The Decline in Chinese Soybean Demand and Its Implications for Global Agricultural Commodities Markets

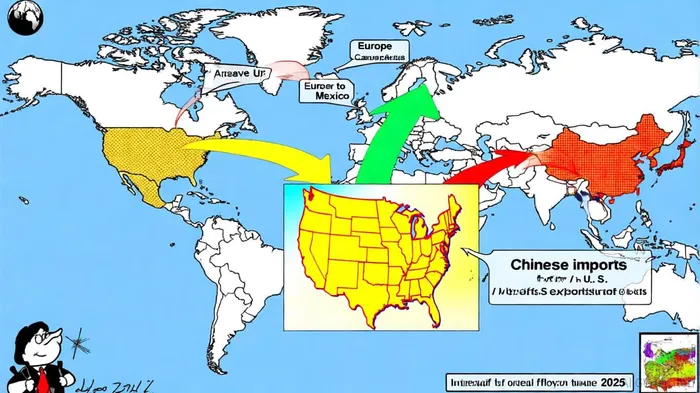

The global agricultural commodities market is undergoing a seismic shift as Chinese soybean demand, once a cornerstone of U.S. agribusiness, faces a structural decline. This trend, driven by geopolitical tensions and trade policy realignments, has profound implications for U.S. agribusiness investors. According to a report by the World Economic Forum, the U.S. tariff policies under President Donald Trump's 2025 administration—averaging 18.2% by July 2025—have triggered a strategic reallocation of Chinese trade networks[4]. China, the world's largest soybean importer, has redirected 6% of its exports to Europe and 25% to Mexico and Canada to circumvent tariffs, fragmenting traditional trade routes and reducing U.S. market share[3].

The Drivers of Declining Demand

The decline in Chinese soybean demand is not merely a function of tariffs but a symptom of broader geoeconomic fragmentation. As stated by the Future of Jobs Report 2025, over one-fifth of global employers cite trade restrictions as a critical operational risk, accelerating the diversification of supply chains[2]. For soybeans, this means China is increasingly sourcing from Brazil, Argentina, and even African producers to bypass U.S. tariffs. Data from the World Economic Forum further indicates that U.S. soybean exports to China have contracted as Beijing prioritizes bilateral agreements with non-U.S. partners to secure supply[4].

Commodity Exposure Risks for U.S. Agribusiness

U.S. agribusiness investors now face heightened exposure risks. The soybean market, which accounted for 15% of U.S. agricultural exports in 2024, is particularly vulnerable to policy-driven volatility. The Trump administration's 50% tariff on copper and 25% tariff on cars, part of a broader protectionist agenda, have created a ripple effect, deterring Chinese buyers from locking in long-term contracts with U.S. suppliers[4]. This uncertainty has led to a 12% drop in U.S. soybean export volumes to China year-over-year, according to the same WEF analysis[4].

Moreover, the U.S. Department of Agriculture's February 2025 trade outlook, while not quantifying soybean-specific impacts, underscores the sector's vulnerability to geopolitical shifts. Investors must also consider the indirect effects of China's domestic policies, such as anti-dumping duties on U.S. agricultural goods, which further erode competitiveness[3].

Strategic Implications for Investors

For U.S. agribusinesses, the decline in Chinese demand necessitates a reevaluation of risk management strategies. Diversification into emerging markets, such as Southeast Asia and Africa, could mitigate losses, but these regions lack the infrastructure to absorb U.S. export volumes immediately. Additionally, innovation in value-added soybean products—such as plant-based proteins—may offset raw commodity price declines. However, these strategies require capital investment and time, leaving short-term exposure unaddressed.

Conclusion

The decline in Chinese soybean demand represents a pivotal risk for U.S. agribusiness investors, compounding existing challenges from climate change and domestic policy shifts. While the U.S. remains a key supplier, the erosion of market share underscores the need for agile, diversified strategies. Investors must monitor trade policy developments closely, as even minor adjustments to tariffs or trade agreements could further destabilize this critical sector.

Comentarios

Aún no hay comentarios