Disruption in Financial Services: The Rise of Non-Bank Financial Powerhouses

The financial services landscape is undergoing a seismic shift, driven by the rapid ascent of non-bank financial institutions (NBFIs). These entities-encompassing fintechs, big tech firms, and alternative lenders-are reshaping traditional paradigms of credit, payments, and wealth management. For investors, this evolution demands a strategic reevaluation of capital allocation and risk diversification.

The Market Share Revolution

By 2023, NBFIs had captured nearly 50% of global financial services, a stark contrast to their 43% share during the 2008 financial crisis, according to the IMF explainer. This growth is not merely a statistical anomaly but a structural transformation fueled by technological innovation and evolving consumer preferences. For instance, the global payments market, valued at USD 3.12 trillion in 2025, is projected to surge to USD 5.34 trillion by 2030, growing at a compound annual rate of 11.29%, according to a Mordor report. Digital wallets, now the preferred payment method in Asia-Pacific and Europe, exemplify this shift, with adoption rates exceeding 50% in key markets, as the Mordor report finds.

The lending sector further underscores this disruption. In 2025, fintech platforms accounted for 63% of U.S. personal loan origination, while 55% of small businesses in developed economies accessed loans through these platforms, according to a Coinlaw analysis. Peer-to-peer lending alone reached $19 billion in value, with blockchain and AI-driven credit scoring reducing default rates to below 1% in some cases, per Coinlaw's data. These advancements are not confined to niche markets; they are redefining accessibility, efficiency, and risk management in financial services.

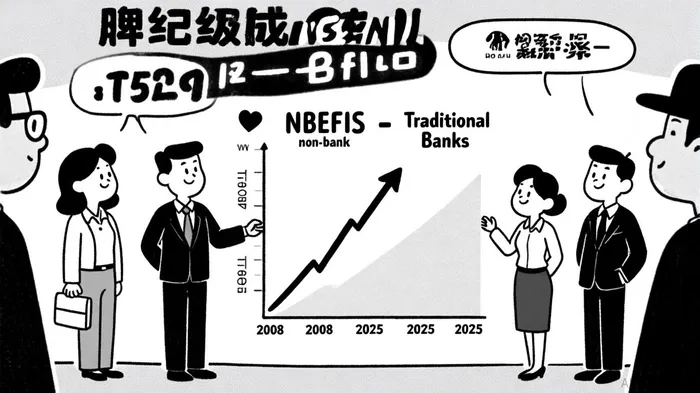

Strategic Capital Reallocation

The rise of NBFIs necessitates a recalibration of investment strategies. Traditional banks, which grew at a modest 3.3% annualized rate between 2012 and 2025, now face stiff competition from non-depository financial institutions (NDFIs), whose lending expanded at 26% annually over the same period, according to the St. Louis Fed analysis. For investors, this disparity highlights the need to prioritize sectors where NBFIs are outpacing incumbents.

Consider the wealth management segment: passive investment vehicles like index funds managed 48% of U.S. assets under management by 2023, per the IMF explainer. Fintechs are further leveraging AI and machine learning to democratize access to personalized financial planning, a trend Deloitte predicts will drive a 20–40% reduction in software investment costs for banks by 2028, as noted in the IMF explainer. Investors who allocate capital to AI-driven fintech platforms or embedded finance models-where financial services are integrated into non-financial platforms-are positioning themselves at the forefront of this innovation.

Risk Diversification in a Fragmented Ecosystem

While the growth of NBFIs presents opportunities, it also introduces new risks. Regulatory scrutiny, cybersecurity vulnerabilities, and the volatility of fintech valuations post-2022 market corrections require a nuanced approach to diversification. For example, the fintech sector's projected 15% annual revenue growth (vs. 6% for traditional banks) is concentrated in scaled players with over $500 million in revenue, according to the St. Louis Fed analysis. Overexposure to these firms could amplify portfolio risk if regulatory or technological disruptions arise.

A balanced strategy might involve hedging against these risks by diversifying across subsectors. The global fintech industry, valued at $280 billion in 2025, is expected to grow to $1.38 trillion by 2034, driven by innovations like blockchain and API-driven financial infrastructure, according to an HSBC report. Investors could allocate capital to both high-growth fintechs and more stable, technology-enabled traditional banks that are adapting to the new ecosystem.

Conclusion

The rise of non-bank financial powerhouses is not a passing trend but a fundamental reordering of the financial services sector. For investors, this shift demands a dual focus: reallocating capital to high-growth NBFIs while diversifying across subsectors to mitigate risks. As the IMF notes, megatrends such as digital inclusion, technological innovation, and shifting consumer behavior will continue to amplify the influence of NBFIs. Those who act strategically today will be well-positioned to capitalize on the opportunities-and navigate the challenges-of tomorrow's financial landscape.

Comentarios

Aún no hay comentarios