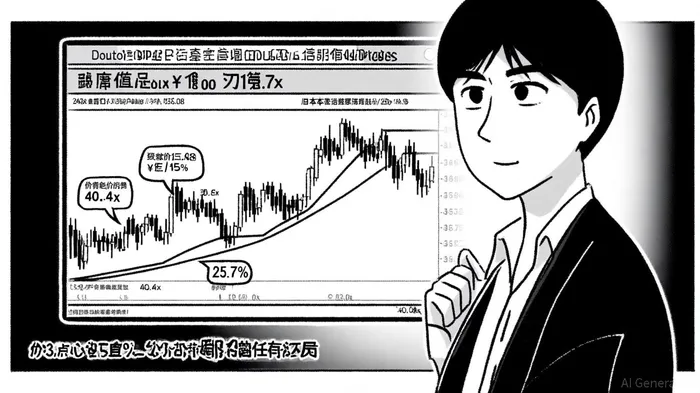

Doutor Nichires (TSE:3087): A Case for Undervaluation in Japan's Hospitality Sector

In the competitive landscape of Japan's hospitality sector, Doutor Nichires Holdings (TSE:3087) emerges as a compelling case of valuation mispricing. Data from SimplyWall St indicates that the company's shares trade at a 25.7% discount to their estimated intrinsic value of ¥3,315.08, a disparity that warrants closer scrutiny[1]. This undervaluation is further underscored by its Price-to-Earnings (P/E) ratio of 15.7x, which lags significantly behind both its industry peers' average of 40.4x and the broader Japanese hospitality sector's P/E of 24x[1]. Such a gap suggests a disconnect between the company's fundamentals and market perception.

Earnings Narrative: A Tale of Underappreciated Strengths

Doutor Nichires' earnings narrative reveals a business with robust operational performance. The company reported trailing twelve-month revenue of ¥153.3 billion and net income of ¥6.6 billion, supported by a diversified portfolio spanning coffee shops, restaurants, and confectionery products[1]. Its EV/EBITDA ratio of 5.6 is another outlier, dwarfed by peers such as Mos Food Services (34.5x) and Kura Sushi (61.2x)[4]. This metric, which measures enterprise value relative to earnings before interest, taxes, depreciation, and amortization, highlights Doutor Nichires' efficiency in converting earnings into market value.

The company's financial health further strengthens its case. With a net cash position of ¥30.5 billion[3], Doutor Nichires is insulated from liquidity risks, a critical advantage in a sector prone to cyclical demand shifts. Its Price-to-Book (P/B) ratio of 1.1, calculated as a market cap of ¥109.3 billion divided by equity book value of ¥100.9 billion[1], suggests that investors are paying little premium for its tangible assets-a contrast to peers who often trade at higher multiples for similar asset bases.

Valuation Mispricing: Why the Gap?

The disconnect between Doutor Nichires' valuation and its fundamentals may stem from market skepticism about its growth trajectory. While the company operates a well-established brand portfolio-including Italian coffee, American food, and Asian noodle chains[2]-its expansion potential could be perceived as limited compared to peers with stronger international footprints. However, this perspective overlooks the company's strategic focus on domestic market penetration and its ability to leverage its integrated supply chain for cost efficiency[2].

Moreover, the Japanese hospitality sector's average P/E of 24x[1] implies that investors are willing to pay a premium for growth stories, even if they come with higher risk. Doutor Nichires' lower P/E and EV/EBITDA ratios suggest it is being penalized for perceived conservatism, despite its strong balance sheet and consistent earnings. This mispricing creates an opportunity for value investors who can capitalize on the market's underappreciation of its stable cash flows and operational discipline.

Risks and Considerations

While the valuation case is compelling, investors must weigh potential risks. The hospitality sector is sensitive to economic downturns and shifting consumer preferences, as evidenced by the post-pandemic recovery challenges faced by many operators. Additionally, Doutor Nichires' reliance on domestic markets exposes it to Japan-specific macroeconomic factors, such as demographic trends and tourism fluctuations.

Conclusion: A Mispriced Opportunity

Doutor Nichires' valuation metrics-particularly its P/E and EV/EBITDA ratios-position it as a candidate for undervaluation relative to its peers. With a market cap of ¥108.03 billion[1] and a strong net cash position, the company offers a margin of safety that aligns with value investing principles. For investors seeking exposure to Japan's hospitality sector, Doutor Nichires represents a compelling opportunity to capitalize on a mispricing that may correct as the market re-evaluates its earnings potential and strategic strengths.

Comentarios

Aún no hay comentarios