Dow Inc.'s Strategic Crossroads: Assessing Catalysts for Value Unlocking Amid Sector Headwinds

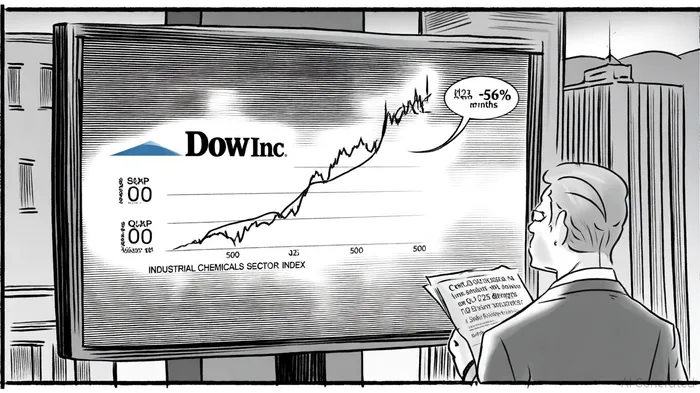

Dow Inc. (DOW) has endured a punishing 12-month stretch, with its shares plummeting 56% compared to the S&P 500's 17% gain and lagging even its industrial chemicals peers[1]. This underperformance reflects a confluence of macroeconomic headwinds, sector-specific pressures, and internal strategic recalibration. Yet, for investors willing to parse the noise, the company's aggressive cost-cutting, asset rationalization, and sustainability-driven innovation may yet unlock value—if the timing aligns with a sector poised for stabilization.

Sector Dynamics: A Landscape of Overcapacity and Regulatory Turbulence

The industrial chemicals sector, part of the broader Materials industry, remains a "Marketperform" segment relative to the S&P 500, according to Schwab's 2025 outlook[4]. Global overcapacity—particularly in China—has depressed margins, while U.S. tariffs and European demand softness have compounded challenges[1]. For instance, the German Chemicals Industry Association (VCI) reported a 3.8% decline in Q2 2025 production year-over-year, with capacity utilization hitting levels not seen since 1991[1]. Meanwhile, Asia's surplus chemicals capacity now exceeds 226 million tonnes, intensifying global price competition[1].

Amid these pressures, sustainability and digital transformation have emerged as critical differentiators. Companies investing in circular economy models and low-carbon technologies are better positioned to navigate regulatory shifts and consumer demand for eco-friendly products[4]. Dow's alignment with these trends—through initiatives like REVOLOOP™ recycled plastics and electric steam crackers—suggests a strategic pivot toward long-term resilience[2].

Dow's Strategic Overhaul: Cost Discipline and Capital Reallocation

Dow's Q2 2025 earnings report underscored the urgency of its transformation. A 3% year-over-year decline in net sales to $10.4 billion, coupled with a GAAP net loss of $290 million, prompted a $6 billion "cash support" plan[3]. Key components include:

- Dividend Reduction: A $500 million cut to preserve liquidity[3].

- Cost-Savings Target: $1 billion by 2026, with $400 million achieved in 2025 alone[3].

- Asset Sales: A $2.4 billion stake in Gulf Coast infrastructure assets (Diamond Infrastructure Solutions) and a $1 billion legal judgment[3].

- Operational Rationalization: Closure of three European upstream facilities, expected to yield $200 million in annual EBITDA by 2029[3].

These measures aim to stabilize cash flow while addressing structural inefficiencies. The Poly-7 polyethylene train in Freeport, Texas—a fully integrated downstream project—is a rare bright spot, with management projecting margin expansion as production ramps[3]. However, the delayed Fort Saskatchewan Path2Zero project—a $1 billion EBITDA driver—highlights the trade-offs between short-term liquidity and long-term decarbonization goals[4].

Analyst Sentiment: Cautious Optimism Amid Execution Risks

Despite these steps, analyst sentiment remains split. As of September 2025, DOW carries a "Hold" consensus rating, with 13 of 19 analysts recommending neutrality, 4 advocating "Buy," and 2 issuing "Sell" ratings[4]. The average price target of $30.74 implies a 25.58% upside from its current $24.48 level[4]. Yet, recent downgrades—such as UBS lowering its target to $24.00 from $28.00—reflect skepticism about near-term execution[4].

The critical question for investors is whether Dow's cost discipline and asset sales can catalyze a turnaround before sector conditions deteriorate further. Management's guidance for $800 million in Q3 2025 EBITDA—a $100 million sequential improvement—hinges on margin recovery and project ramp-ups[4]. If achieved, this could signal a bottoming-out of the current downcycle.

Strategic Investment Timing: Balancing Short-Term Pain and Long-Term Gain

For value-oriented investors, DOW's discounted valuation—trading at a 40% discount to its 5-year average P/E—presents an intriguing case. However, timing is paramount. The industrial chemicals sector's projected 2.3% growth in 2025, while modest, is constrained by overcapacity and trade tensions[1]. A near-term catalyst could emerge if global demand stabilizes in 2026, particularly in Asia, where infrastructure spending and green energy transitions may drive chemical demand[5].

Dow's alignment with circular economy trends—such as its partnerships with Mura Technology and Valoregen—also positions it to benefit from regulatory tailwinds. For instance, North American recycled LDPE pellet prices have surged due to policy-driven PCR (post-consumer resin) mandates[1]. If Dow can scale its REVOLOOP™ technology to capture this market, it could unlock incremental margins.

Conclusion: A Calculated Bet on Execution

Dow's strategic overhaul is a high-stakes gamble. The company's aggressive cost-cutting and asset sales provide near-term liquidity but risk underinvestment in innovation. Conversely, its sustainability initiatives and digital transformation efforts—while laudable—require time to materialize into earnings. For investors, the key is to monitor two metrics:

1. EBITDA Recovery: Can Dow deliver the projected $100 million sequential improvement in Q3 2025?

2. Sector Stabilization: Will global overcapacity ease by mid-2026, or will trade restrictions further depress demand?

If both checks align, DOW's discounted valuation and strategic repositioning could offer compelling upside. But until then, the "Hold" rating reflects a sector and company navigating a crossroads where patience and precision are paramount.

Comentarios

Aún no hay comentarios