Dollar Tree, Inc.'s Fiscal Year 2026 Earnings Guidance: Assessing the Sustainability and Growth Potential of a Resilient Discount Retail Model Amid Macroeconomic Pressures

Introduction

In an era of persistent inflation, shifting consumer spending patterns, and intensifying competition, Dollar TreeDLTR--, Inc. (DLTR) has positioned itself as a resilient player in the discount retail sector. With its FY2026 earnings guidance projecting 4%-6% comp sales growth and adjusted EPS of $5.32-$5.72, per Dollar Tree's investor day release, the company is navigating macroeconomic headwinds through strategic pricing, operational efficiency, and a reimagined value proposition. This analysis evaluates whether Dollar Tree's core discount retail model is sustainable and growth-oriented, and whether its strategic positioning justifies a bullish investment outlook for Q4 2025 entry.

Earnings Guidance and Strategic Resilience

Dollar Tree's FY2026 guidance reflects confidence in its ability to mitigate cost pressures while maintaining pricing power. The company raised its full-year EPS forecast to $5.32-$5.72, citing improved gross margins (34.4% in Q2 2025, according to a TradingKey analysis) and cost management initiatives. This optimism is underpinned by a $1 billion share repurchase program and $425 million in tax benefits from the Family Dollar divestiture (per the investor day release). However, recent downward revisions to FY2026 EPS (now $5.73-$6.13, per a financial analysis paper) highlight challenges such as lower-margin grocery expansion and operational costs. Despite these adjustments, Dollar Tree's long-term EPS growth target of 8%-10% (as noted in the investor day release)-bolstered by discrete cost benefits in FY2026-signals a disciplined approach to profitability.

Operational Efficiency and Competitive Positioning

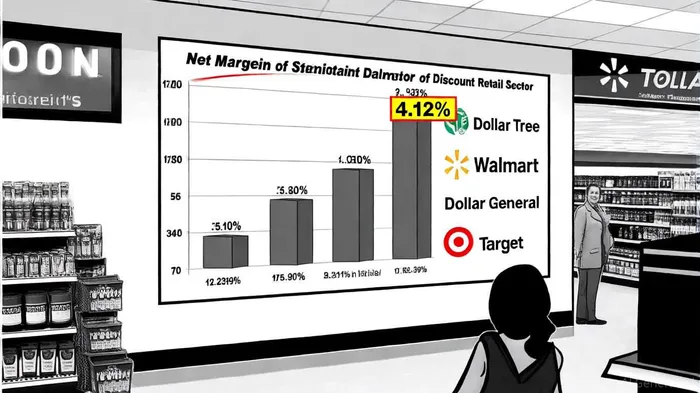

Dollar Tree's operational efficiency metrics are central to its sustainability. The company plans to renegotiate 75% of supplier contracts to reduce costs by 5% by Q3 2025, automate three distribution centers to boost throughput by 15%, and leverage AI-driven demand forecasting to cut stock-outs by 25%, according to a SWOT analysis. These initiatives are critical in maintaining a 4.12% net margin in Q2 2025, per CSIMarket data, outperforming competitors like Walmart (4.01%) and Dollar General (4.05%) (CSIMarket).

Strategically, Dollar Tree is redefining its value proposition with the "Dollar Tree 3.0" model, introducing multi-price products (e.g., $3 cleaning supplies, $5 hammers) to attract affluent shoppers while retaining price-sensitive customers, as its 3.0 strategy explains. This shift has already driven a 2% same-store sales increase in adopting stores (WebProNews), demonstrating adaptability to inflation-driven consumer behavior.

Macroeconomic Adaptability and Risk Mitigation

Dollar Tree's macroeconomic adaptability is evident in its proactive cost management and capital allocation. The company's debt-to-equity ratio of 2.71 as of July 2025 remains high but is offset by $1.418 billion in net cash from operating activities in 2024, per the Q2 2025 results, and a $2.5 billion share repurchase authorization (Q2 2025 results). Additionally, the tornado-related $117 million distribution center loss in Q3 2025, reported in Q3 2025 earnings, was fully insured and underscores its risk mitigation capabilities.

The company's focus on rural market expansion (800 new stores planned, per WebProNews) and high-margin categories like health and beauty (WebProNews) further insulates it from urban retail saturation and e-commerce competition. Analysts note that Dollar Tree's 12-15% EPS CAGR target for 2026-2028 (investor day release) hinges on sustained cost discipline and the absence of discrete expenses like tariff mitigation (investor day release).

Analyst Sentiment and Price Targets

Analyst sentiment for Dollar Tree in Q4 2025 is mixed but cautiously optimistic. A consensus of 19 analysts assigns an average price target of $109.28 (14.72% upside from current levels, per the MarketBeat forecast), with high and low estimates at $140 and $70, respectively (MarketBeat). Notable upgrades include JPMorgan raising its target to $140 (MarketBeat) and Goldman Sachs to $130 (MarketBeat), while downgrades like Jefferies' $70 target (MarketBeat) reflect concerns over margin pressures. Despite the "Hold" consensus (MarketBeat), the company's strong cash flow, strategic clarity, and margin resilience justify a bullish outlook.

Conclusion: A Strong Buy for Q4 2025 Entry

Dollar Tree's FY2026 guidance, operational efficiency, and strategic innovation position it as a compelling investment. While macroeconomic risks and margin pressures persist, the company's disciplined cost management, margin leadership, and adaptive pricing model mitigate these challenges. With a robust balance sheet, clear growth levers (e.g., multi-price formats, rural expansion), and analyst price targets averaging $109.28 (MarketBeat), Dollar Tree offers a strong buy opportunity for investors seeking exposure to a resilient discount retail model.

Comentarios

Aún no hay comentarios