Dimensional US Real Estate ETF: Evaluating Dividend Appeal in a Low-Yield Environment

In a market environment where benchmark yields remain stubbornly low, income-focused investors are increasingly scrutinizing the sustainability and competitiveness of ETF dividends. The Dimensional US Real Estate ETF (DFAR), with its recent $0.1431 per-share dividend declared on September 22, 2025[1], offers a case study in balancing yield, cost efficiency, and financial health. This analysis evaluates DFAR's appeal in the context of its 2.17% trailing twelve-month (TTM) yield[2], its expense ratio, and its position relative to peers like the Schwab US REIT ETF (SCHH) and Vanguard Real Estate ETF (VNQ).

DFAR's Dividend: A Cost-Effective but Volatile Proposition

DFAR's 0.19% expense ratio[3] positions it as a cost-competitive option for real estate exposure, particularly for investors prioritizing U.S. real estate equities. However, the fund's dividend history reveals significant volatility. For instance, the June 2025 payout of $0.141 per share marked a 60.51% decline compared to the prior year's $0.36 per share distribution[2]. This volatility raises questions about the sustainability of its current $0.1431 dividend, especially in a low-yield environment where investors demand reliable income streams.

The fund's net asset value (NAV) of $23.69 as of September 23, 2025[3], slightly lags its market price of $23.75, suggesting limited premium for liquidity. While this could indicate undervaluation, it also underscores the need for careful assessment of underlying asset performance.

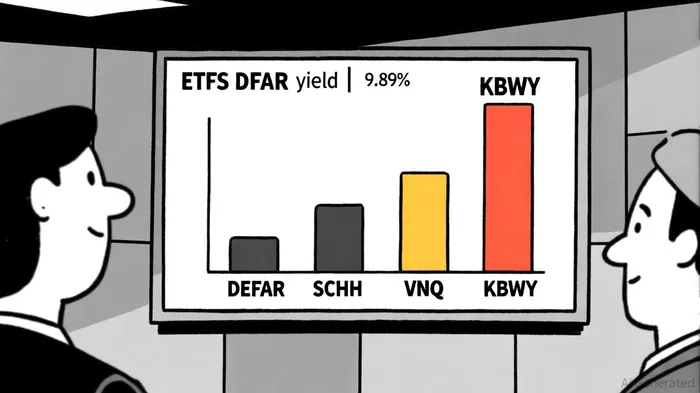

Comparative Landscape: Yield vs. Risk

DFAR's 2.17% yield trails peers like the Schwab US REIT ETF (SCHH) at 3.06% and the Vanguard Real Estate ETF (VNQ) at 3.92%[4]. The Invesco KBW Premium Yield Equity REIT ETF (KBWY) stands out with a 9.89% yield[4], though its exceptionally high payout likely reflects aggressive leverage or return-of-capital distributions, which may not be sustainable.

For context, the 10-year Treasury yield stood at 4.11% on September 19, 2025[5], making DFAR's yield appear less attractive compared to risk-free alternatives. Yet real estate ETFs like DFARDFAR-- offer diversification benefits and potential capital appreciation, which may justify their lower yields for some investors.

Sustainability Concerns: Earnings vs. Return of Capital

A critical unanswered question is whether DFAR's dividends are sourced from earnings or return of capital. While the fund's prospectus does not explicitly clarify this[6], real estate ETFs often blend both. Return-of-capital distributions, though tax-advantaged in the short term, reduce the fund's NAV and may signal pressure on underlying asset values. Investors seeking long-term sustainability should prioritize ETFs with clear earnings-based payout structures, a metric DFAR currently lacks in public disclosures[6].

Conclusion: A Niche Player in a Competitive Field

DFAR's low expense ratio and real estate focus make it a viable option for cost-conscious investors, but its dividend volatility and lack of clarity on payout sources limit its appeal in a low-yield environment. For those prioritizing yield stability, alternatives like VNQ or SCHH may offer better value, albeit with trade-offs in cost or risk profile. Investors considering DFAR should monitor its future dividend announcements and seek transparency from the fund provider on distribution composition.

Comentarios

Aún no hay comentarios