Diversified Healthcare Trust's Strategic Rebalancing: Navigating Risks and Opportunities in Q3 2025

The healthcare real estate sector is undergoing a seismic shift, driven by demographic tailwinds, technological innovation, and a redefinition of care delivery models. Against this backdrop, Diversified Healthcare Trust (DHC) finds itself at a critical inflection point. As the company prepares to unveil its Q3 2025 earnings on November 4, 2025, the question looms: Can DHC's aggressive strategic overhauls offset its structural vulnerabilities and position it as a resilient player in a high-stakes market?

Strategic Rebalancing: From Senior Housing to Medical Office and Life Science

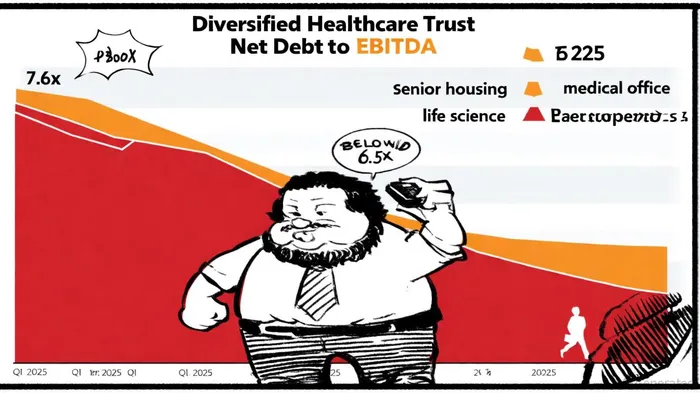

DHC's Q3 2025 earnings call will likely spotlight its ongoing portfolio transformation. The company has committed to divesting underperforming senior housing assets, a move aimed at reallocating capital to higher-growth sectors like medical office buildings (MOBs) and life science properties. According to the Diversified Healthcare Trust SWOT report, this pivot is not merely tactical but existential. With its Net Debt to EBITDA ratio at 7.6x-a level that constrains financial flexibility-the trust must demonstrate that its asset sales can fund a deleveraging strategy while generating returns for shareholders.

The logic is compelling. MOBs and life science properties are benefiting from a surge in demand driven by outpatient care expansion and biotech innovation. Data from MarketBeat indicates that DHC's Q1 2025 revenue of $386.86 million exceeded expectations, suggesting that early-stage optimizations-such as operational efficiency improvements in its core portfolio-are yielding results. However, the success of this strategy hinges on execution. The trust must navigate a competitive acquisition landscape, where rival REITs and private equity firms are also targeting high-quality healthcare assets.

Historical data on DHC's earnings events from 2022 to 2025, as summarized in the Businesswire release, reveals an average 1-day excess return of approximately +1.7% following announcements, though statistical significance was low across all holding windows. While this suggests limited immediate market reaction, the strongest relative drift occurred around 20 trading days post-release, with cumulative returns of ~+12% versus ~+4.5% for the benchmark. This pattern hints at a delayed market reassessment of DHC's strategic direction, though the 50% win rate across events underscores the absence of a reliable directional edge.

Risk Mitigation: Debt, Operating Costs, and Strategic Uncertainty

While DHC's asset-level strategy is ambitious, its risk profile remains precarious. The company's Senior Housing Operating Portfolio (SHOP) continues to underperform, with elevated property-level operating expenses-particularly labor costs-eroding profitability, according to the Diversified Healthcare Trust SWOT report. This is a systemic challenge: The healthcare sector's labor intensity, compounded by inflationary pressures, has strained margins across the industry. For DHCDHC--, the urgency to shed these liabilities is acute.

The termination of the proposed merger with OPI in 2025 further complicates the narrative. As noted in the trust's investor materials, that development created market uncertainty and raised questions about DHC's long-term vision. Yet, the company's leadership appears undeterred. CEO Christopher Bilotto and CFO Matthew Brown have emphasized a disciplined approach to debt reduction, targeting a Net Debt to EBITDA ratio below 6.5x by year-end, as described in the earnings call notice. Whether this target is achievable will depend on the pace of asset sales and the pricing environment in the current market.

Growth Potential: A High-Stakes Bet on the Future of Healthcare

DHC's Q3 2025 earnings report will serve as a litmus test for its strategic credibility. Analysts project an EPS of $0.10 for the quarter, up from $0.06 in Q1 2025, according to MarketBeat. If realized, this growth would validate the trust's pivot to MOBs and life science properties. However, the path to sustained profitability remains fraught.

A critical factor will be DHC's ability to secure favorable financing terms. With interest rates remaining elevated, refinancing existing debt-or acquiring new assets-could prove costly. Additionally, the trust must prove that its operational efficiency initiatives, such as enhanced asset management and performance reviews, can consistently boost net operating income (NOI), as shown in the SEC filing.

Conclusion: A Portfolio in Transition

Diversified Healthcare Trust's Q3 2025 earnings will be a pivotal moment in its transformation. The company's strategic rebalancing-from senior housing to medical office and life science assets-positions it to capitalize on long-term healthcare trends. Yet, its high leverage, operating inefficiencies, and the lingering shadow of the OPI merger termination create a volatile backdrop.

For investors, the key takeaway is clear: DHC's success will hinge on its ability to execute with precision. If the trust can reduce its debt burden, accelerate asset sales, and demonstrate NOI growth in its newer sectors, it may yet emerge as a formidable player in the evolving healthcare real estate market. But for now, the jury remains out-and the November 4 earnings report will offer the first definitive verdict.

Comentarios

Aún no hay comentarios