Delta Air Lines' Q3 Earnings: A Critical Barometer for Airline Recovery

The third quarter of 2025 has emerged as a pivotal test for DeltaDAL-- Air Lines' (NYSE: DAL) post-pandemic recovery, with its earnings report offering a mixed but telling snapshot of the broader airline industry's challenges. As the largest U.S. carrier by international destinations, Delta's performance in unit revenue, cost management, and balance sheet resilience provides critical insights into whether the sector can sustain its recent momentum amid macroeconomic headwinds.

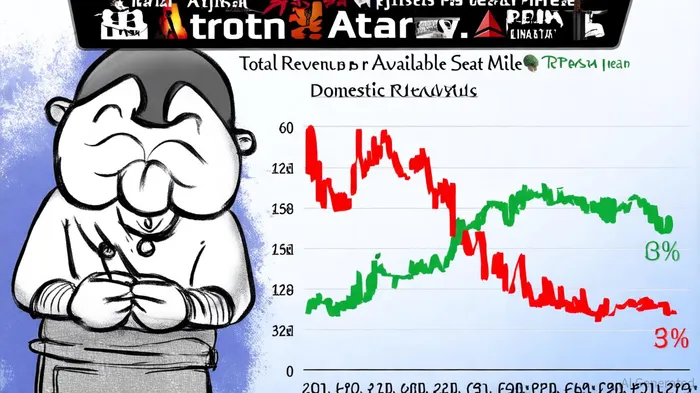

Unit Revenue Trends: A Tale of Two Markets

Delta's Q3 2025 results underscored the fragility of its revenue streams. Adjusted Total Revenue per Available Seat Mile (TRASM) fell 3% year-over-year, despite a 4% increase in available seat miles, signaling that capacity expansion outpaced demand or pricing power weakened, according to a Panabee analysis. This decline was most pronounced domestically, where revenue dropped 1%, reflecting softer business travel demand and competitive pressures in the U.S. market, according to a MarketBeat alert. However, international routes offered a counterbalance: Pacific region revenue surged 11%, and Transatlantic markets grew 2%, driven by premium cabin demand and Delta's strategic focus on high-yield corridors, the Panabee analysis noted.

Premium and loyalty revenue proved to be lifelines, contributing 59% of total adjusted revenue. Premium revenue rose 5% year-over-year, while loyalty revenue climbed 8%, demonstrating Delta's ability to monetize its elite customer base and ancillary services, per the Panabee write-up. These high-margin streams, however, cannot fully offset the drag from domestic underperformance, raising questions about the sustainability of Delta's pricing strategy in a low-inflation environment.

Cost Discipline: Operational Gains vs. Structural Pressures

Delta's cost management efforts in Q3 2025 showcased both innovation and limitations. The airline achieved its 2025 jet fuel savings target ahead of schedule, cutting 45 million gallons of fuel consumption and $110 million in costs through operational tweaks like weight reduction, optimized routing, and drag-reduction technologies, as described in a SustainabilityMag article. Fleet modernization further bolstered efficiency, with 42 new aircraft-28% more fuel-efficient per seat mile-joining the fleet, according to a GuruFocus report.

Yet structural challenges persist. Delta's adjusted operating margin contracted by 1.5 percentage points to 13.2%, reflecting the TRASM decline and rising labor costs amid a tight labor market, the Panabee piece found. Free cash flow plummeted 42% year-over-year to $733 million, highlighting the strain of balancing capital expenditures with profitability, Panabee also reported. While Delta's cost discipline is commendable, these figures suggest that operational efficiencies alone may not be sufficient to offset broader economic pressures.

Balance Sheet Resilience: Progress Amid Constraints

Delta's balance sheet remains a cornerstone of its recovery narrative. The airline reduced adjusted net debt by $1.7 billion since year-end 2024, bringing it to $16.3 billion, and aims for an additional $3 billion in reductions by year-end 2025, the Panabee analysis noted. This deleveraging reflects disciplined capital allocation, though liquidity metrics remain a concern: a current ratio of 0.38 and quick ratio of 0.33 indicate limited short-term flexibility to navigate shocks, according to GuruFocus data.

The company's debt-to-equity ratio of 1.22 suggests a balanced approach to leveraging for growth, per GuruFocus. However, the combination of elevated debt and declining free cash flow raises questions about Delta's ability to fund dividends and share buybacks without compromising operational flexibility. The 25% dividend increase announced in Q2 2025, while a positive signal for shareholder returns, must be weighed against the need for prudence in uncertain economic conditions, GuruFocus observed.

Strategic Adjustments: Navigating Uncertainty

Delta's Q3 2025 guidance-EPS of $1.25–$1.75 versus the $1.49 consensus-reflects a recalibration of expectations, as noted in the Panabee coverage. The airline has abandoned second-half 2025 capacity growth, retiring 30 older aircraft and focusing on fleet modernization to reduce costs and emissions, according to an Aviation Outlook analysis. This pivot to domestic route optimization and international expansion underscores Delta's attempt to align supply with demand while capitalizing on higher-yield markets.

Conclusion: A Barometer with Mixed Signals

Delta's Q3 2025 earnings highlight both the resilience and vulnerabilities of the airline sector. While premium revenue and cost discipline provide a buffer, the TRASM decline and liquidity constraints signal that the recovery is far from linear. For investors, the key takeaway is that Delta's ability to navigate this period will hinge on its capacity to balance growth ambitions with fiscal prudence. As the October 9 earnings report unfolds, all eyes will be on whether Delta can translate its strategic adjustments into a sustainable path to profitability.

Comentarios

Aún no hay comentarios