The Dollar's Path Ahead: Labor Data, Fed Policy, and Central Bank Divergence

The U.S. dollar’s trajectory in 2025 has been shaped by a confluence of weak labor data, a dovish Federal Reserve, and divergent central bank policies. As the September 5 release of the August 2025 Nonfarm Payrolls (NFP) report looms, investors must navigate a landscape where the dollar’s positioning hinges on the interplay of these forces.

Labor Data: A Cooling Labor Market and Rate-Cut Expectations

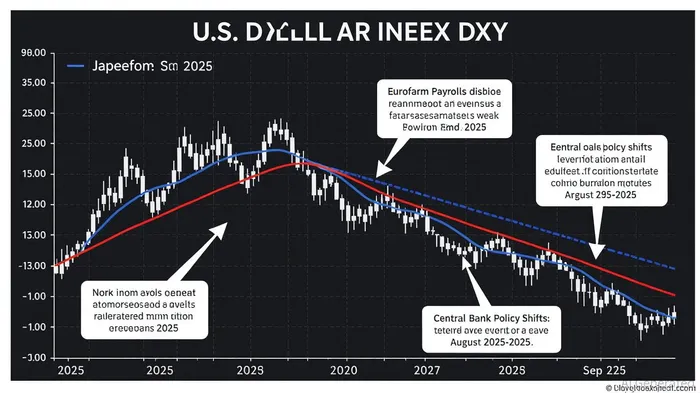

Recent NFP reports have painted a starkly mixed picture of the U.S. economy. The August 2025 figure of just 22,000 jobs added—far below the 75,000 forecast—marked a significant slowdown from July’s revised 73,000 gain [1]. This weak performance, coupled with an expected rise in the unemployment rate to 4.3% (its highest since 2021) and a deceleration in average hourly earnings growth to 3.7% [4], has reinforced market expectations for Fed easing.

Data from Trading Economics underscores the sectoral imbalances: gains in healthcare and social assistance were offset by job losses in manufacturing, government, and mining [1]. Such fragmentation suggests a labor market under structural strain, not merely cyclical softness. As a result, the dollar has depreciated against major currencies, with the DXY index trading with a bearish bias ahead of further policy easing [4].

Fed Policy: A Dovish Pivot and Market Pricing

The Federal Reserve’s policy trajectory has shifted decisively toward easing. Markets currently price in 60 basis points (bps) of Fed Fund rate cuts by year-end, with a 98% probability of a 25 bps cut in September [1]. This starkly contrasts with the hawkish positioning seen in August 2024, when a strong NFP report had pushed expectations for prolonged tightening [1].

The ADP private payrolls report (54,000 added in August) and the Beige Book’s indication of firms hesitating to hire further validate the Fed’s data-dependent approach [2]. While a strong NFP report might not alter the September cut narrative, it could trigger a hawkish repricing in longer-dated rates. Conversely, another weak report could accelerate expectations for a third rate cut by year-end or even a 50 bps cut in September, further pressuring the dollar [4].

Central Bank Divergence: A Tale of Two Cycles

The Fed’s dovish pivot stands in sharp contrast to the policy trajectories of its global counterparts. The European Central Bank (ECB) has signaled it will maintain rates in September, with policy makers near the end of their easing cycle [3]. This divergence has bolstered the euro against the dollar, as investors anticipate a narrowing of yield differentials. Similarly, the Bank of Japan (BoJ) remains committed to a gradual tightening path, though its actions are contingent on the Fed’s timing [3].

Meanwhile, the Bank of England (BoE) and other G10 central banks, including the Bank of Canada (BoC) and Riksbank, are also navigating easing cycles, albeit at a slower pace. The BoC and Riksbank each face a roughly 50% chance of a 25 bps cut in September [1]. This cluster of policy decisions creates a volatile backdrop for the dollar, as divergent monetary trajectories amplify currency fluctuations.

Strategic Positioning: Navigating the Dollar’s Weakness

For investors, the dollar’s near-term trajectory suggests a strategic shift toward hedging against further depreciation. Key considerations include:

1. Currency Pairs: Long positions in the euro and yen could benefit from the Fed’s easing cycle relative to the ECB and BoJ’s more neutral stances [2].

2. Gold and Equities: A weaker dollar has already driven gold prices near record highs, as monetary easing boosts demand for safe-haven assets [4]. Equities, particularly in sectors sensitive to rate cuts (e.g., housing, consumer discretionary), may also outperform.

3. FX Carry Trades: With the Fed’s rate cuts priced in, carry trades involving shorting the dollar against higher-yielding currencies (e.g., the Australian dollar) could gain traction.

Geopolitical Risks and the Dollar’s Long-Term Outlook

Beyond monetary policy, structural risks loom over the dollar’s global role. Concerns about the Fed’s independence—exemplified by President Trump’s controversial firing of Governor Lisa Cook—and the imposition of steep tariffs are eroding confidence in the dollar as a reserve currency [4]. While a global recession could temporarily reinforce the dollar’s safe-haven appeal, these developments suggest a longer-term weakening trend.

Conclusion

The dollar’s path ahead is inextricably linked to the interplay of weak labor data, Fed easing, and central bank divergence. As the September NFP report approaches, investors must balance short-term volatility with long-term structural shifts. Strategic positioning in currency pairs, gold, and equities offers a pathway to capitalize on the dollar’s potential depreciation while mitigating risks from geopolitical uncertainties.

Source:

[1] United States Non Farm Payrolls, [https://tradingeconomics.com/united-states/non-farm-payrolls]

[2] NFP Preview: US Jobs Report & Implications for the DXY, [https://www.marketpulse.com/markets/nfp-preview-us-jobs-report-implications-for-the-dxy-gold-xauusd-dow-jones-djia/]

[3] Monthly Foreign Exchange Outlook, [https://www.mufgresearch.com/fx/monthly-foreign-exchange-outlook-september-2025/]

[4] Dollar's Rebound: Tactical Recovery or Structural Decline?, [https://www.marketpulse.com/markets/dollar-rebound-tactical-vs-structural-decline/]

Comentarios

Aún no hay comentarios