. As Action Network highlights, it marks a first for U.S. sportsbooks, reflecting the industry's desperation to adapt .

Financial Impacts and Strategic Shifts

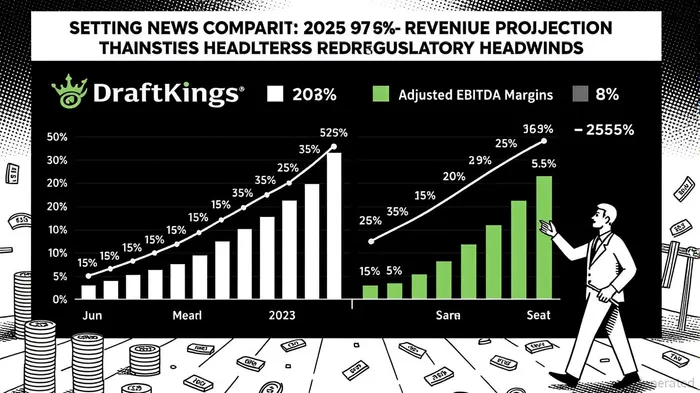

The financial toll of these challenges is evident. DraftKings reported a $170 million revenue headwind and $111 million EBITDA drag in Q1 2025 due to regulatory and tax changes . Despite this, the company maintained a 20% year-over-year revenue increase to $1.409 billion, driven by sportsbook growth and AI-driven cost efficiencies . However, analysts project a 32% revenue growth for 2025, with adjusted EBITDA guidance revised to $800–900 million—a 13.5% margin—down from earlier forecasts .

Flutter Entertainment, another DFS giant, has also faced headwinds. The company introduced a $0.50 wager fee in Illinois to counteract regulatory costs, a move that boosted operating expenses but preserved market share . Flutter's 2025 guidance includes 28% U.S. revenue growth and a 15.2% EBITDA margin, up from 8.7% in 2024 .

Diversification and Technological Resilience

To mitigate risks, DFS operators are doubling down on diversification. DraftKings has expanded into iGaming, live betting, and the DraftKings+ platform, while exploring acquisition targets like Railbird Exchange to enter prediction markets . Similarly, FlutterFLUT-- has leveraged AI and automation to reduce customer service costs and improve promotional efficiency .

These strategies reflect a broader industry trend: prioritizing high-margin, low-regulation segments. As Data Insights Market notes, DFS operators are increasingly adopting an “AI-first” approach to pricing and risk management, enabling them to navigate unpredictable customer outcomes and regulatory shifts .

Market Reactions and Investor Sentiment

The stock market has responded with mixed signals. DraftKings' shares rose 15% in three months as of June 2025, buoyed by Q1 results and a “Strong Buy” analyst rating . However, the company's net debt-to-EBITDA ratio remains elevated at 1.5x, raising concerns about leverage . Flutter, meanwhile, trades at $267.98, with a net debt-to-EBITDA of 1.4x and $3.5 billion in cash on hand, signaling stronger financial flexibility .

Conclusion: Navigating a Fragmented Future

For DFS operators, the path forward is fraught with uncertainty. Regulatory fragmentation and tax liabilities will continue to pressure valuations, but companies that innovate in compliance, diversify revenue streams, and leverage technology stand to outperform. Investors must weigh the risks of regulatory overreach against the potential for long-term resilience in a sector that remains resilient despite headwinds.

As the DFS industry evolves, the ability to adapt to “phantom tax risks”—those hidden costs and compliance burdens—will define the next phase of growth. For DraftKings and its peers, the stakes have never been higher.

Source:

[1] Gambling Reacts to Proposed Trump Tax Changes, [https://www.sportico.com/business/sports-betting/2025/donald-trump-tax-bill-gambling-losses-deductions-1234859009/]

[2] DraftKings Inc.DKNG--, [https://www.datainsightsmarket.com/companies/DKNG]

[3] Up 15% in 3 Months, Is It Too Late to Buy DraftKings Stock?, [https://finance.yahoo.com/news/15-3-months-too-buy-183401006.html]

[4] One Big Beautiful Bill Tax Act – How Can You Benefit?, [https://www.kahntaxlaw.com/one-big-beautiful-bill-tax-act-how-can-you-benefit-4/]

[5] US Sportsbook Leaders Flutter and DraftKings Post Double ... [https://buildingbenjamins.com/stock-thoughts/us-sportsbook-leaders-flutter-and-draftkings-post-double-digit-growth-guidance/]

Comentarios

Aún no hay comentarios