Diverging U.S. Equity Market Trends: Sector Rotation and Valuation Disparities in Q3 2025

The U.S. equity market in Q3 2025 has been defined by a paradox: resilience amid volatility and divergent sector performance. While the S&P 500 has maintained strength, corporate earnings reaching record highs[2], the underlying dynamics reveal a fragmented landscape. Sector rotation and valuation disparities have become central themes, driven by macroeconomic uncertainty, trade policy shifts, and divergent investor sentiment.

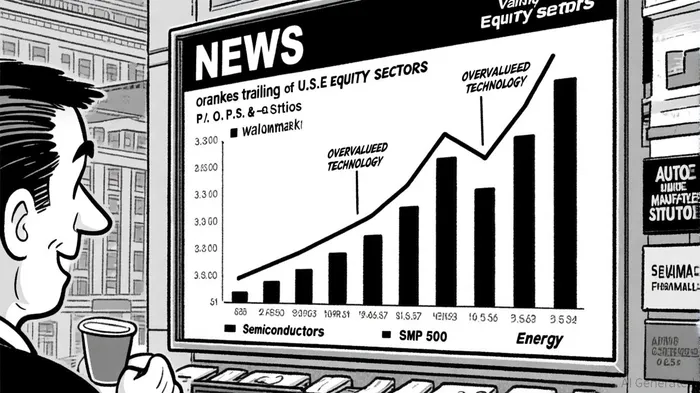

Sector Rotation: A Tale of Caution and Opportunity

The Schwab Center for Financial Research's "Marketperform" rating for all 11 sectors underscores the market's hesitancy to commit to clear winners or losers[4]. This neutrality reflects the fog of uncertainty surrounding the White House's new global tariff policy, which has left analysts struggling to assess sector-specific impacts[1]. For instance, Energy and Financials have emerged as relative bargains, with P/E ratios of 17.47 and 18.09, respectively[3], while sectors like Information Technology (38.09) and Semiconductors (46.61) trade at premium valuations[2].

The rotation trends are further amplified by fund flows. In July 2025, U.S. equity categories experienced outflows, with leveraged inverse tech funds attracting inflows—a sign of deteriorating sentiment toward overvalued tech stocks[1]. Meanwhile, defensive sectors like Consumer Staples (23.02 P/E) and Utilities (21.17 P/E) have drawn cautious capital, reflecting a flight to stability amid geopolitical tensions[3].

Valuation Disparities: Overpriced Optimism vs. Earnings-Driven Justification

The S&P 500's forward P/E of 27.35—a level typically reserved for periods of extreme optimism—highlights the market's uneven valuation landscape[2]. While the Information Technology sector has justified its elevated P/E through robust profit growth (despite a 7.9% decline in its multiple in 2025[2]), other sectors appear disconnected from fundamentals. Industrials and Consumer Discretionary, for example, have seen their P/E ratios rise by 17% and 15%, respectively, without commensurate earnings growth[2].

This divergence is starkly illustrated by the Auto Manufacturers sector, which trades at a mere 8.32 P/E—a discount that suggests investor skepticism about near-term demand[3]. In contrast, Semiconductors and Health Information Services command P/E ratios of 46.61 and 43.24, respectively[2], reflecting bets on long-term innovation cycles.

Strategic Implications for Investors

The current environment demands a nuanced approach. For long-term investors, volatility created by tariff uncertainty and sector rotation presents opportunities to add exposure to fundamentally sound stocks at attractive valuations[2]. Defensive sectors like Utilities and Consumer Staples, though overvalued by historical standards, offer stability in a high-risk environment[3]. Conversely, investors in overvalued growth sectors (e.g., Technology) must weigh the risks of a potential earnings slowdown against the sector's innovation-driven momentum[1].

Fund flows also suggest a shift in capital toward foreign assets and derivative-income strategies. In Q3 2025, European stocks—particularly in banking and aerospace—have shown resilience, offering diversification benefits[4]. Covered-call strategies, which attracted $7.5 billion in July[1], further underscore the demand for downside protection.

Conclusion

The U.S. equity market in Q3 2025 is a mosaic of contradictions: optimism in tech, caution in industrials, and a search for stability in defensive sectors. As trade policy clarity emerges and macroeconomic signals evolve, investors must balance growth potential with valuation discipline. The key lies in leveraging sector rotation to capitalize on mispricings while hedging against the risks of overvalued markets.

Comentarios

Aún no hay comentarios